|

|

|

AGENDA

Audit and Risk Sub-committee Meeting

|

|

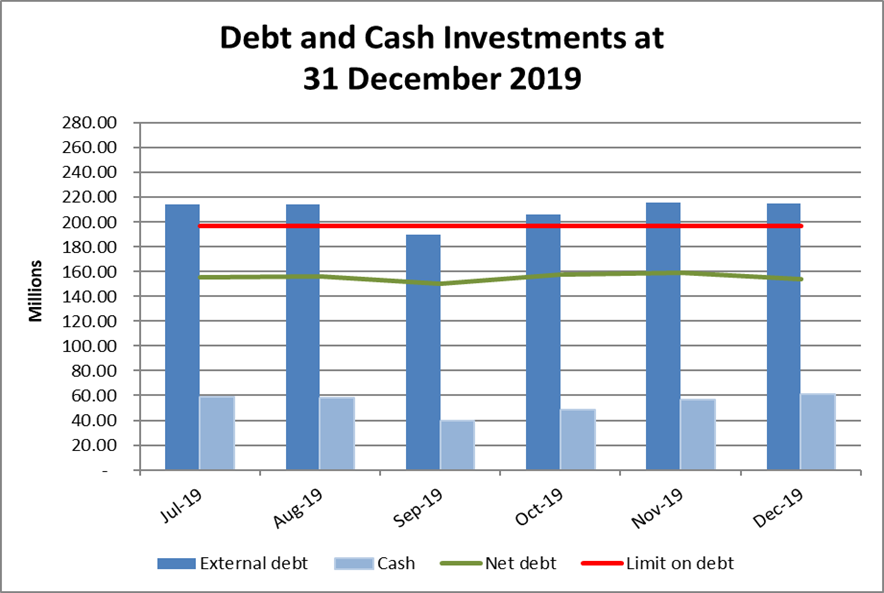

I hereby give notice that a Meeting of the Audit and Risk Subcommittee will be held on:

|

|

Date:

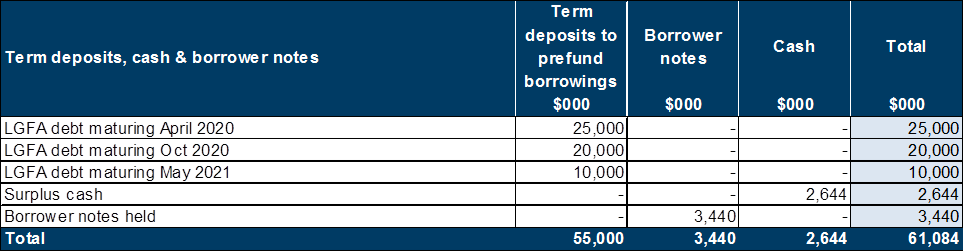

|

Thursday, 20 February

2020

|

|

Time:

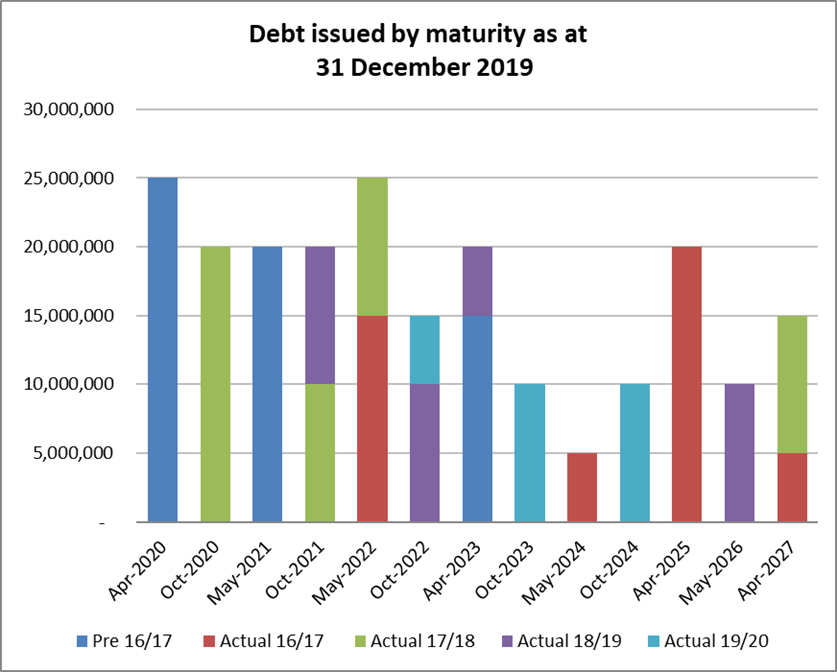

|

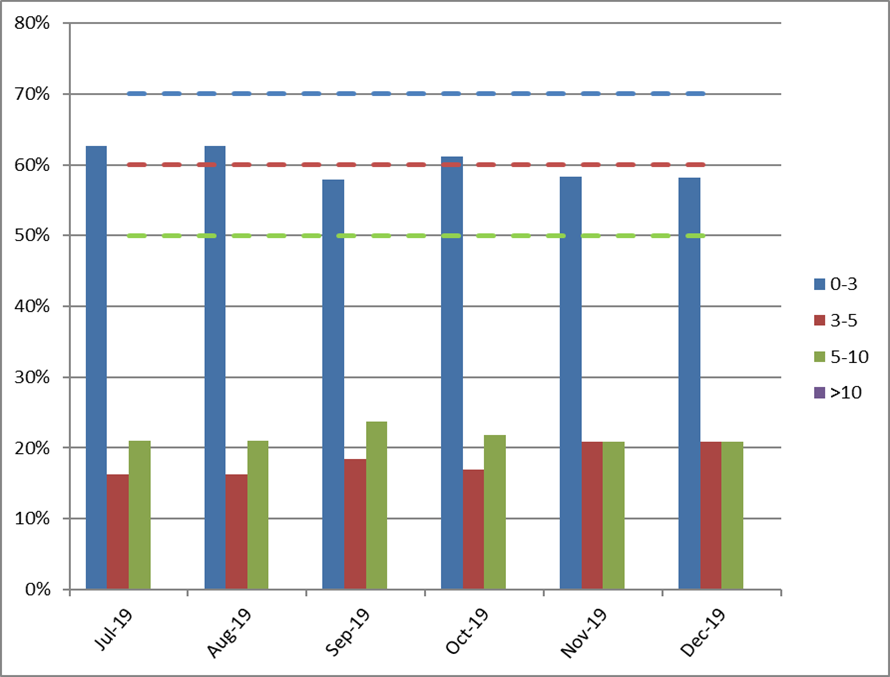

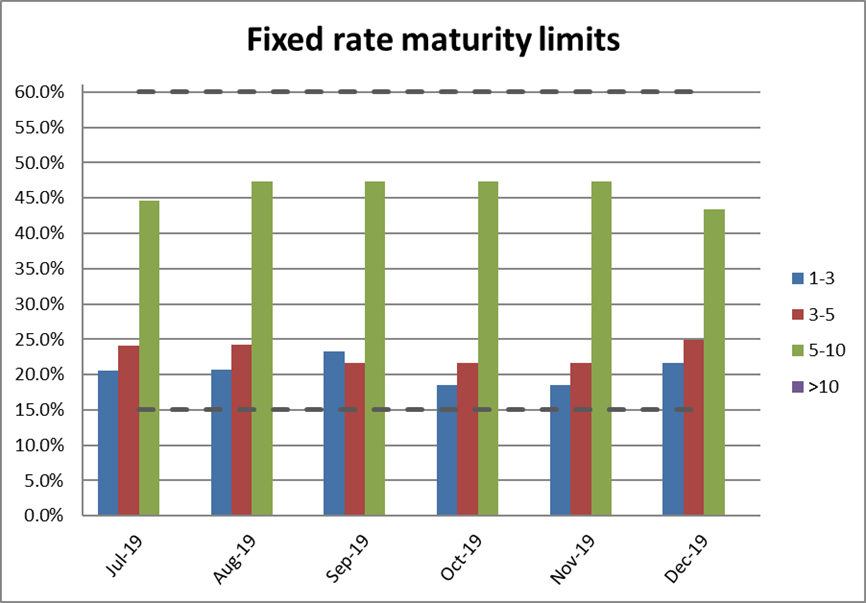

9.30am

|

|

Location:

|

Council Chamber

Ground Floor, 175 Rimu Road

Paraparaumu

|

|

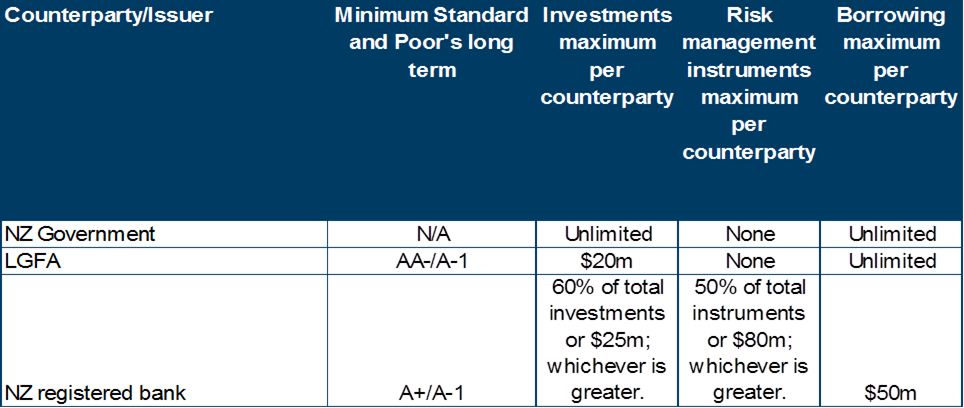

Mark de Haast

Group Manager

|

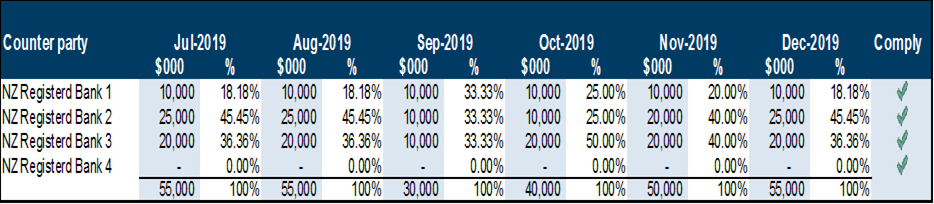

|

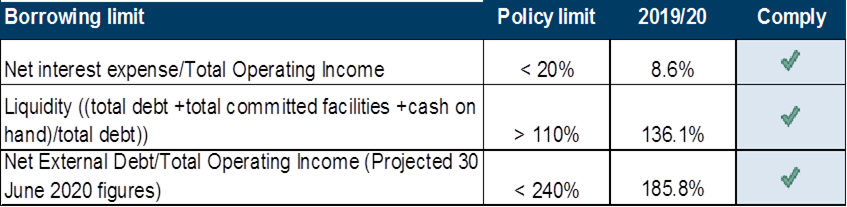

Audit

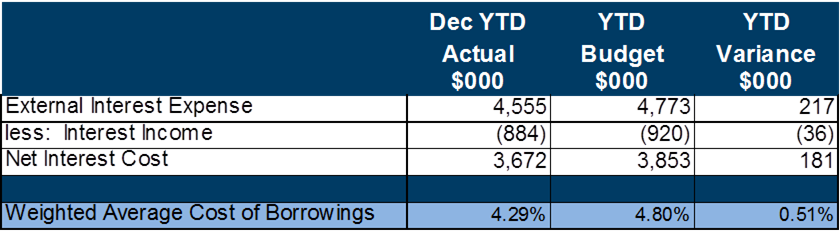

and Risk Sub-committee Meeting Agenda

|

20 February 2020

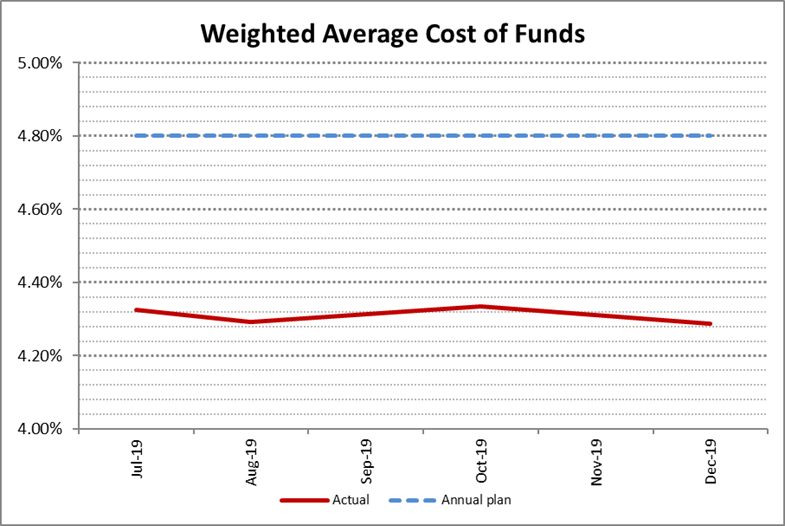

|

Kapiti Coast District Council

Notice

is hereby given that a meeting of the Audit and Risk Subcommittee will

be held in the Council Chamber,

Ground Floor, 175 Rimu Road, Paraparaumu, on Thursday 20 February 2020, 9.30am.

Audit and Risk

Subcommittee Members

|

Mr Bryan Jackson

|

Chair

|

|

Cr Angela Buswell

|

Deputy Chair

|

|

Mayor K Gurunathan

|

Member

|

|

Deputy Mayor Janet Holborow

|

Member

|

|

Cr Gwynn Compton

|

Member

|

|

Mr Gary Simpson

|

Member

|

2 Council

Blessing

“As we deliberate on the

issues before us, we trust that we will reflect positively on the communities

we serve. Let us all seek to be effective and just, so that with courage,

vision and energy, we provide positive leadership in a spirit of harmony and

compassion.”

I a mātou e whiriwhiri ana

i ngā take kei mua i ō mātou aroaro, e pono ana mātou ka

kaha tonu ki te whakapau mahara huapai mō ngā hapori e mahi nei

mātou. Me kaha hoki mātou katoa kia whaihua, kia tōtika

tā mātou mahi, ā, mā te māia, te tiro whakamua me te

hihiri ka taea te arahi i roto i te kotahitanga me te aroha.

3 Apologies

4 Declarations

of Interest Relating to Items on the Agenda

Notification from Elected

Members of:

4.1 – any interests that

may create a conflict with their role as an elected member relating to the items

of business for this meeting, and

4.2 – any interests in

items in which they have a direct or indirect pecuniary interest as provided

for in the Local Authorities (Members’ Interests) Act 1968

5 Public

Speaking Time for Items Relating to the Agenda

6 Members’

Business

(a)

Public Speaking Time Responses

(b)

Leave of Absence

(c)

Matters of an Urgent Nature (advice to be provided to the Chair prior to

the commencement of the meeting)

7 Updates

Nil

8 Reports

8.1 Proposal

to conduct the audit of the Council on behalf of the Auditor-General for 2020,

2021 and 2022 financial years

Author: Anelise

Horn, Manager Financial Accounting

Authoriser: Mark

de Haast, Group Manager

Purpose of Report

1 This

report informs the Audit and Risk Subcommittee of the proposal from

Council’s auditors, Ernst & Young, to carry out the annual audits of

Council on behalf of the Auditor-General for the 2020, 2021 and 2022 financial

years.

Delegation

2 The

Audit and Risk Subcommittee has delegated authority to consider this report

under the following delegation in the Governance Structure, Section C.1.

· Confirming

the terms of engagement for each audit with a recommendation to the Council;

and receiving the external audit reports for recommendation to the Council.

Background

3 The

Auditor-General is the auditor of all ‘public entities’, including

Kāpiti Coast District Council.

4 Under

section 32 and 33 of the Public Audit Act 2001, the Auditor General has

appointed Ernst & Young to carry out the annual audit of the

Council’s financial statements and performance information for the three

years ending 30 June 2020 to 30 June 2022.

5 Fees

for the audit of public entities are set by the Auditor-General under section

42 of the Public Audit Act 2001. Ernst & Young has provided Council the

opportunity to consider the proposed fees before being recommended for approval

by the Auditor General. The Auditor-General will only set audit fees directly

if both parties fail to reach an agreement.

CONSIDERATIONS

6 Ernst & Young sets out their proposal to conduct the

statutory audit of the Council on behalf of the Auditor-General for the 2020,

2021 and 2022 Financial years (Refer to Appendix)

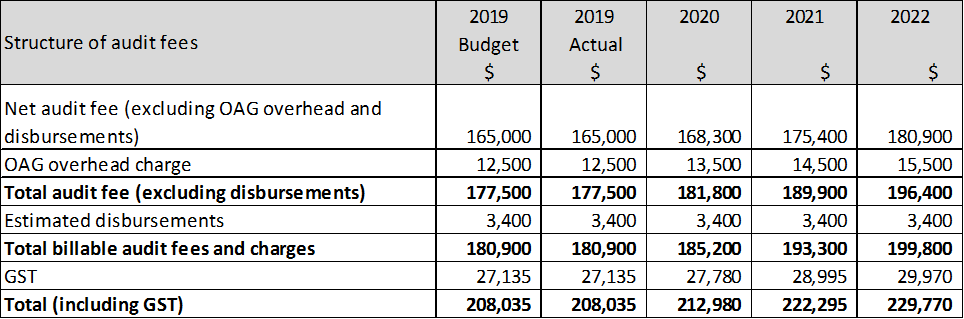

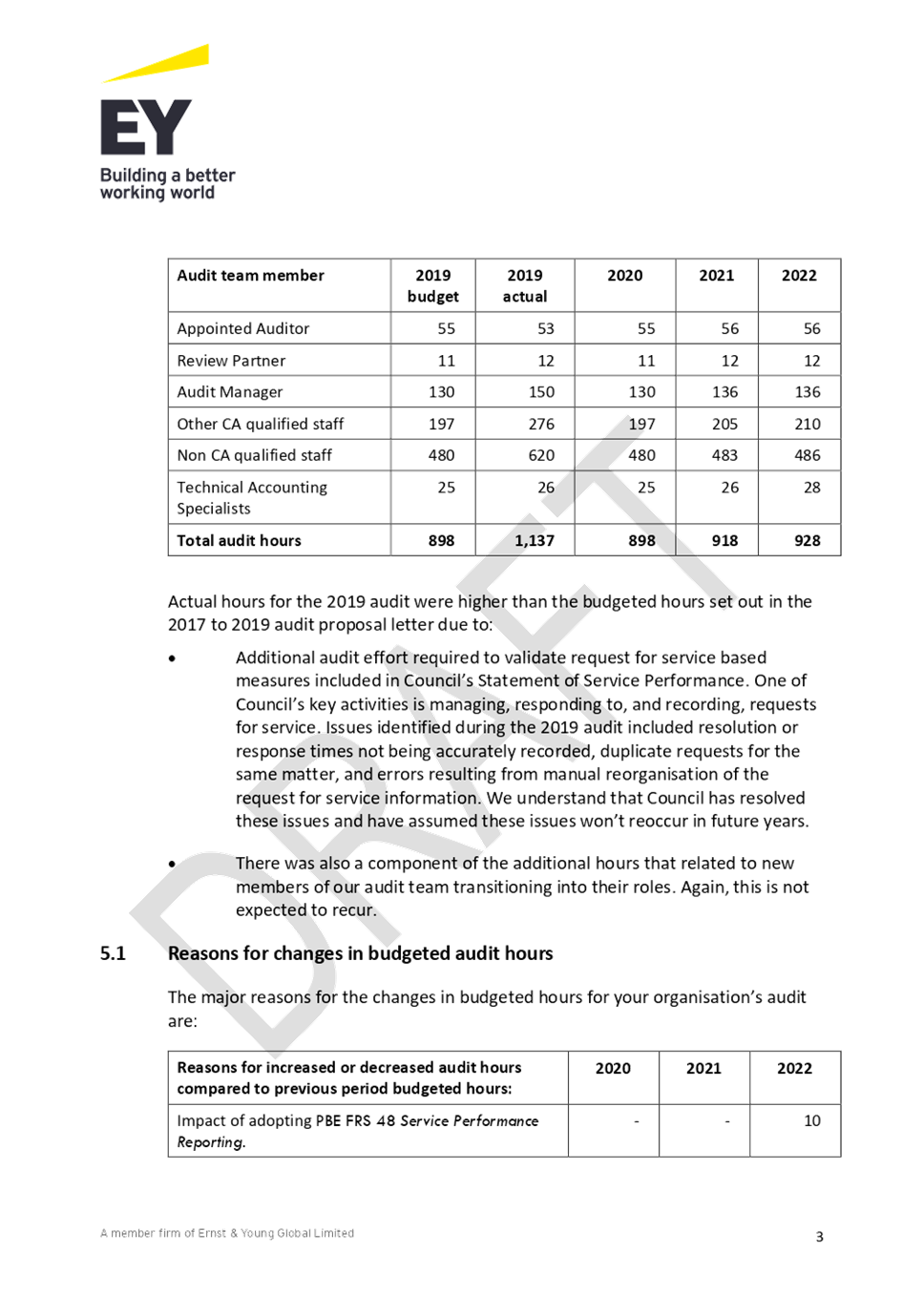

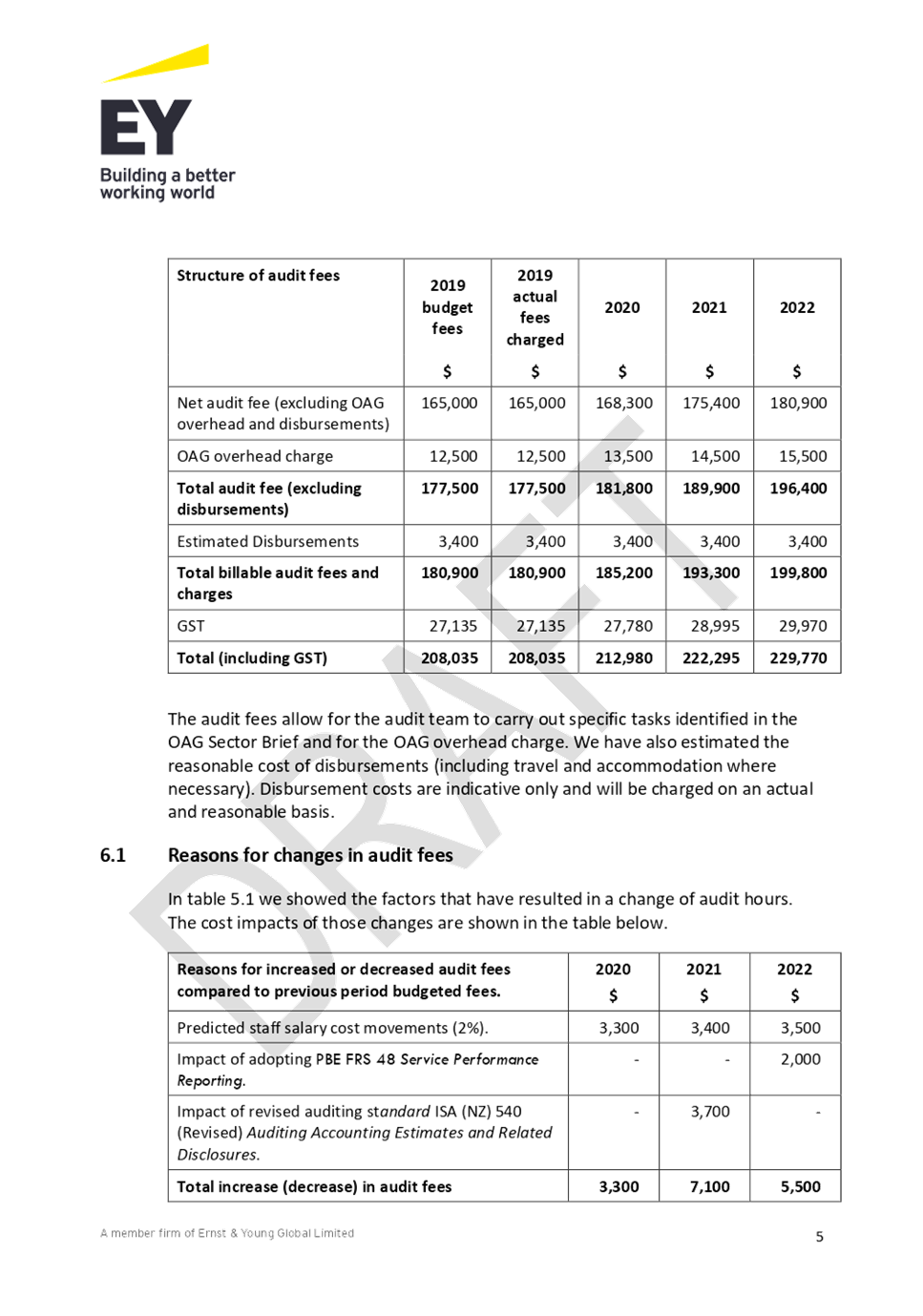

7 Ernst & Young’s proposed audit fees for the 2020,

2021 and 2022 Financial years are as follows:

8 Compared

to the actual audit fees for the 2019 financial year, the proposed fee increase

is due to the following:

· Ernst

and Young predict an annual staff salary cost movement of 2% per year for the

three-year period.

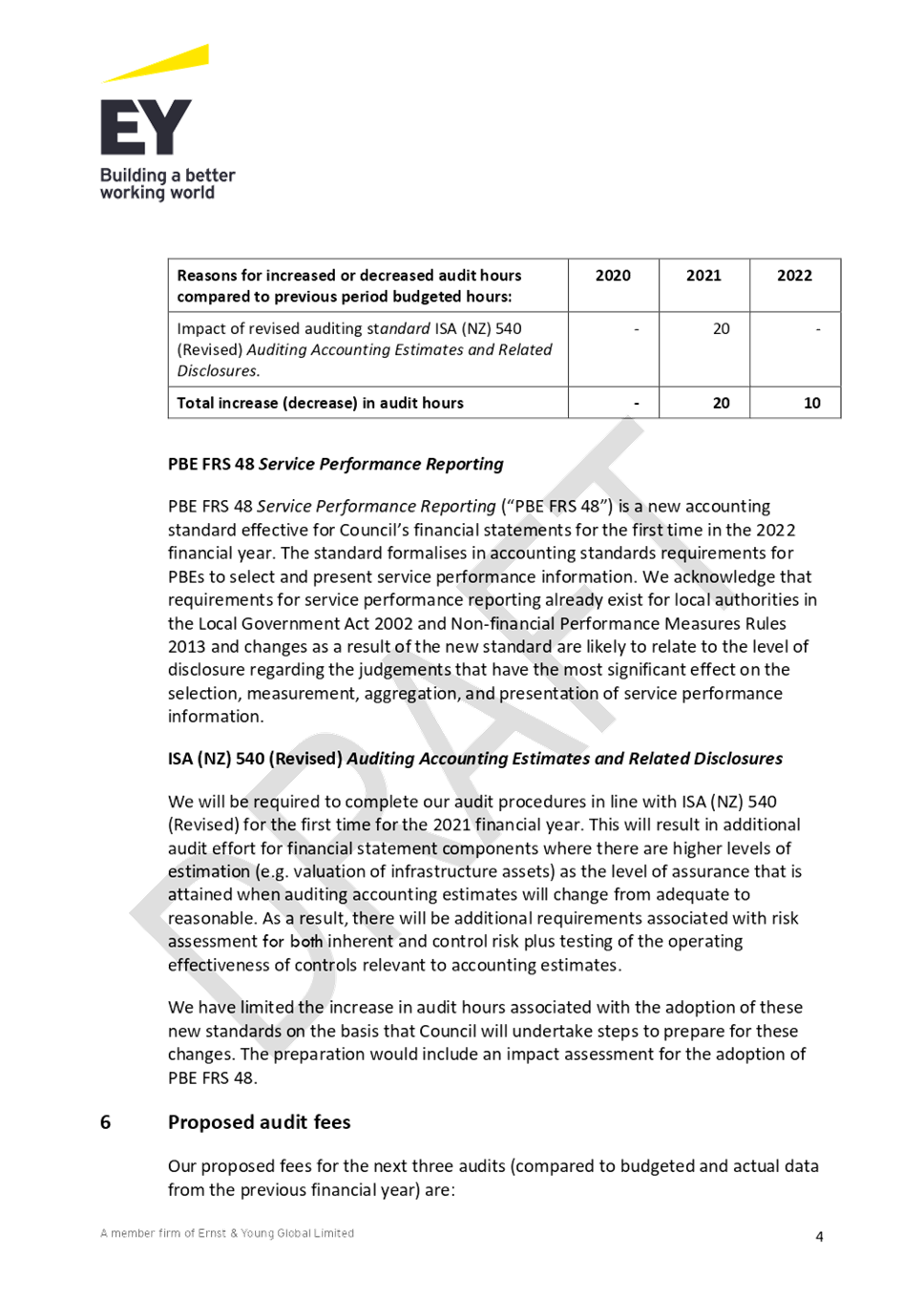

· 20

additional audit hours are required by the audit team in 2021, for the

implementation of the revised auditing standards ISA (NZ) 540 Auditing

Accounting Estimates and Related Disclosures.

· 10

additional audit hours are required by the audit team in 2022, for auditing the

impact of Council adopting PBE FRS 48 Service Performance Reporting.

9 Council

Officers have considered this proposal and have

determined that the proposed fee increases are fair and reasonable.

Considerations

Policy

considerations

10 There

are no policy considerations arising from this report.

Legal

considerations

11 There

are no legal issues in addition to those already outlined in this

report.

Financial

considerations

12 The

total audit fees payable to Ernst & Young for the year ended 30 June 2020

are $188,400 plus GST. This fee includes the audit of the 2019/20 Annual Report

including estimated disbursements and assessing the Council’s compliance

with its Debenture Trust Deed for the year ended 30 June 2020. This has been

included in the 2019/20 Annual Plan and no new money is required.

13 In

addition, the Council’s Debenture Trust Deed requires a full audit of the

Council’s register. Council has engaged PricewaterhouseCoopers (PwC), the

auditors of Computershare (the Council’s registrar), to complete a full

audit of the Council’s register. The fee for this service is $750

(inclusive of GST). This has been included in the 2019/20 Annual Plan and no

new money is required.

Tāngata

whenua considerations

14 There

are no tāngata whenua considerations arising from this report.

Significance and Engagement

Significance

policy

15 This

matter has a low level of significance under the Council’s Significance

and Engagement Policy.

Publicity

16 There

are no publicity considerations arising from this report.

|

Recommendations

17 That

the Audit and Risk Subcommittee receives and accepts Ernst &

Young’s proposal to conduct the audit of Council on behalf of the

Auditor-General for the 2020, 2021 and 2022 financial years.

|

Appendices

1. 2020-22

Draft KCDC Audit Proposal Letter ⇩

|

Audit

and Risk Sub-committee Meeting Agenda

|

20 February 2020

|

8.2 Ernst

and Young Audit Plan for the year ended 30 June 2020

Author: Anelise

Horn, Manager Financial Accounting

Authoriser: Mark

de Haast, Group Manager

Purpose of Report

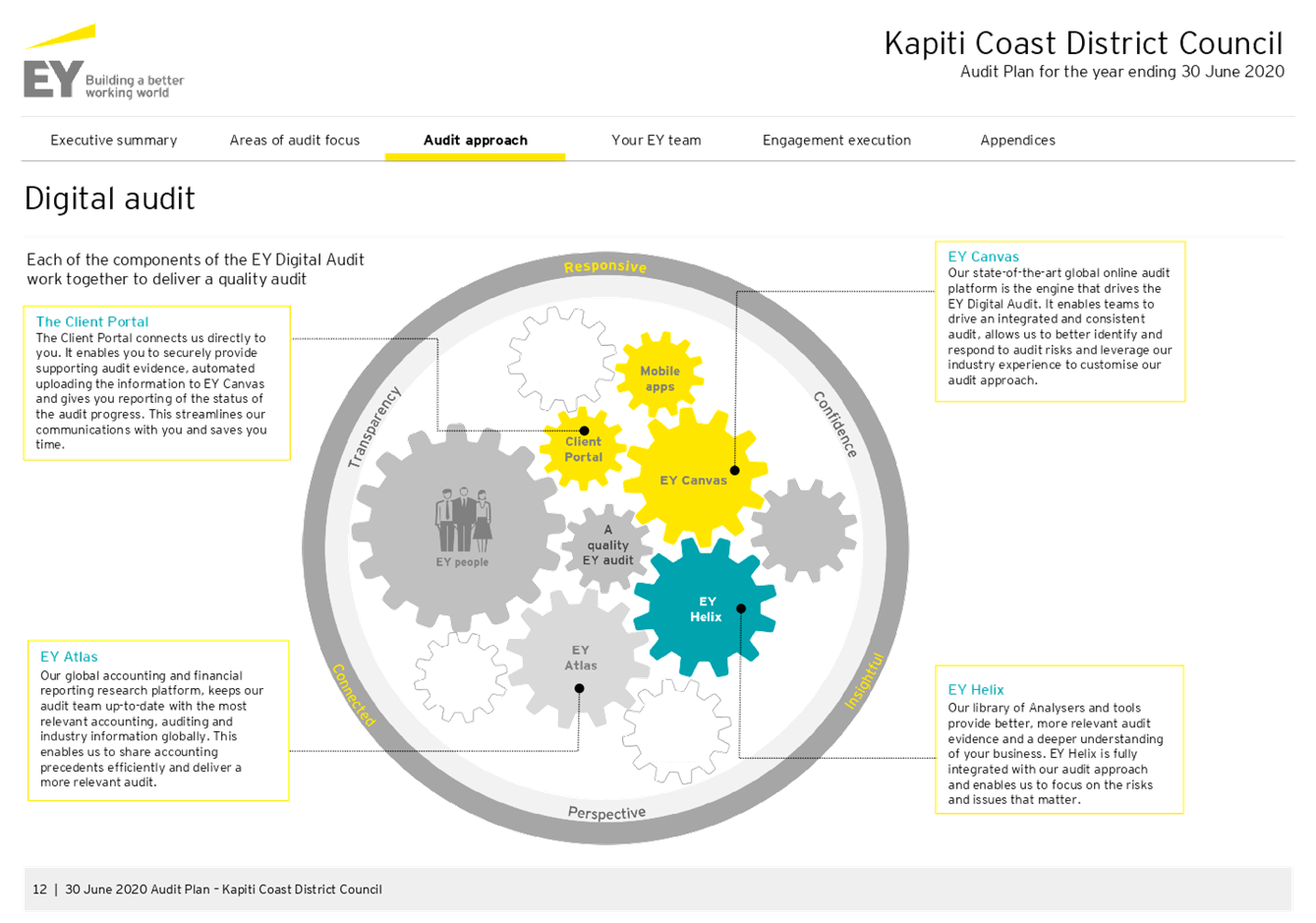

1 This

report provides the Audit and Risk Subcommittee with a summary of the Ernst

& Young Audit Plan for the year ending 30 June 2020.

Delegation

2 The

Audit and Risk Subcommittee has delegated authority to consider this report

under the following delegation in the Governance Structure, Section C.1.

· Confirming

the terms of engagement for each audit with a recommendation to the Council;

and receiving the external audit reports for recommendation to the Council.

· Obtaining

from external auditors any information relevant to the council’s

financial statements and assessing whether appropriate action has been taken by

management in response to the above.

Background

3 Council’s

Auditors, Ernst & Young (Audit) have been engaged to undertake the audit of

Council’s Annual Report, including the Council’s Summary Annual

Report and compliance with its Debenture Trust Deed, for the year ended 30 June

2020.

4 The

Audit Plan is attached as Appendix 1 to this report. This provides an

overview of audit’s focus areas, their risk assessment and their audit

approach for the year ended 30 June 2020.

Considerations

Audit

focus areas and risk assessment

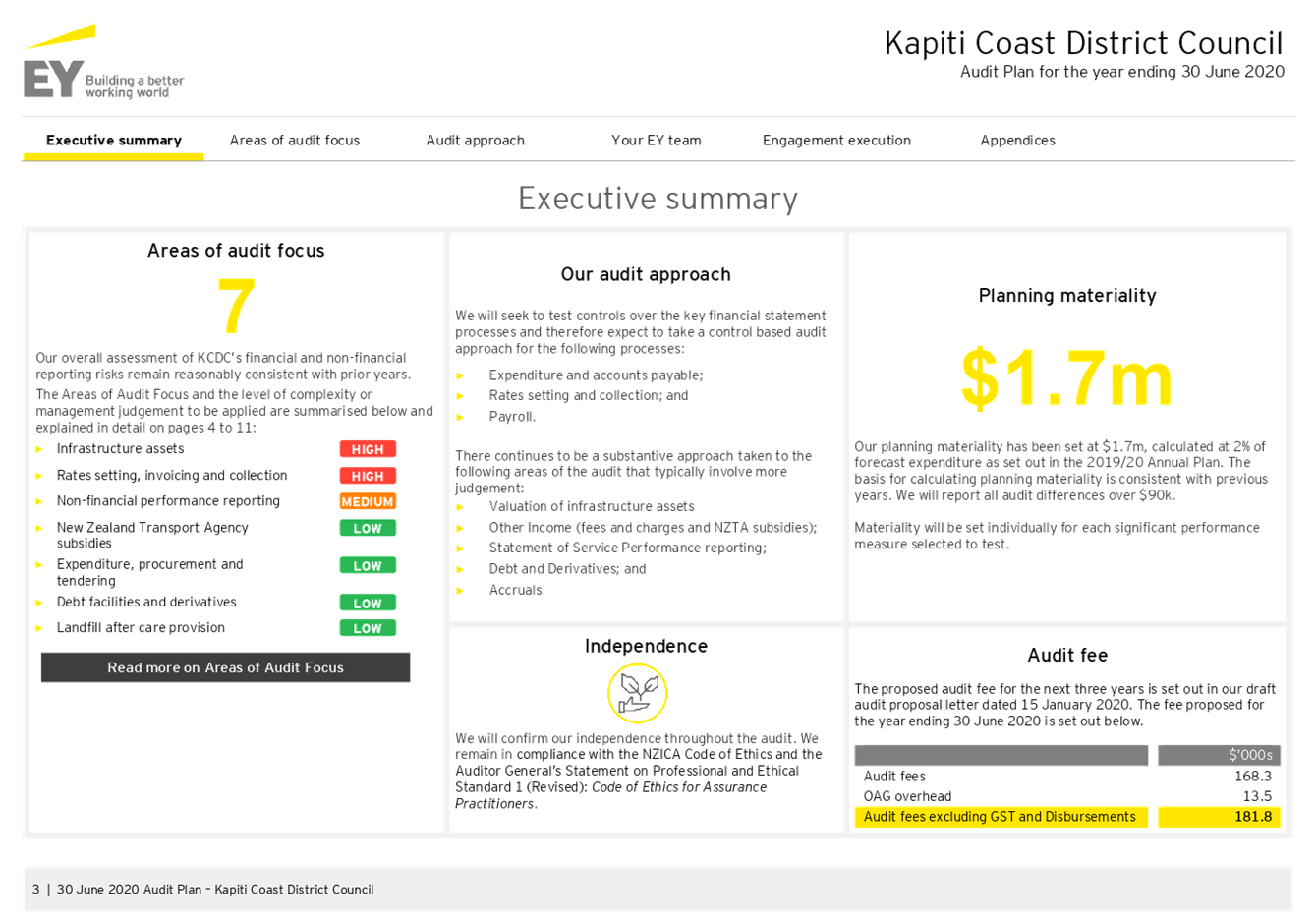

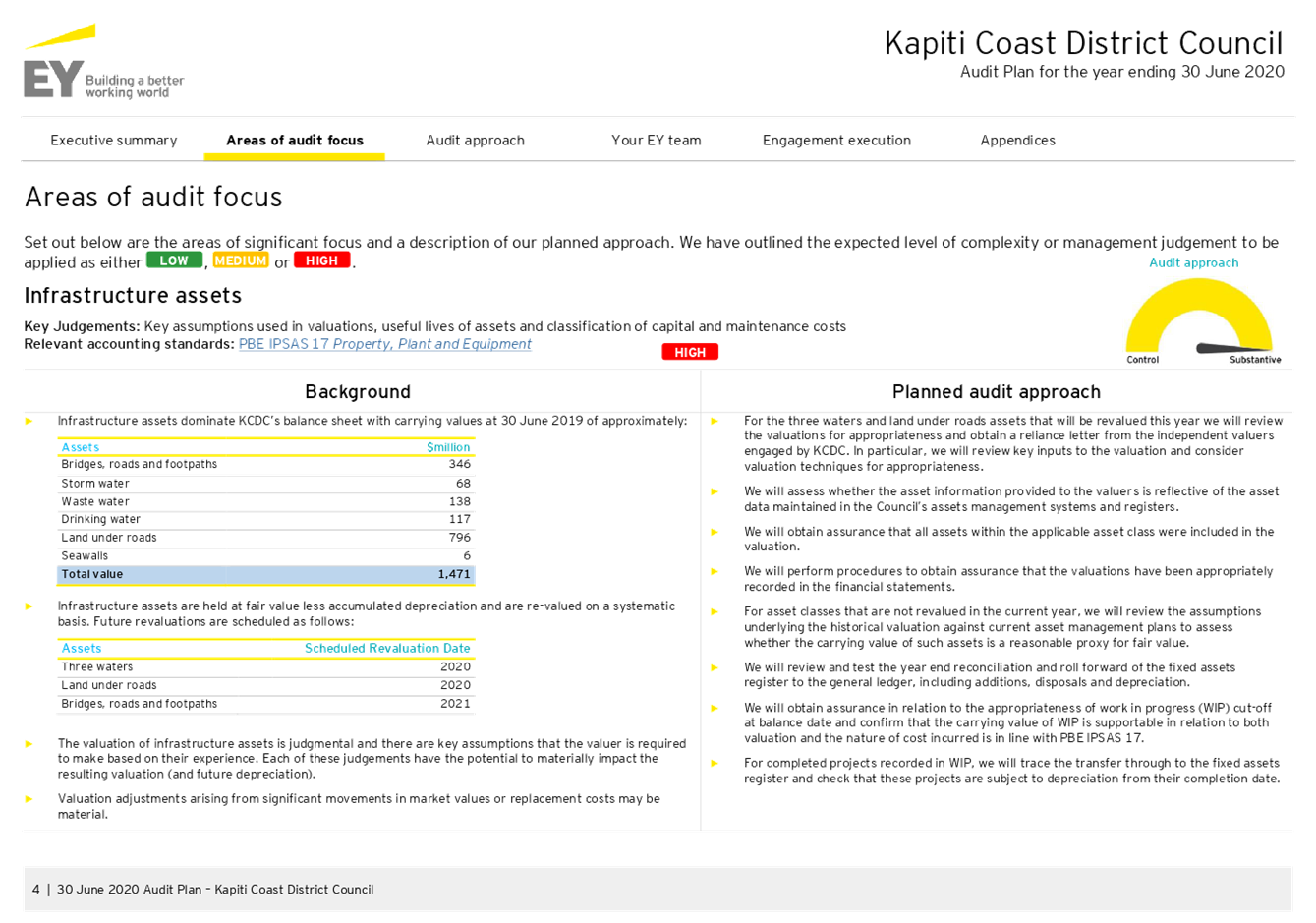

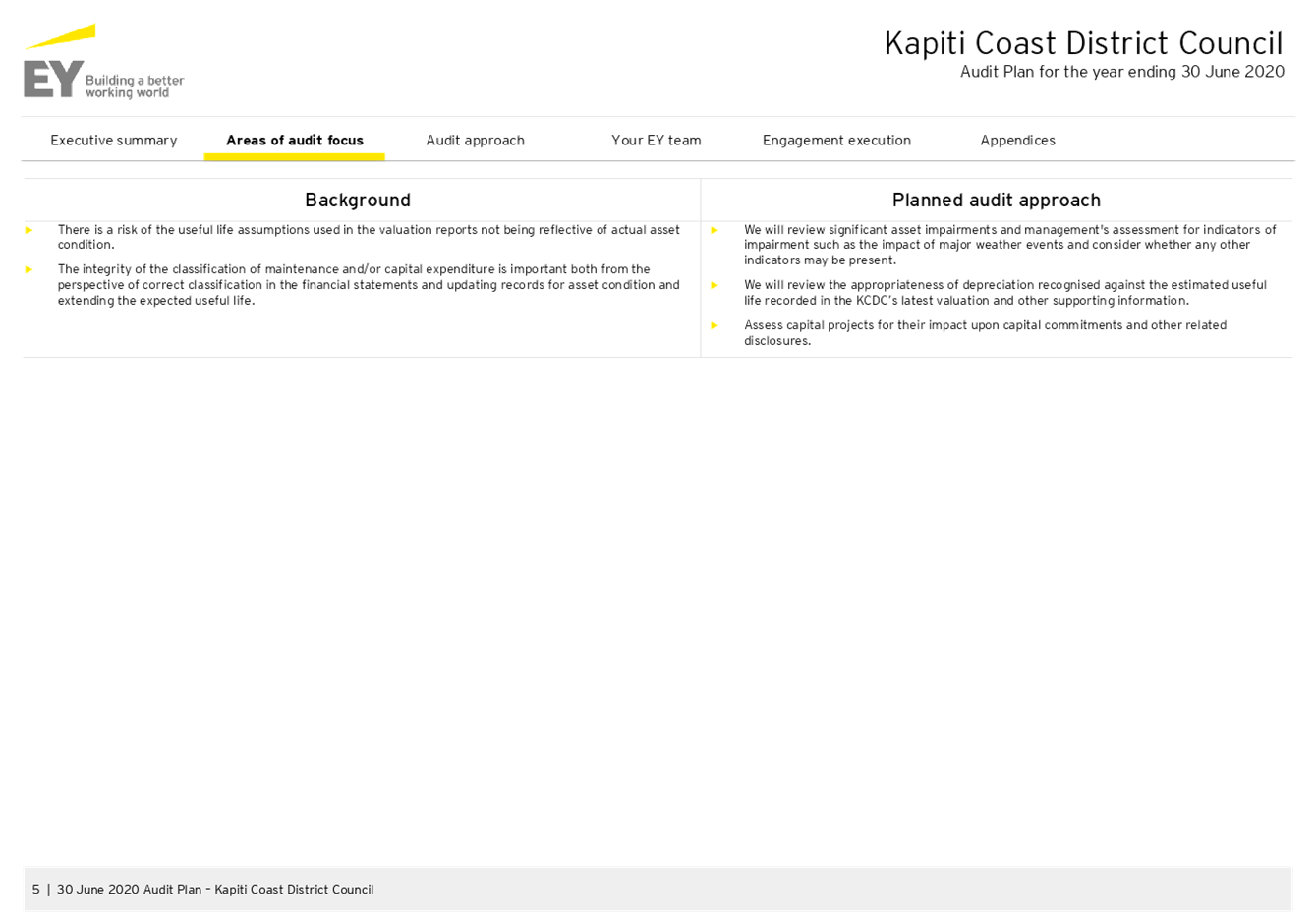

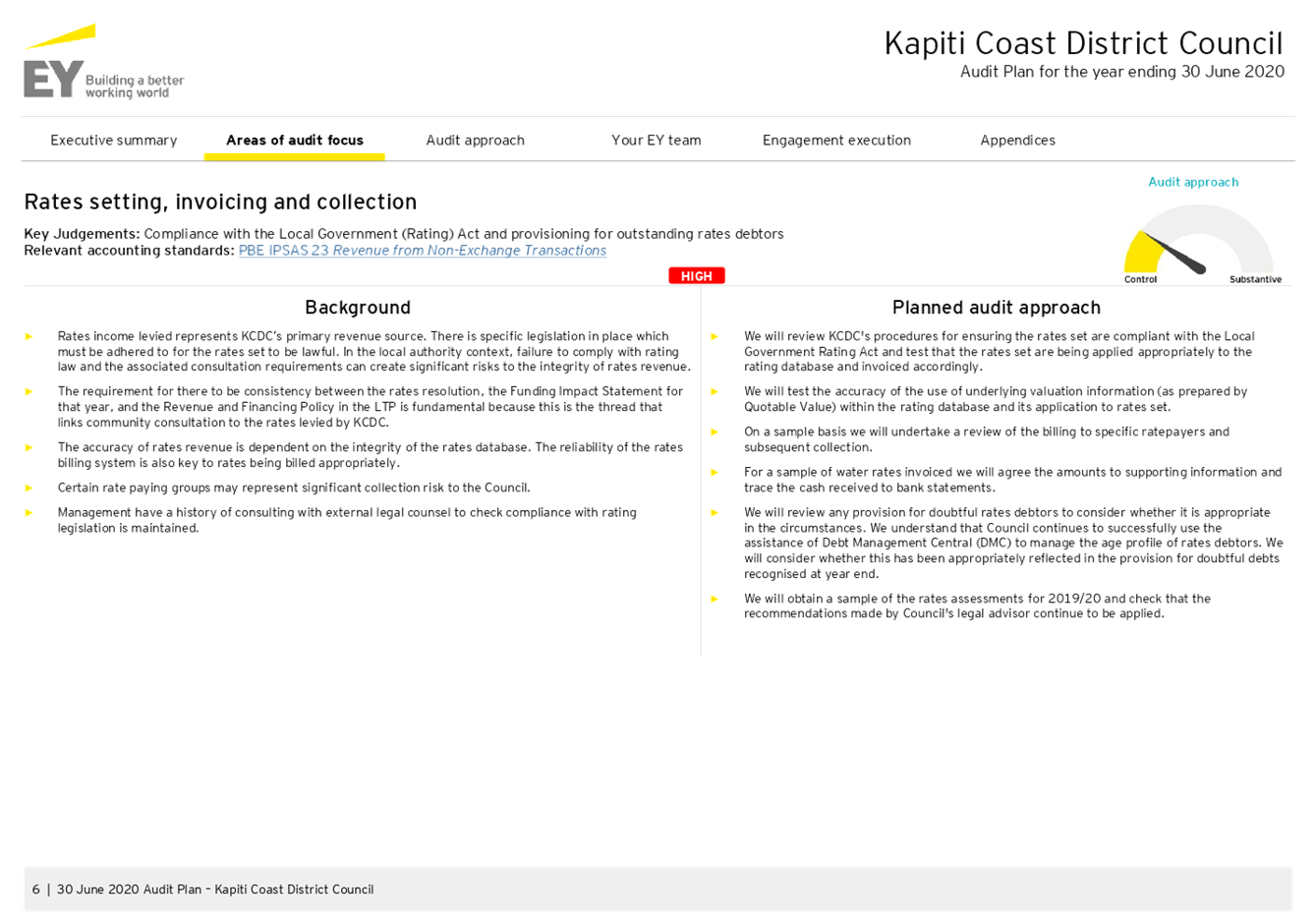

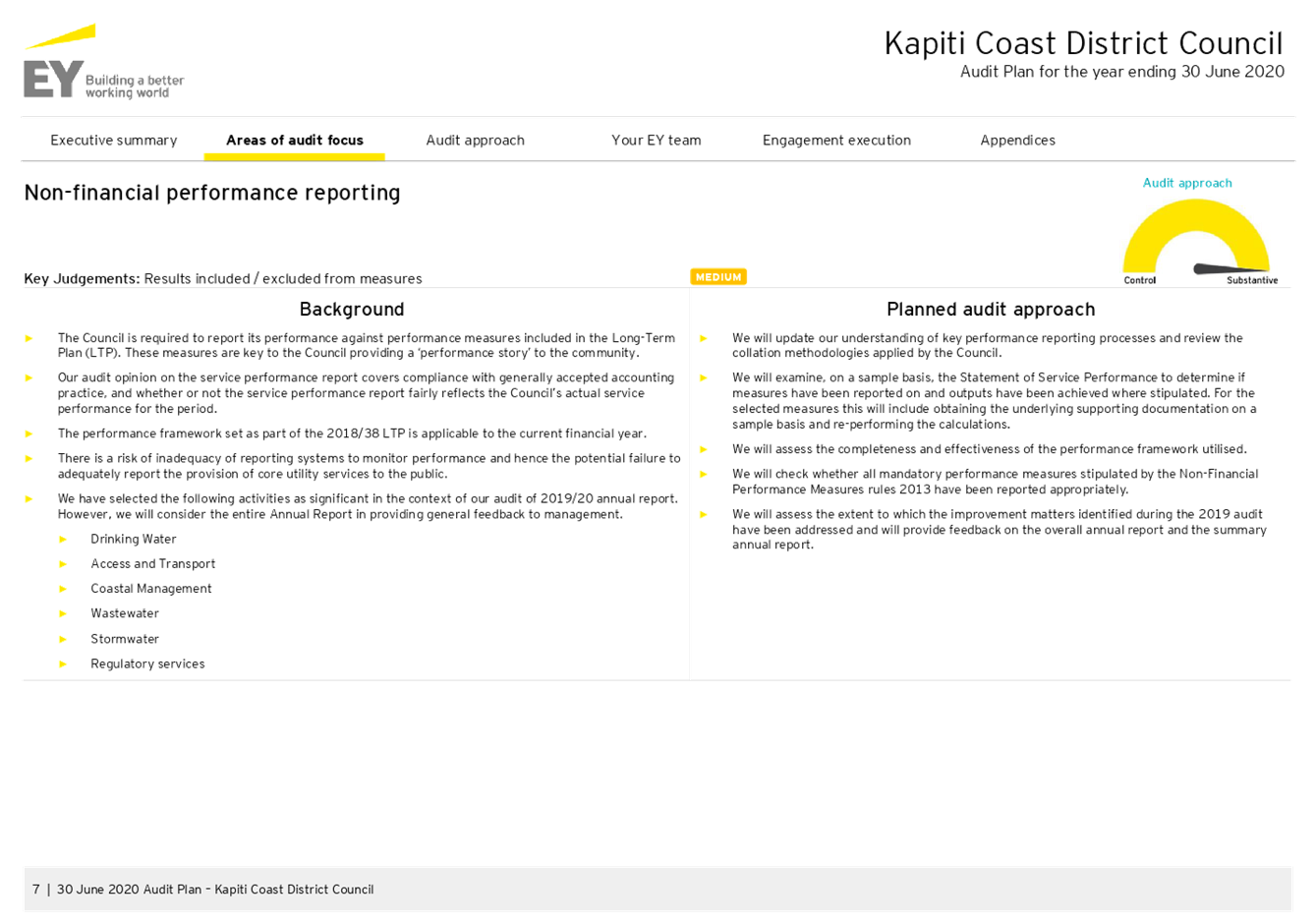

5 The

areas of audit focus, which are broadly consistent with the previous year are

summarised below:

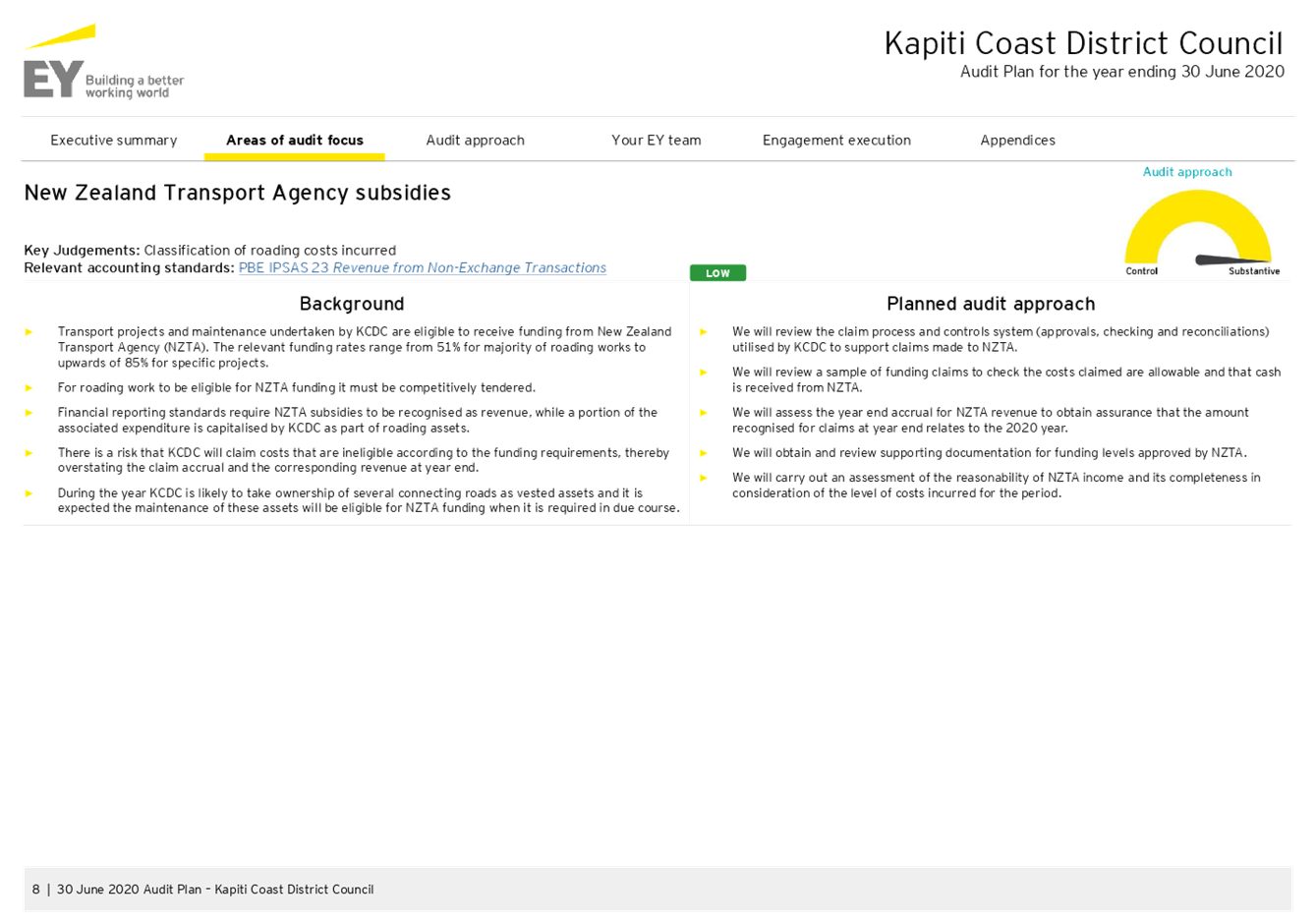

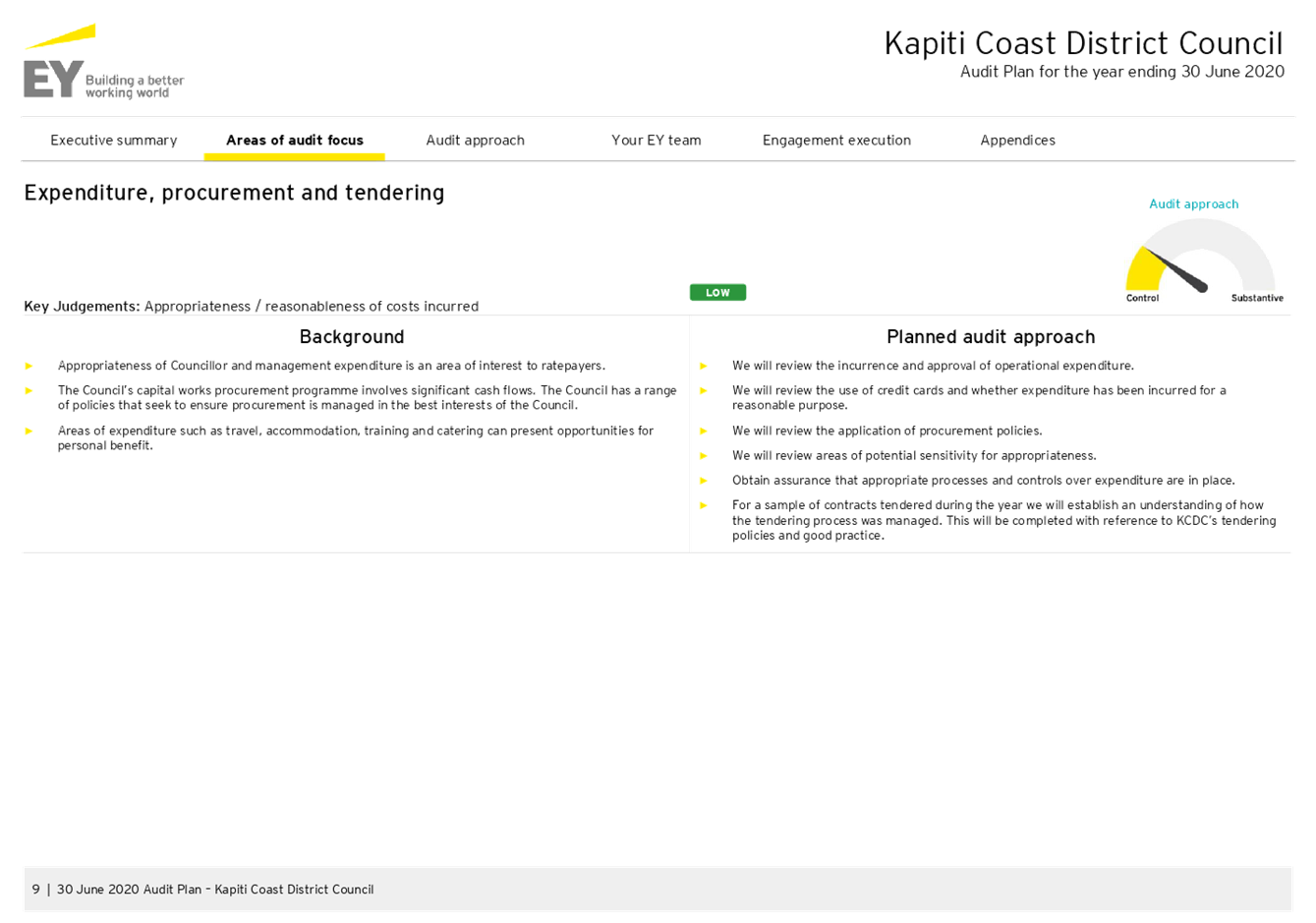

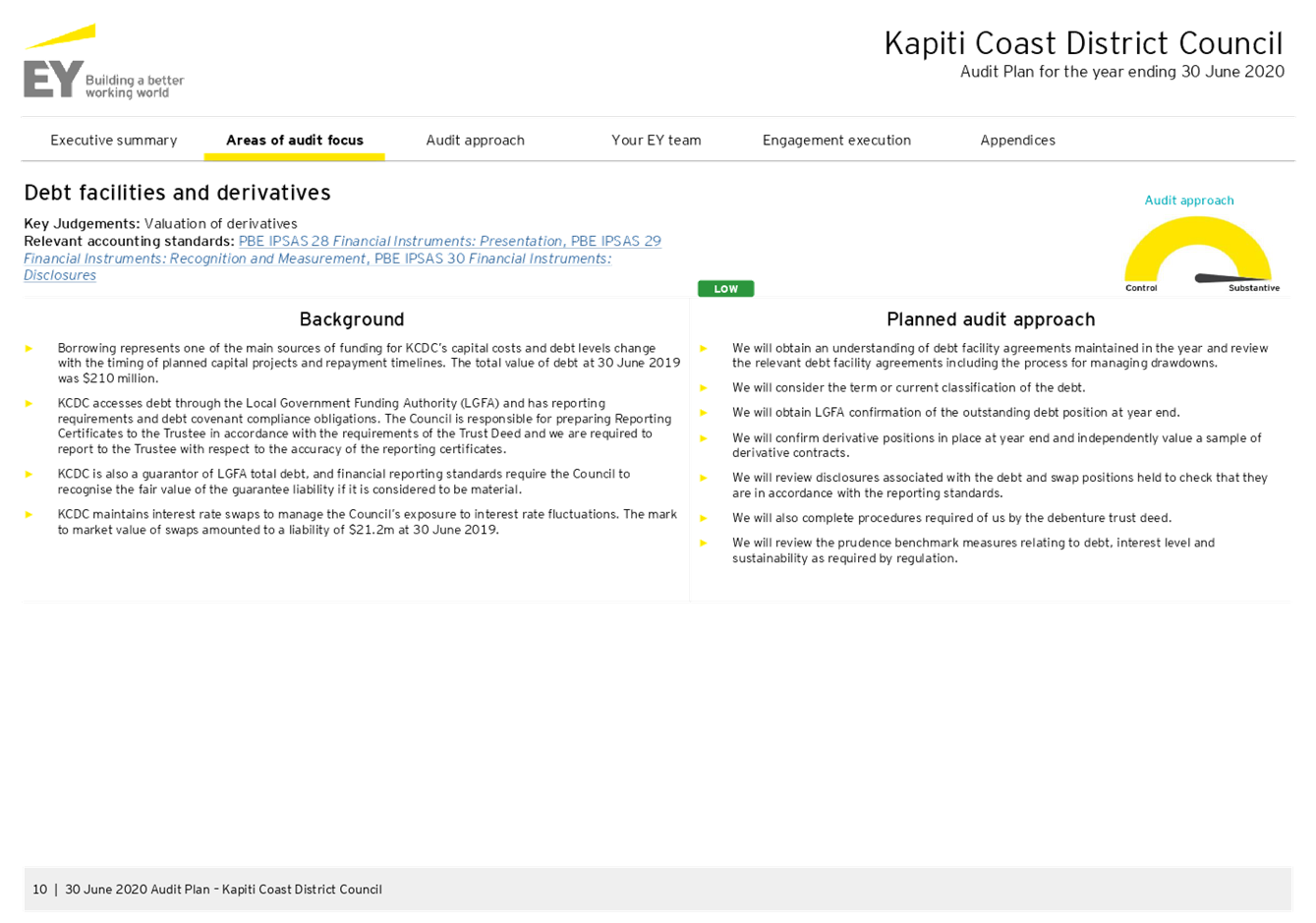

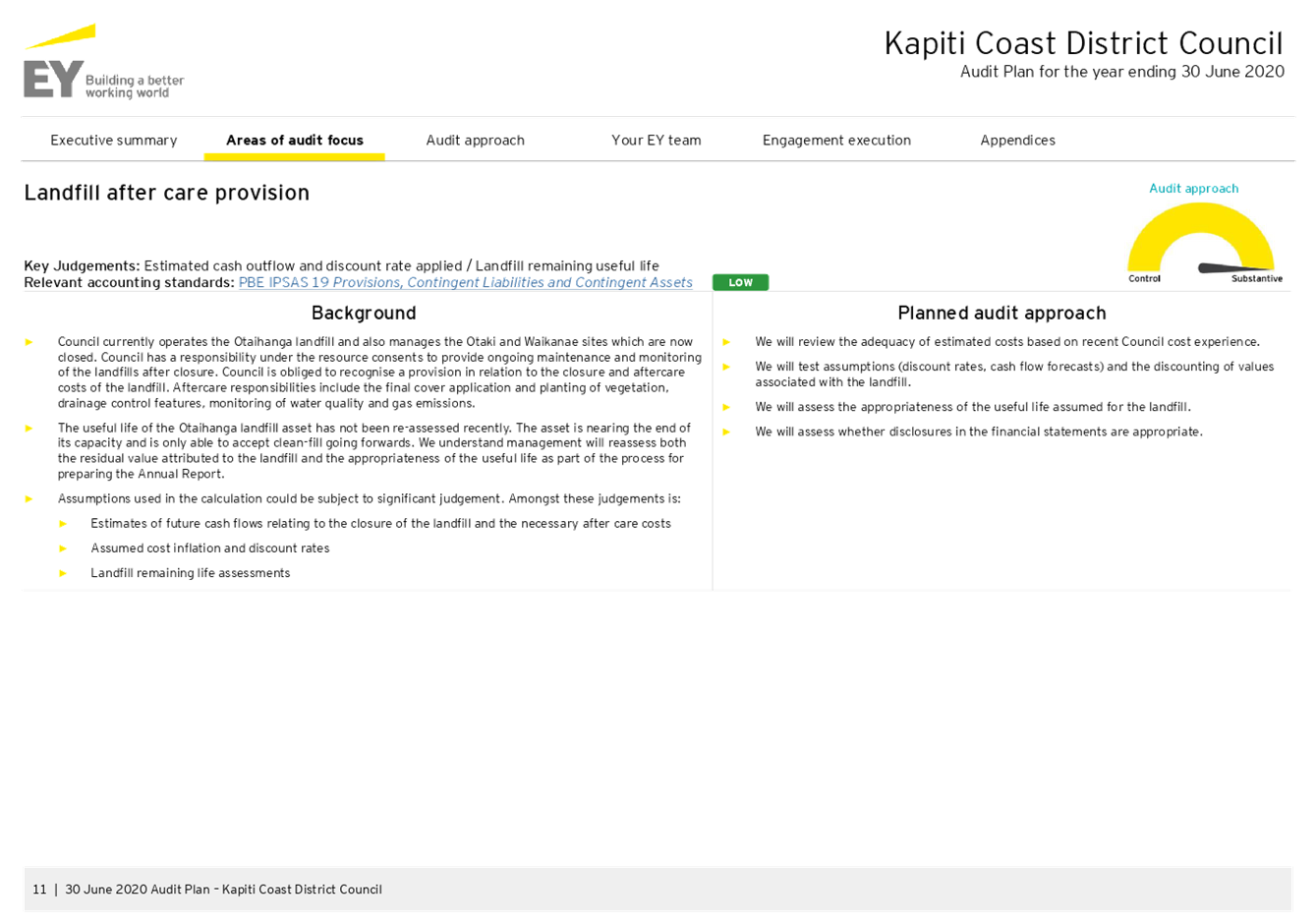

· Infrastructure

assets;

· Rates

setting, rates invoicing and collection;

· Non-financial

performance reporting;

· New

Zealand Transport Agency (NZTA) subsidies;

· Expenditure,

procurement and tendering;

· Debt

facilities and derivatives; and

· Landfill

aftercare provision

Materiality

6 Audit

has set their materiality threshold at $1.7 million, being 2% of forecast

expenditure. Materiality is broadly defined as the quantum of any misstatements

(through error or otherwise), that would likely mislead users of the financial

statements. Any identified misstatements impacting on Council’s operating

result by more than $90,000 will be reported to the Subcommittee by way of

Audit’s Closing Report on conclusion of their audit.

Policy

considerations

7 There

are no policy implications arising from this report.

Legal

considerations

8 There

are no legal issues arising from this report.

Financial

considerations

9 The

total audit fees payable to Ernst & Young for the year ended 30 June 2020

are estimated to be $188,400 plus GST. This fee includes the audit of the

2019/20 Annual Report ($185,200, including reasonable disbursements) and

Council’s compliance with its Debenture Trust Deed ($3,200) for the year

ended 30 June 2020. Provision for this audit fee has been included in the

2019/20 Annual Plan.

Tāngata

whenua considerations

10 There

are no tāngata whenua considerations arising from this report

Significance and Engagement

Significance

policy

11 This

matter has a low level of significance under the Council’s Significance

and Engagement Policy.

Publicity

12 There

are no specific publicity considerations arising from this report.

|

Recommendations

13 That

the Audit and Risk Subcommittee receives and notes the Ernst & Young

Audit Plan for the year ended 30 June 2020 attached as Appendix 1 to this

report.

|

Appendices

1. Ernst

and Young Audit Plan for the year ended 30 June 2020 ⇩

|

Audit

and Risk Sub-committee Meeting Agenda

|

20 February 2020

|

8.3 Timetable

for the Audit Plan for the year ended 30 June 2020

Author: Anelise

Horn, Manager Financial Accounting

Authoriser: Mark

de Haast, Group Manager

Purpose of Report

1 This

report updates the Audit and Risk Subcommittee on the proposed timetable for

the audit of Council’s Annual Report and Debenture Trust Deed for the

year ended 30 June 2020.

Delegation

2 The

Audit and Risk Subcommittee has delegated authority to consider this report

under the following delegation in the Governance Structure, Section C.1.

· Confirming

the terms of engagement for each audit with a recommendation to the Council;

and receiving the external audit reports for recommendation to the Council.

· Obtaining

from external auditors any information relevant to the council’s

financial statements and assessing whether appropriate action has been taken by

management in response to the above.

Background

3 The

Auditor-General is the auditor of all ‘public entities’, including

the Kāpiti Coast District Council.

4 Under

section 32 and 33 of the Public Audit Act 2001, the Auditor General has

appointed Ernst & Young to carry out the annual audit of the

Council’s financial statements and performance information for the years

ending 30 June 2020 to 30 June 2022.

5 Fees

for the audit of public entities are set by the Auditor General under section

42 of the Public Audit Act 2001.

6 The

nature and scope of these audit engagements are set out in the Letters of

Engagement as approved by Council, the Council’s auditors, Ernst &

Young and the Council’s Trustee, Covenant Trustee Services. The latter is

only applicable to the audit of the Debenture Trust Deed.

CONSIDERATIONS

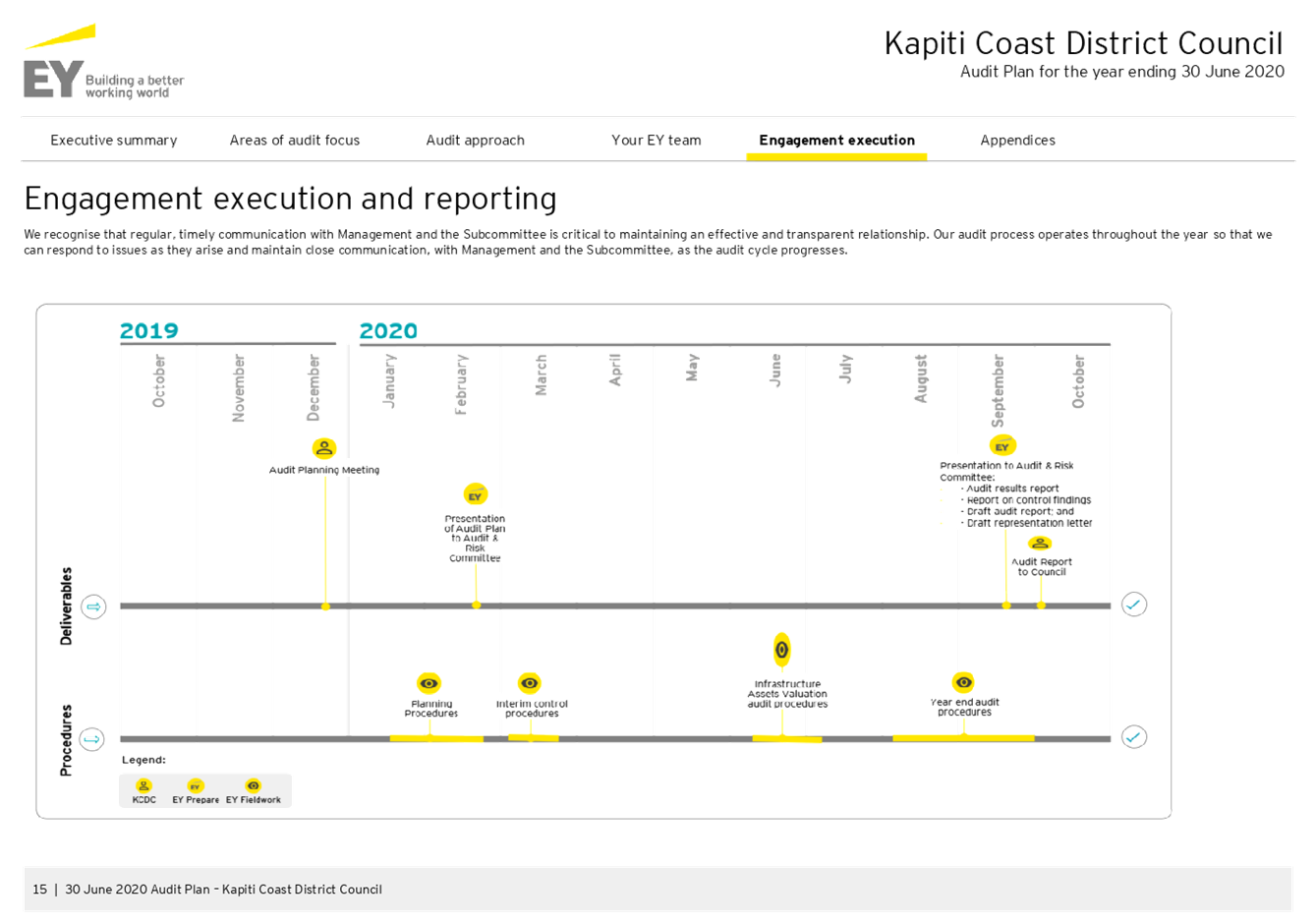

Audit Plan for the year ended 30 June 2020

7 Ernst

& Young is presenting their audit plan for the audit of the 2019/20 annual

report to the Audit and Risk Subcommittee at this meeting. (refer to Ernst and

Young Audit Plan for the year ended 30 June 2020)

Audit Approach

8 Following

agreement with Ernst & Young, the audit of the Council’s financial

statements and non-financial information for the year ended 30 June 2020 will

be completed in two separate stages. Stage one comprises an audit of the

revaluation of the infrastructure assets and stage two comprises an audit of

the financial statements, non-financial performance information and a full

review of the draft 2019/20 Annual report.

9 Stage

one includes:

Property, plant and equipment

(PPE) is the largest and most complex asset category on the balance sheet and a

separate audit stage is allocated to the revaluation of infrastructure assets.

Based on councils annual rolling

asset revaluation programme, Council is revaluing the following asset classes

as at 31 March 2020:

· Land and buildings

(including land under roads)

· Parks and reserves

structures

· Water, wastewater

and stormwater (including seawalls and river control)

The valuation of infrastructure

assets is judgemental and there are a number of key assumptions that the

independent valuer is required to make, based on their experience and

expertise, that have the potential to materially impact the resulting asset values.

For this reason, the audit of the asset revaluation will be done in isolation

of the other financial statement elements and is scheduled to take place from

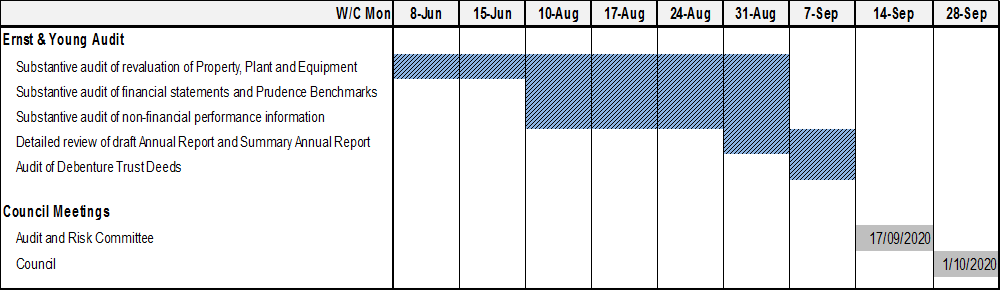

Monday 8 June 2020 to Friday 19 June 2020.

10 Stage

two includes:

· A

substantive audit of the draft financial statements (including a draft

financial overview and a draft Report Disclosure Statement (Prudence

Benchmarks)).

· A

substantive audit of the non-financial performance information (service

performance measures).

· A

detailed review of the draft Annual Report and Summary Annual Report for the

year ended 30 June 2020.

· The

audit of the Debenture Trust Deed for the year ended 30 June 2020.

This is

scheduled to take place from Monday 10 August 2020 to Friday 11 September 2020.

2019/20

Annual Report adoption timetable

11 The

table below sets out the scheduled meeting dates of the Audit and Risk

Subcommittee, and Council meetings that are relevant to the adoption of the

2019/20 Annual Report.

12 Agenda

items relevant to the 2019/20 Annual Report have been outlined.

|

Meeting of…

|

Meeting Date

|

Agenda Items to

include…

|

|

Audit and Risk Subcommittee

|

Thursday

20 February 2020

|

For Review and feedback:

1. Ernst

and Young’s audit plan for the audit of the 2019/20 annual report.

|

|

Audit and Risk Subcommittee

|

Thursday 17 September 2020

|

For

Information:

1. Ernst

and Young’s Closing Report to the Audit and Risk Subcommittee for the

year ended 30 June 2020.

2. Ernst

& Young’s Report on Control Findings for the year ended 30 June

2020.

For Decision:

3. Review

and recommend adoption of the 2019/20 Annual Report to Council.

|

|

Council

|

Thursday

1 October 2020

|

For Decision

1. Adopt

the 2019/20 Annual Report.

|

13 The

table below summarises the combined timings of both the audit process and the

Council meetings at which the audit outputs are tabled for information and or

decision-making purposes, which will result in the adoption of the Annual

Report.

Summary table of audit processes

and related Council meetings:

Considerations

Policy considerations

14 There

are no policy considerations at this stage.

Legal

considerations

15 There

are no legal considerations at this time.

Financial

considerations

16 The

total audit fees payable to Ernst & Young for the year ended 30 June 2020

are estimated to be $188,400 plus GST. This fee includes the audit of the

2019/20 Annual Report ($185,200, including reasonable disbursements) and

Council’s compliance with its Debenture Trust Deed ($3,200) for the year

ended 30 June 2020. This audit fee is included in the 2019/20 Annual Plan.

17 In

addition to the above, the Debenture Trust Deed requires the Council to

complete a full audit of its debt/security stock register. Council has engaged

PricewaterhouseCoopers (PWC), the auditors of Computershare (the registrar), to

complete this audit. The fee for this service is $750 (inclusive of GST).

Similarly, this fee is included in the 2019/20 Annual Plan.

Tāngata

whenua considerations

18 There

are no tāngata whenua considerations.

Significance and Engagement

Significance

policy

19 This

matter has a low level of significance under the Council’s Significance

and Engagement Policy.

Publicity

20 There

are no publicity considerations at this stage.

|

Recommendations

21 That

the Audit and Risk Subcommittee notes the timetable for the audit of the

Council’s Annual Report and the Council’s Debenture Trust Deed

for the year ended 30 June 2020.

|

Appendices

Nil

8.4 Update

on key 2018-19 Audit Findings

Author: Anelise

Horn, Manager Financial Accounting

Authoriser: Mark

de Haast, Group Manager

Purpose of Report

1 This

report provides the Audit and Risk Subcommittee with a progress update regards

Ernst & Young’s Report on Control Findings for the year ended

30 June 2019.

Delegation

2 The

Audit and Risk Subcommittee has delegated authority to consider this report

under the following delegation in the Governance Structure, Section C.1.

· Reviewing

and maintaining the internal control framework.

Obtaining from external auditors any

information relevant to the Council’s financial statements and assessing

whether appropriate action has been taken by management in response to the

above.Background

3 In

accordance with New Zealand Auditing Standards, Ernst & Young (Audit)

performed a review of the design and operating effectiveness of the

Council’s significant financial reporting processes as part of their

audit for the year ended 30 June 2019.

4 Control

risk matters and/or issues are classified as high, moderate or low. Control

risk definitions are as follows:

· High

Risk – matters and/or issues are considered to be fundamental to the

mitigation of material risk, maintenance of internal control or good corporate

governance. Action should be taken either immediately or within three months.

· Moderate Risk –

matters and/or issues are considered to be of major importance to maintenance

of internal control, good corporate governance or best practice for processes.

Action should normally be taken within six months.

· Low Risk – A weakness which does

not seriously detract from the internal control framework. If required, action

should be taken within 6 -12 months.

5 Audit

identified eight control risk issues for the year ended 30 June 2019, ranging

from low to moderate risk rankings. The table at the end of the report, details

the year to date progress against these control findings.

6 In

keeping with standard practice, Audit will consider whether these control

findings can be closed-out, as part of their audit for the year ended 30 June

2020.

Considerations

Policy

considerations

7 There

are no policy implications arising from this report.

Legal

considerations

8 There

are no legal considerations arising from this report.

Financial

considerations

9 Financial

issues have been covered as part of this report.

Tāngata

whenua considerations

10 There

are no tāngata whenua considerations arising from this report.

Significance and Engagement

Significance

policy

11 This

matter has a low level of significance under the Council’s Significance

and Engagement Policy.

Publicity

12 There

are no publicity considerations.

|

Recommendations

13 That

the Audit and Risk Subcommittee notes the progress update in regards to Ernst

& Young’s Report on Control findings for the year ended 30 June

2019 and that Ernst & Young will re-assess these as part of their audit

for the year ended 30 June 2020.

|

Appendices

Nil

Summary

of Control Findings for the year ended 30 June 2019

|

1.

Service requests - Accuracy of response and resolution times (Moderate)

|

|

Target date for completion and current status

|

31/03/2020

On track with manual reviews. System upgrade likely

to take longer.

|

|

Ernst & Young Audit

Observation

|

In completing our testing

of performance reporting information we identified multiple instances where

the response and resolution times used as a basis for calculating measures

were inconsistent with the times indicated on job sheets that were completed

for those jobs by the staff attending to the request.

One

particular issue we observed that occurred for multiple items tested was

requests being marked as responded to or resolved too early. This was

observed for both water supply and waste water when measuring response or

resolution times to urgent and non-urgent requests. This is primarily the

result of the first action logged in response to the request being treated as

either KCDC having responded to, or resolved, the matter when in actual fact

the action was a step towards either responding to, or resolving, the matter.

Since a number of performance measures

require reporting of response or resolution times discrepancies in the time

recorded will lead to incorrect outcomes being reported. Whilst this has

implications for Council’s non-financial performance reporting it also

impacts management’s ability to understand the team’s responsiveness

to ratepayer requests and any resourcing or process issues that may need to

be remedied to allow timely responses to requests.

|

|

EY Audit Recommendation

|

Requests logged in Council’s system

should be reviewed on a periodic basis to ensure the time to respond to, or

resolve, matters is being accurately reflected in the system.

|

|

Action Plan

|

We

agree with the observation. The MagiQ system allows multiple actions to be

recorded against a service request. In some cases, the final response

time is recorded on the second or later action. Our analysis found

that, although the correct response time is being entered in the system, the

automatic reports used to calculate the response time measures only capture

the time that the first action is completed. This has meant that in

cases when the final response time is not when the first action is completed,

the calculations of median response time are being made incorrectly.

The

issues have been documented and several solution options will be investigated

further:

· Re-design the service request system and

data capture process, to allow for reports to accurately calculate the

correct median response time. This is the most robust and long-term

solution, but would be the most complex to implement.

· Adopt a workaround whereby staff ensure

that only the first action can be used for the resolving action, allowing

existing reports to calculate the median response time accurately.

· Continue the current practice of cleaning

the report data manually to ensure that the measure is reported accurately,

but undertake this on a more regular basis throughout the year as recommended

above. This is a short-term solution that does not fix the root cause

of the problem. However, in advance of a more sustainable solution

being implemented, a review and cleaning of the first two months of data for

FY19/20 is already underway.

Responsibility:

Manager Corporate Planning and

Reporting and Chief Information Officer

|

|

Progress Update

|

Data from the first quarter of the 19/20 year has

been fully reviewed to ensure

that both the response and/or resolution times to service request matters is

being accurately reflected in the system. This will be repeated during the 2019/20

financial year to ensure that the

time to respond to, or resolve matters is being accurately reflected in the

system.

Manual reviews of the data are time consuming and

work is continuing to explore a re-design of the service request system and

data capture process to allow for reports to accurately calculate the correct

median response time.

|

|

2. Service requests - Monitoring of roading requests for service

(Moderate)

|

|

Target date for completion and current status

|

31/03/2020

On track with manual reviews. System upgrade likely

to take longer.

|

|

Ernst & Young Audit

Observation

|

For the

access and transport measure relating to the Council’s response time to

requests for service for roads and footpaths Council were unable to

accurately determine if requests for service had been responded to within the

target timeframes. The information for this measure is sourced from two

separate systems, MagiQ which holds the details of requests, and RAMM which

holds the details of work and actions undertaken. The primary issue is that

there is insufficient clarity of how some requests in MagiQ can be linked to

actions taken recorded in RAMM.

Because requests for service in MagiQ are

unable to be fully mapped to work undertaken recorded in RAMM, Council is

unable to report an outturn for the year against this target. The issue also

limits Council’s ability to measure responsiveness from the perspective

of managing operations and considering performance on a regular basis and how

resource should be allocated.

|

|

EY Audit Recommendation

|

We recommend that work is

completed to improve the interfacing or flow of data between these two

systems. Alternatively work completed could be recorded in MagiQ against each

of the relevant requests for service.

|

|

Action Plan

|

Investigative

work will be needed to determine the best way forward to accurately measure

response time to service requests for road and footpath work. The ideal would

be an automated flow of data between MagiQ and RAMM where the interface is

seamless and error-free. However, if that proves unattainable we will

have to look at establishing systems to achieve manual updates of service

request response time information from RAMM to MagiQ at the same time that

completion times are entered into MagiQ from RAMM. This may require

additional consistency checks between the two databases to ensure that

request types and priority assignments are the same in the two systems so

that response time targets are equivalent. At first glance this appears to be

a substantial piece of work and will probably exceed the recommended

six-month timeframe.

Responsibility:

Chief Information Officer and

Manager Corporate Planning and Reporting

|

|

Progress Update

|

Council’s road maintenance

contractor has identified a solution to automate service requests data from

Council’s MagiQ system into RAMM to ensure the data is consistent

across both systems. Currently this is a one-way data transfer, and solutions

to enable two-way data transfer are being investigated.

Data is currently being manually reviewed

as the two-way automatic data transfer is still likely to take several months

to implement.

|

|

Audit

and Risk Sub-committee Meeting Agenda

|

20 February 2020

|

|

3. Service requests – Duplicate

requests for services (Low)

|

|

Target date for completion and current status

|

30/06/2020

On track

|

|

Ernst & Young Audit

Observation

|

When

reviewing requests for service data for the water supply and wastewater

management activities we identified duplicate requests for service for the

same matter. In some instances, requests for service were closed with zero

response times if they were confirmed as duplicates. This has an impact on

median response times through reducing this measure incorrectly.

We also noted instances where

Council initiated requests for service for planned work and these were

included in the calculation of median response times. The request for service

based metrics are primarily intended to measure response times to ratepayer

requests as opposed to Council’s internal work program.

Duplicate

requests included in the system impact the reported results especially in

instances where duplicates have a response time set to zero and have been

included in the calculation of the median.

The inclusion of requests

for service from Council employees means the measures become less focused on

Council’s responsiveness to ratepayer requests.

|

|

EY Audit Recommendation

|

We recommend implementing

controls that prevent duplicate requests for service being recorded in the system.

Alternatively, a periodic review of requests within the system could be

undertaken to identify and remove duplicate requests. The same review could

ensure Council generated requests are clearly labelled as such and excluded

from the calculation of the measure.

|

|

Action Plan

|

We agree

with the observation.

Several

solution options will be investigated further in conjunction with the

response in 2.1.1:

1. Re-design

the service request system and data capture process, to ensure that duplicate

requests, internal requests, planned work, and other non-applicable requests

can be excluded from the calculation of the performance measure.

2. Continue

the current practice of cleaning the report data manually to ensure that the

measures are reported accurately, but undertake this on a more regular basis

throughout the year as recommended above.

As noted in

2.1.1, we have already begun a review and cleaning of the report data for

FY19/20. As well as correcting the response times, this task also

includes removing duplicates and non-applicable service requests from the

calculated median response times.

Responsibility:

Manager Corporate Planning and

Reporting, and Chief Information Officer

|

|

Progress Update

|

Data from the first quarter of the 19/20 year has

been fully reviewed for

duplicate service requests to ensure that both the response and/or resolution

times to service request matters is being accurately reflected in the system. Similarly, this will be repeated

during the 2019/20 financial year to ensure that the time to respond to, or resolve matters is being

accurately reflected in the system.

Similar to above, work is continuing to explore a

re-design of the service request system and data capture process, (including

removing any duplicate requests), to allow for reports to accurately

calculate the correct median response time.

|

|

4.

Service requests – Manual reorganisation of requests for services (Low)

|

|

Target date for completion and current status

|

30/06/2020

On track

|

|

Ernst & Young Audit

Observation

|

To calculate

outcomes for some measures data was extracted from the system and put through

a further manual process to determine the category of the request. This

involved adjusting the category of the request per the system and then

calculating the measure to be reported based on the excel spreadsheet with

updated categorisations.

We

identified instances where information extracted from the system subjected to

further manual categorisation was incorrectly categorised affecting the

reported results. For example, requests for service that did not relate to

the particular activity or urgency categorisation were included in

calculating the outcome for that measure.

We also identified

instances where subsequent to information being extracted from the system

changes were made to the information in the system and the associated

spreadsheet wasn’t updated to reflect these changes. Because the

measures are calculated based on the data in the spreadsheet this results in

information relevant to the request for service being excluded.

Incorrect categorisation

of data could lead to measures being incorrectly calculated.

|

|

EY Audit Recommendation

|

We recommend that

processes be updated to allow for correct classification of requests for

service at the point the requests are received. If this is impractical we

would suggest that requests for service be reviewed on a periodic basis and

reclassified within the system when a reclassification is required.

|

|

Action Plan

|

The points

above appear to refer to the current system for assessing and reporting on

Stormwater and Coastal service requests.

We agree

that this system should be amenable to significant improvement.

However, following our own analysis we have further characterised the issue:

Firstly,

our understanding is that ‘instances where information extracted

from the system subjected to further manual categorisation was incorrectly

categorised affecting the reported results’ relates to two separate

matters;

i) Where instances of service requests

related to stormwater outlets were included in calculations of the Coastal

measure for ‘Urgent requests to repair sea walls or rock

revetments’ when they should only be accounted for in the Coastal

measure for ‘Stormwater beach outlets are kept clear’. This has

been fixed in the current reporting and is a straightforward fix even in the

existing ‘manual’ spreadsheet method of reporting on Coastal KPI

measures.

ii) There were three instances of stormwater

service requests (out of 89) which were classified as urgent in error. This

error rate is unlikely to be improved by adopting the suggestion that ‘processes

be updated to allow for correct classification of request for service at the

point requests are received’. Requests are received at the

call centre for the most part and staff often either a) do not have

sufficient or accurate enough information from the caller to correctly

classify the request, or b) do not have the experience to be able to do so.

This is why we rely on a subsequent, secondary, classification process by our

stormwater team, who occasionally make errors.

Secondly,

it was identified that ‘instances where subsequent to information

being extracted from the system changes were made to the information in the

system and the associated spreadsheet wasn’t updated to reflect these

change’. It isn’t clear how many instances of this were

found but to our knowledge there weren’t many and we expect they would

be largely immaterial to the measures being reported on or the response time

calculations. Many of the changes made to request types subsequent to data

being extracted from the system do not have any material bearing on the

secondary categorisation made by the stormwater team and to revisit MagiQ on

a regular basis to update these would be both time-consuming and probably not

very productive.

A full

improvement solution to MagiQ to enable it to generate more stream-lined and

efficient Coastal and Stormwater service request reporting will take

significant investigation and discussion with both MagiQ, regarding the

system’s capabilities, and the Coastal and Stormwater team, regarding

their requirements. We envisage the following:

i) introducing a pro-forma report that

doesn’t require manual set-up each week and only needs date ranges

entered to provide the appropriately filtered list of service requests each

week.

ii) ideally, we would then like to see

enhancements to the system so that there are a range of drop-down or

pick-list categories that the Coastal and Stormwater team can use for

providing secondary and tertiary categorisations to each service request (so

that this is done in MagiQ rather than on a separate spreadsheet). This

categorisation process would include categorisations as to which service

requests are Coastal or Stormwater requests, and further to that which are

urgent/non-urgent, council/private issues, affect buildings/or don’t

etc

iii) if such improvements are feasible then

when that secondary categorisation process is complete each week a report

should be able to be generated from MagiQ which generates the equivalent of

the current Stormwater and Coastal service request spreadsheets.

This

approach would significantly improve the efficiency of the current process

and improve the audit trail. It would not remove the human judgement

factor behind the categorisation process as that is how the categorisations

are currently made in MagiQ in any case. We would need to investigate whether

there is an efficient process for checking whether subsequent changes to

categorisations of service requests not initially identified as relevant for

Coastal or Stormwater reporting purposes have, as a result of a

re-categorisation in MagiQ, become relevant for those purposes.

This will

be a significant piece of work and will need to be undertaken in concert with

the planned upgrade to MagiQ and other proposed improvements recommended to

improve reporting of actual resolution times and avoidance of counting

duplicate service requests in those calculations.

Responsibility:

Manager

Corporate Planning and Reporting, and Chief Information Officer

|

|

Progress Update

|

Work is continuing to explore a re-design of the

service request system and data capture process, (including removing any

duplicate requests) that will include solutions (i) and (iii) above as well.

The additional categorisation proposed at (ii) above

may require external resource from MagiQ and may take longer to complete.

|

|

5.

Corporate policies due for review (Low)

|

|

Target date for completion and current status

|

30/06/2020

On-track

|

|

Ernst & Young Audit

Observation

|

We

observed various employee manuals and policy documents were last updated over

3 years ago. Specifically, we noted the below policies are currently overdue

for review and update:

a. Receipt

of gifts and hospitality

b. Rewards

and recognition policy

c. Mitigation

of fraud

d. Employee

code of conduct

e. Elected

member code of conduct

Policies and other guidance documents should be

updated on a regular basis to ensure any changes in circumstances that

require additional guidance are incorporated on a timely basis.

|

|

EY Audit Recommendation

|

We recommend that

corporate policies be monitored and updated on a regular basis.

|

|

Action Plan

|

We accept

the findings and recommendation from audit. The register of corporate

policies, including review dates, will be updated and monitored by Corporate

Services going forward as part of the wider policy programme.

Responsibility:

Manager

Research and Policy, Corporate Services

|

|

Progress Update

|

The Research and Policy team are currently developing

a programme of work to review, update and maintain Corporate Policies.

|

|

6.

Timeliness of purchase order initiation (Low)

|

|

Target date for completion and current status

|

30/06/2020

On-track

|

|

Ernst & Young Audit

Observation

|

During our testing of the expenditure and payments

process we observed that some purchase orders were generated subsequent to

the receipt of invoices.

Without adequate controls for processing and

reconciling purchase orders, invoices and the receipt of goods and services

there is an increased risk inappropriate or erroneous expenditure is incurred

or reported. A purchase

order system works most effectively when purchase orders are approved prior

to goods or services being purchased. After the transaction has occurred

there may be less opportunity to change the agreement that has been entered

into.

|

|

EY Audit Recommendation

|

We recommend purchase

orders are raised and appropriately approved prior to placing orders with

suppliers.

|

|

Action Plan

|

Management

accepts the recommendation and is currently working on a programme for

induction and increased training for staff to ensure there is a consistent

high standard of compliance with the Procurement Policy across all areas of

the Council. The Finance team worked with the suppliers during the

2018/19 year to highlight the importance of requesting an EPO number from

Council before beginning any work.

Responsibility:

Chief Financial

Officer

|

|

Progress Update

|

Council-wide procurement training continues and the

Finance team are actively providing one-on-one EPO training for new staff

members.

Furthermore, Council is currently investigating how

technology can be used more effectively in the supplier payment space through

automation of the accounts payable function. A Request for Proposal (RFP) was

issued in January 2020 with full implementation of the selected solution

targeted by 30 June 2020.

Automation will strengthen the discipline of

initiating an EPO when the goods or services are ordered as the EPO number

will be a key field on the supplier invoice required by the payment solution.

|

|

7.

Approval of expenditure (Low)

|

|

Target date for completion and current status

|

30/06/2020

On-track

|

|

Ernst & Young Audit

Observation

|

KCDC’s

General Expenses policy states “one-up authorisation must be given to

the person who will benefit or might be perceived to benefit from the

expenditure.”

We noted two instances where an expense

claim was either authorised by a person who was not one up from the

individual that incurred the cost or was not one up from the most senior

individual that benefited or might be perceived to have benefited from the

expenditure. In both instances we are satisfied that the expenditure was

appropriate but have recommendations regarding the execution of the relevant

controls.

This may increase the risk

that inappropriate expenditure goes undetected.

This policy also serves to safeguard

staff in that in instances where they may have been perceived to have

benefited from Council expenditure an independent member of staff has

concurred with their judgement that the costs are appropriate.

|

|

EY Audit Recommendation

|

We recommend that

expenses incurred are approved in a manner that is in line with KCDC’s

policies

|

|

Action Plan

|

Management

accepts the findings and recommendation from Audit. Corporate Services will

seek to increase Council-wide access to and awareness of all corporate

policies

Responsibility:

Chief Financial

Officer

|

|

Progress Update

|

The Accounts Payable team are manually reviewing

each expense claim submitted for payment to ensure that it has been approved

in accordance with the general expense policy. If not, the claim is reverted

to the relevant staff members to be corrected.

The General Expense policy is included in the

programme of work being developed by the Research and Policy team to review,

update and maintain Corporate Policies.

|

|

8.

Review of useful life of landfill asset (Low)

|

|

Target date for completion and current status

|

30/06/2020

On-track

|

|

Ernst & Young Audit

Observation

|

The useful life of the Otaihanga landfill

asset has not been thoroughly re-assessed recently. The asset is nearing the

end of its capacity and is only able to accept clean-fill going

forwards. There is currently an asset recorded on balance sheet for the

Otaihanga landfill that has a residual useful life spanning a number of

years. If the landfill is near to the end of its useful life and the asset

has limited remaining value the residual useful life used for accounting

purposes may need to be reduced or the value attributed to the asset may need

to be decreased.

|

|

EY Audit Recommendation

|

The

current useful life of the landfill suggests that benefit will continue to be

derived from the landfill over a number of years going forward. We recommend

that Council consider the nature and timing of the expected benefits from the

landfill and use this as context for evaluating if the current useful life is

still appropriate and if Council is likely to receive future benefit from the

landfill that broadly equates to the current carrying value of the landfill

asset.

|

|

Action Plan

|

Management

accepts the findings and will assess the economic life of the asset during

the 2019/20 year.

Responsibility:

Chief Financial

Officer

|

|

Progress Update

|

The

economic life of the Otaihanga landfill asset is scheduled to be reviewed in

April 2020.

|

8.5 Quarterly

Treasury Compliance Report

Author: Anelise

Horn, Manager Financial Accounting

Authoriser: Mark

de Haast, Group Manager

Purpose of Report

1 This

report provides confirmation to the Audit and Risk Subcommittee of the

Council’s compliance with its Treasury Management Policy (Policy) for the

six months ended 31 December 2019.

Delegation

2 The

Audit and Risk Subcommittee has delegated authority to consider this report

under the following delegation in the Governance Structure, Section C.1.

Ensuring that

the Council has in place a current and comprehensive risk management framework

and making recommendations to the Council on risk mitigation.

Background

3 The

Policy sets out a framework for the Council to manage its borrowing and

investment activities in accordance with the Council’s objectives and

incorporates legislative requirements.

4 The

Policy mandates regular treasury reporting to management and the Strategy and

Operations Committee, as well as quarterly compliance reporting to the Audit

and Risk Subcommittee.

5 In

order to assess the effectiveness of the Council’s treasury management

activities and compliance to the Policy, certain performance measures and

parameters have been prescribed. These are:

· cash/debt

position;

· liquidity/funding

control limits;

· interest

rate risk control limits;

· counterparty

credit risk;

· specific

borrowing limits; and

· risk

management performance.

6 Given

this is the first Audit and Risk Subcommittee meeting for this triennium, this

report covers the compliance reporting for both the first quarter (July to

September) and the second quarter (October to December) of the 2019/2020

financial year.

discussion

Cash/Debt Position

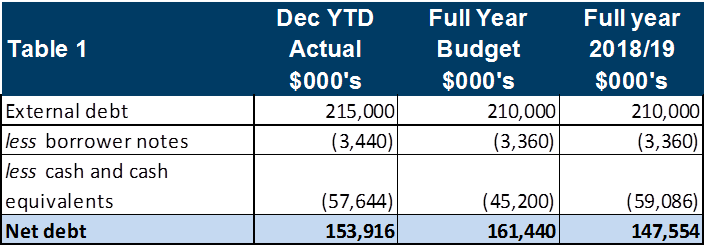

7 Table

1 below shows the Council’s net debt position as at 31 December 2019 against

the 2019/20 full year budget and the prior year closing balance.

8 During

the past six months, the Council has issued $25 million of new debt towards

prefunding the April 2020, October 2020 and May 2021 debt maturities. The funds

were placed on term deposit, at the most favourable market rates available at

that time, as part of the Council’s prefunding programme.

9 During

the same period, $20 million of long term debt matured during September 2019.

This was fully funded through the Council’s prefunding programme and was

repaid from term deposits maturing on the day.

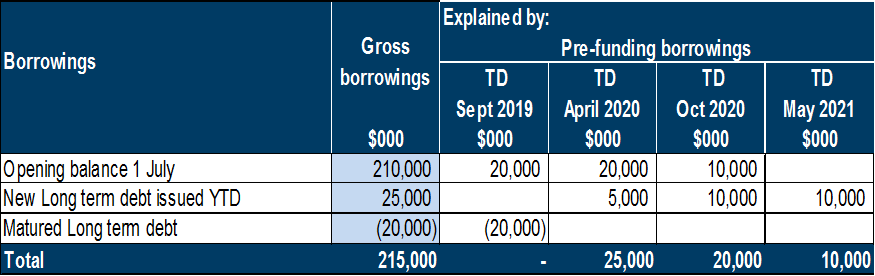

10 The

table below shows (a) the movement in the Council’s external debt balance

and (b) the movement in the Council’s pre-funding programme by debt

maturity, for the six months ended 31 December 2019.

11 As

at 31 December 2019, the Council had $61.08 million of cash, term deposits and

borrower notes on hand, and relates mainly to the Council’s debt

pre-funding programme. This is broken down as follows:

12 The

Council is targeting through its financial strategy to keep net borrowings

below 200% of total operating income. At 31 December 2019, the Council is

forecasting its net borrowings to be 185.8% of total operating income at 30

June 2020.

13 For

the six months ended 31 December 2019, the Council has not breached its net

debt upper limit, as shown in the chart below:

Liquidity/Funding control limits

14 Liquidity

and funding management focuses on reducing the concentration of risk at any

point so that the overall borrowings cost is not increased unnecessarily and/or

the desired maturity profile is not compromised due to market conditions. This

risk is managed by spreading and smoothing debt maturities and establishing

maturity compliance buckets.

15 Since

October 2015 the Council’s treasury strategy has included a debt

pre-funding programme. The Policy allows pre-funding of Council debt maturities

up to 18 months in advance, including re-financing. Market conditions have been

favourable for this approach, where the Council draws down debt early and is

able to invest the funds on term deposit for a positive net return.

16 The

debt pre-funding programme was highlighted by Standard & Poor’s

(S&P) in their July 2019 review, where Council’s credit rating was

upgraded from A+ to AA with S&P noting the Council’s exceptional

liquidity coverage.

17 The

following graph presents the Council’s debt maturity dates in relation to

the financial year in which the debt was issued. This demonstrates that since

2016/17, the Council has actively reduced risk concentration by spreading debt

maturity dates and debt maturity values.

18 Debt

maturities must fall within maturity compliance buckets. These maturity buckets

are as follows:

|

Maturity

Period

|

Minimum

|

Maximum

|

|

0 to

3 years

|

10%

|

70%

|

|

3 to

5 years

|

10%

|

60%

|

|

5 to

10 years

|

10%

|

50%

|

|

10

years plus

|

0%

|

20%

|

19 For

the 6 months ending 31 December 2019, the Council has been fully compliant with

its debt maturity limits, as shown by the chart below. The upper limits, as

shown by dashed lines, relate to the bars of the same colour. For example, the

0 to 3 year upper limit of 70% is in blue. Actual maturities in the 03 year

bucket are represented by the blue bars. The Council has no long term debt

maturing in ten years’ time or beyond.

Interest rate risk control limits

20 The

Council issues all debt on a floating rate basis, as lower interest rates are

realised this way, and uses fixed interest rate swaps (hedges) to minimise

exposure at any one time to interest rate fluctuations. This ensures more

certainty of interest rate costs when setting our annual plan and long term

plan budgets.

21 Without

such hedging, the Council would have difficulty absorbing adverse interest rate

movements. A 1% increase in interest rates on $215 million in net debt would

equate to additional interest expense of $2.15 million per annum. Conversely,

fixing interest rates does however reduce the Council’s ability to benefit

from falling and/or more favourable interest rate movements.

22 The

objectives of any treasury strategy are therefore to smooth out the effects of

interest rate movements, while being aware of the direction of the market, and

to be able to respond accordingly.

23 The

Policy sets out the following interest rate limits:

Major control limit where

the total notional amount of all interest rate risk management instruments

(i.e. interest rate swaps) must not exceed the Council’s total actual

debt, and;

Fixed/Floating Risk Control

limit, that specifies that at least 55% of Council’s borrowings must be

fixed, up to a maximum of 100%.

24 The

table below shows the Council’s hedging value for the six months ending

31 December 2019.

25 The Policy Fixed/Floating Risk Control

Limit was briefly breached during the month of September 2019. This breach

occurred because planned debt pre-funding of $5 million was not issued. This

has since been corrected and the debt pre-funding programme is closely

monitored by Council Officers.

26 Similar to debt maturities, hedging

instrument maturities must also fall within maturity compliance buckets.

These maturity compliance buckets are as follows:

|

Period

|

Minimum

|

Maximum

|

|

1 to

3 years

|

15%

|

60%

|

|

3 to

5 years

|

15%

|

60%

|

|

5 to

10 years

|

15%

|

60%

|

|

10

years plus

|

0%

|

20%

|

27 The

Council has been fully compliant for the six months ended 31 December 2019, as

shown by the following chart. Note that maturities falling within 1 year are

not included.

Counterparty Credit Risk

28 The

policy sets maximum limits on transactions with counterparties. The purpose of

this is to ensure the Council does not concentrate its investments or risk

management instruments with a single party.

30 The

policy sets the gross counter party limits as follows:

31 The

Council was in full compliance with all counterpart credit limits for the six

months ended 31 December 2019. The tables below show the Council’s

investments and risk management instruments holdings per counterparty during

the quarter.

Term deposits

*Policy Limit: 60% of total investments or $25 million;

whichever is greater

Interest rate

swaps

*Policy

Limit: 50% of total instruments or $80 million; whichever is greater

Specific Borrowing Limits

32 In

managing debt, the Council is required to adhere to the limits below. The

Council fully complied with these limits for the six months ended 31 December

2019 (or a period as otherwise specified) and the results are shown below:

Risk Management Performance

33 The

following table shows the Council’s interest income and expense for the

year to date, along with the weighted average cost of borrowing (WACB)

34 Council’s

net interest cost year to date is $181,00 favourable to budget. This is mainly

due to a lower external borrowings balance at the start of the 2019/20

financial year than planned.

35 Council

has been effective in its treasury management with its weighted average cost of

funds being 0.51% lower that budget as at the 31 December 2019.

36 The

following graph shows the cost of borrowing each month.

Considerations

Policy

considerations

37 There

are no policy considerations other than those already noted in this

report.

Legal

considerations

38 There

are no legal considerations arising from this report.

Financial

considerations

39 There

are no financial considerations other than those already noted in this

report.

Tāngata

whenua considerations

40 There

are no tāngata whenua considerations arising from this report.

Significance and Engagement

Significance

policy

41 This

matter has a low level of significance under Council’s Significance and

Engagement Policy.

Publicity

42 There

are no publicity considerations arising from this report.

|

Recommendations

43 That

the Audit and Risk Subcommittee notes the Council’s compliance with its

Treasury Management Policy for the six months ended 31 December 2019.

|

Appendices

Nil

8.6 Ombudsman

Investigation into Christchurch City Council LGOIMA Practices

Author: Tim

Power, Senior Legal Counsel

Authoriser: Mark

de Haast, Group Manager

Purpose of Report

1 The

purpose of this report is to update the Subcommittee on the Council’s

compliance with its obligations under the Local Government Official Information

and Meetings Act (LGOIMA) following concerns raised by the Chief Ombudsman over

compliance in the sector.

2 An

internal self-review has been undertaken of Council’s LOGIMA

practices. The report does not identify any major areas of concern but

does note some areas where the Council could improve its processes.

Delegation

3 The

Audit and Risk Subcommittee has the appropriate delegation to consider this

report and recommendations under the Governance Structure C1:

· Reviewing

and maintaining the internal control framework.

BackgrounD

4 The

Chief Ombudsman has been monitoring agencies’ official information

practices, resources and systems by undertaking targeted investigations and

publishing reports of findings. Several local authorities have been the

subject of a targeted investigation. Most recently an investigation into

Christchurch City Council (CCC) identified a number of serious concerns about

the Council’s leadership and culture, and its commitment to openness and

transparency. A number of recommendations were made in the

Ombudsman’s report. A copy of the Executive Summary of the

Ombudsman’s report is attached as Appendix 1 to this report.

5 A

full copy of the report can be found by accessing the following link:

https://www.ombudsman.parliament.nz/resources/lgoima-compliance-and-practice-christchurch-city-council

Issues and Options

Issues

6 The

Chief Ombudsman’s investigation of CCC looked at how the Council dealt

with requests for official information, produced Land Information Memoranda

(LIM) reports, and whether Council meetings complied with LGOIMA requirements.

7 The

information gathered during the investigation was considered against a

framework consisting of the following areas:

· Leadership

and culture

· Organisation

structure, staffing and capability

· Internal

policies, procedures and resources

· Current

practices

· Performance

monitoring and learning

Leadership

and culture

8 CCC

staff raised concerns about the methods used by the Executive Leadership Team

(ELT) to keep negative information about the Council from Elected Members

and/or the public. The alleged methods included manipulating or removing

information from reports, project reporting not occurring, and staff being told

not to record information or to keep information in draft form.

9 The

investigation found the former CCC Chief Executive failed to take adequate and

appropriate action to address staff concerns and to ensure the actions of the

ELT reflected the LGOIMA’s principle of availability and the commitment

to openness and transparency.

10 The following

recommendations were made:

· All

staff should be encouraged to identify process improvements and receive

training in accordance with their position.

· Review

the delegations’ framework to ensure decision making and accountability

at the senior level are clear.

· Develop

a proactive release policy to support the Council’s commitment to

transparency.

· Establish

a process to ensure any amendments made to documents/records are

transparent.

· Establish

a clear process for staff reporting and raising concerns without fear of

reprisal, and ensure outcomes are clearly communicated back to staff.

· Regular

consistent positive messaging by the CE and ELT about the importance of

openness and transparency.

· Assign

a senior manager with specific strategic responsibility and executive

accountability for official information practice.

Organisation

structure, staffing and capability

11 The report noted

that it is essential that LGOIMA training is mandatory for all staff upon

induction, with refresher training offered periodically to staff who handle

information requests.

12 The following

recommendations were made:

· Develop

a LGOIMA training programme tailored to the needs of all staff.

· Develop

and implement more detailed, regular training for delegated decision makers,

including senior leaders and staff in the LGOIMA team.

· Ensure

appropriate staff have access to, and understand how to use, the LGOIMA

tracking spreadsheet to ensure feedback is available.

Internal

policies, procedures and resources

13 While CCC had

internal guidance material for staff, the report noted that it is important to

ensure the guidance is consistent across the different platforms within

Council. While the policies existed, it was important to ensure they were

adhered to, and senior leaders needed to champion the importance of those

policies.

14 The following

recommendations were made:

· Ensure

guidance is reviewed regularly and updated.

· Leaders

to champion sound record keeping practice.

· Prioritise

the development of a proactive release policy.

Current

practices

15 The report noted

that a number of requests received by the CCC customer services team were not

recorded as LGOIMA requests. CCC used a spreadsheet that recorded the

relevant information associated with each request. However, the

spreadsheet did not include information in respect of the

decision-making. Also, Elected Members directed their requests to

the CE’s Office where information was supplied on a “need to

know” basis. Staff needed to be sure that information requests made by

Elected Members were treated as LGOIMA requests.

16 The

investigation identified that an advisor to the Mayor was present while LGOIMA

requests were being discussed. CCC were encouraged to develop a protocol

to clarify when and in what circumstances decision-makers would consult with

Elected Members, including the Mayor and their staff. Any consultation

needed to be recorded.

17 The following

recommendations were made:

· Ensure

all public and media information requests are handed in accordance with LGOIMA.

· Upgrade

to a database (non-spreadsheet) to track requests and decisions.

· Record

the reasoning behind LGOIMA decisions, including any consideration of the

public interest and results of consultations with third parties.

· Establish

a peer review process.

· Ensure

records are kept of workshops and briefings.

Performance

monitoring and learning

18 CCC had internal

processes which included the ELT receiving a weekly spreadsheet of all open

LGOMIA requests and weekly meetings were held between various teams which

include LGOIMA discussions. The performance monitoring could be improved

by providing analysis of data collected in the spreadsheet, as well as

capturing additional data. The report noted that media requests were not

captured in the spreadsheet which resulted in an incomplete picture of

CCC’s compliance with LGOIMA deadlines.

19 The following

recommendations were made:

· Consider

providing the ELT with a monthly report on LGOMIA.

· Consider

ways to include requests handled by the communications and customer services

team, as well as Elected Members and property file requests, in LGOIMA reporting.

· Develop

a formal quality assurance process.

20 The report also

found that the Council generally complied with its LGOIMA obligations in terms

of time frames for responding to LIM requests, and meeting administration

requirements.

REVIEW OF KCDC’S LGOIMA PRACTICES

21 Officers have

undertaken a self-review assessment of Council’s processes, taking into

account the concerns raised and recommendations made in the CCC

investigation.

22 There are a

number of aspects of the Council’s approach to LGOIMA that Council does

well:

· Responses

are approved by Group Managers.

· Sensitive

and complex requests are all required to have Senior Legal Counsel oversight.

· Good

internal guidance is available to staff in the form of standard form templates

(staff guide available).

· Requests

are tracked in a database and assigned to staff with an automated reminder

function.

· Proactive

disclosure policy is planned (some responses have already been made publicly

available).

23 The Audit and

Risk Subcommittee receives regular reports on the status of new and current

Ombudsman investigations. The Council’s Legal Counsel has a good

relationship with the Office of the Ombudsman and a significant number of

inquiries from members of the public to the Office of the Ombudsman in relation

to the Council are resolved before they are formally recorded as a

“complaint”. In recent years there have been very few

complaints to the Office of the Ombudsman that have been upheld.

24 Council’s

processes for producing LIMs have been through a business improvement process

leading to a much more robust process for the production of LIMs with

accountabilities much clearer.

25 Council has

recently implemented changes to the manner in which records of briefings and

workshops are now captured. A record of elected members attending is now

taken and there is a recording of all workshops and briefings.

26 No issues have

been identified in relation to the notification of meetings and the publication

of agendas and issuing of minutes. For those meetings that are held in

public excluded grounds under LGOIMA are always identified. There

have been no successful challenges to grounds identified by the Council for

excluding members of the public. Council regularly release the recommendations

from public excluded meetings once the meeting has concluded.

27 Council meetings

are livestreamed and the Council is in the process of working through issues

around the proposal to make video records of meetings available to members of

the public on-line.

28 While there are

no concerns in respect of the KCDC LGOIMA processes, the CCC report has

highlighted some areas where processes could be improved, including:

· Training

for new staff at induction (and ongoing training for staff).

· Ensuring

reasons for decisions are recorded in the database. This would require

that any grounds used for withholding information are identified along with any

public interest matters that are taken into account in reaching a decision on

withholding or releasing information.

· Ensuring

that requests received through the communications and customer services teams

are captured in the LGOIMA database.

· Consideration

should be given to whether there should be any record kept of matters discussed

at public only discussions held immediately before Council meetings.

Currently no staff attend these sessions.

Considerations

Policy

considerations

25 There are no policy

considerations arising from the recommendations in this report.

Legal

considerations

26 There

are no additional legal considerations arising from this report.

Financial

considerations

27 For

the most part the recommendations in this report do not require any additional

funding and can be funded from within existing budgets. Any additional

effort required is likely to be off-set by less staff time required to deal

with LGOIMA responses that result in complaints to the Office of the Ombudsman.

Tāngata

whenua considerations

28 There

are no tāngata whenua considerations arising from this report.

Strategic

considerations

29 This

matter relates to Council’s focus outcome of improving accessibility

of Council services. By improving its LGOIMA practices, Council makes it

easier for the community to access information about Council and engage with

Council activities.

Significance and Engagement

Significance

policy

30 This

matter has a low level of significance under Council’s Significance and

Engagement Policy.

Consultation

already undertaken

31 There

has been no consultation undertaken in relation to this report and its

recommendations.

Engagement

planning

32 An

engagement plan is not needed to implement this report.

Publicity

33 No

publicity is planned in relation to this report.

|

Recommendations

34 That

the Audit and Risk Subcommittee:

(a) Notes

the CCC Ombudsman report;

(b) Notes

the areas highlighted for improvement set out in paragraph 28 to this report.

|

|

|

Appendices

1. Office

of the Ombudsman - LGOIMA Compliance and Practice at Christchurch City Council

(Executive Summary only) ⇩

|

Audit

and Risk Sub-committee Meeting Agenda

|

20 February 2020

|

8.7 Risk

Management - Business Assurance Update

Author: Jacinta

Straker, Chief Financial Officer

Authoriser: Mark

de Haast, Group Manager

Purpose of Report

1 This

report primarily updates the Audit and Risk Subcommittee on the on-going

implementation of the Enterprise Risk Management (ERM) framework.

Delegation

2 The

Audit and Risk Subcommittee has delegated authority to consider this report

under the following delegation in the Governance Structure, Section C.1.

Ensuring that Council has in

place a current and comprehensive risk management framework and making

recommendations to the Council on risk mitigation.

Background

3 The

key elements of the Enterprise Risk Management Framework include:

· Risk

Management;

· Business

Continuity Management;

· Business

Assurance; and

· Procurement

Improvement Programme.

4 The

key work streams within this area are:

· Regularly

discuss risks with the Council’s business groups and Senior Leadership

Team and embed the day-to-day management of risks in the more routine

activities;

· develop

a risk communication/reporting process at and between, the following levels:

− Council/Committees;

− Senior

Leadership Team (SLT);

− Business

Units/Groups; and

− Projects,

Asset Management.

· develop

a Business Continuity Management System for effective response to a range of

potential business disruptions;

· provide

fraud awareness training;

· provide

business assurance oversight and complete business assurance work; and

· improve

the understanding and tools to support good procurement practices.

5 As

previously reported, the intended outcomes from performing this programme well

will include:

· stakeholders,

external auditors, Council and management achieve high levels of assurance that

the real risks are being identified and managed effectively;

· better

decision making throughout the business through greater awareness of the real

risks (threats and opportunities); and

· clarification

and socialisation of the Council’s risk appetite and tolerance.

Enterprise Risk Management Progress Update

6 Guidance

for the risk management, procurement and assurance work has been established

through a collaborative process with Council staff.

7 The

work has focussed primarily on tangible outputs, as discussed separately below.

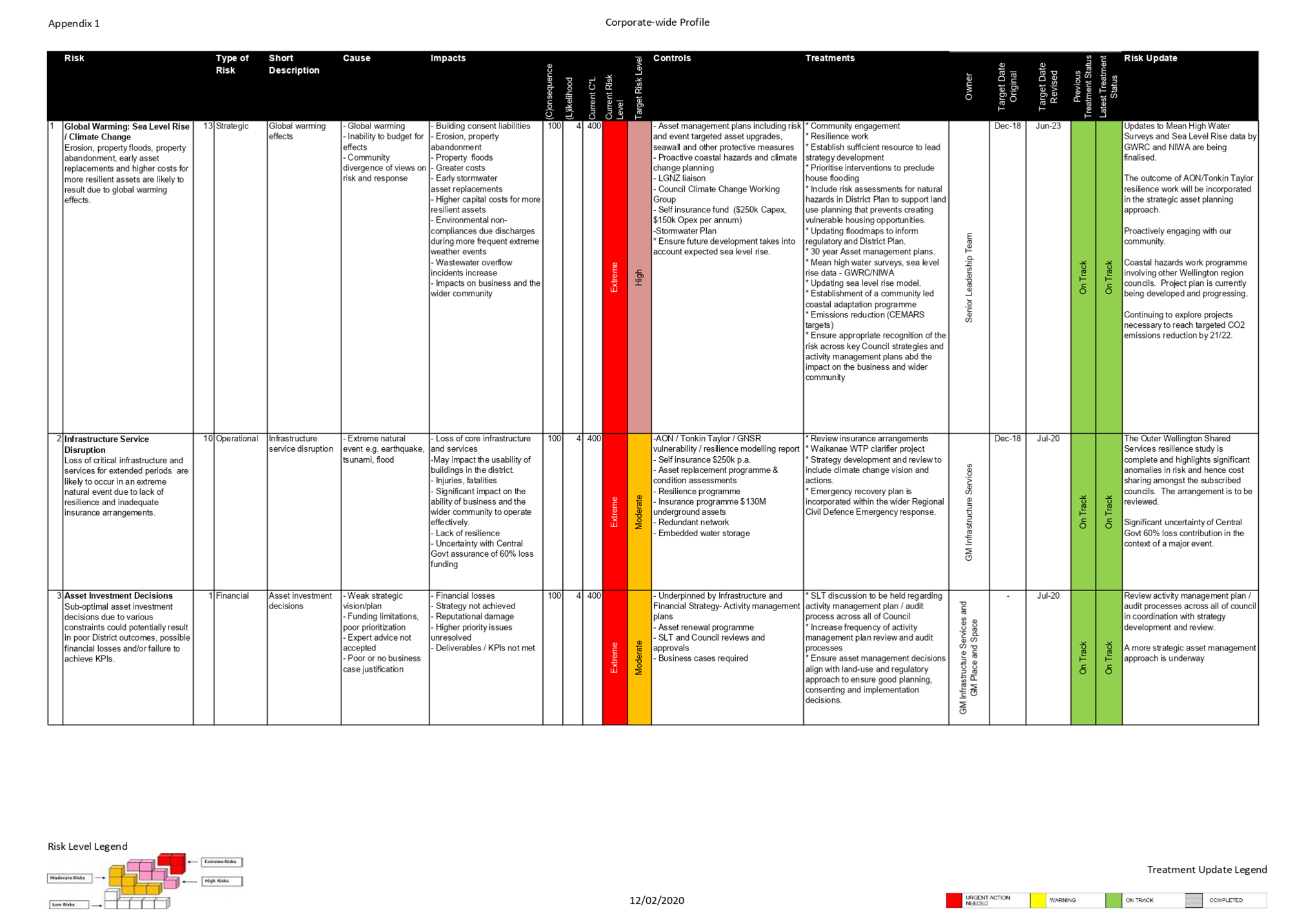

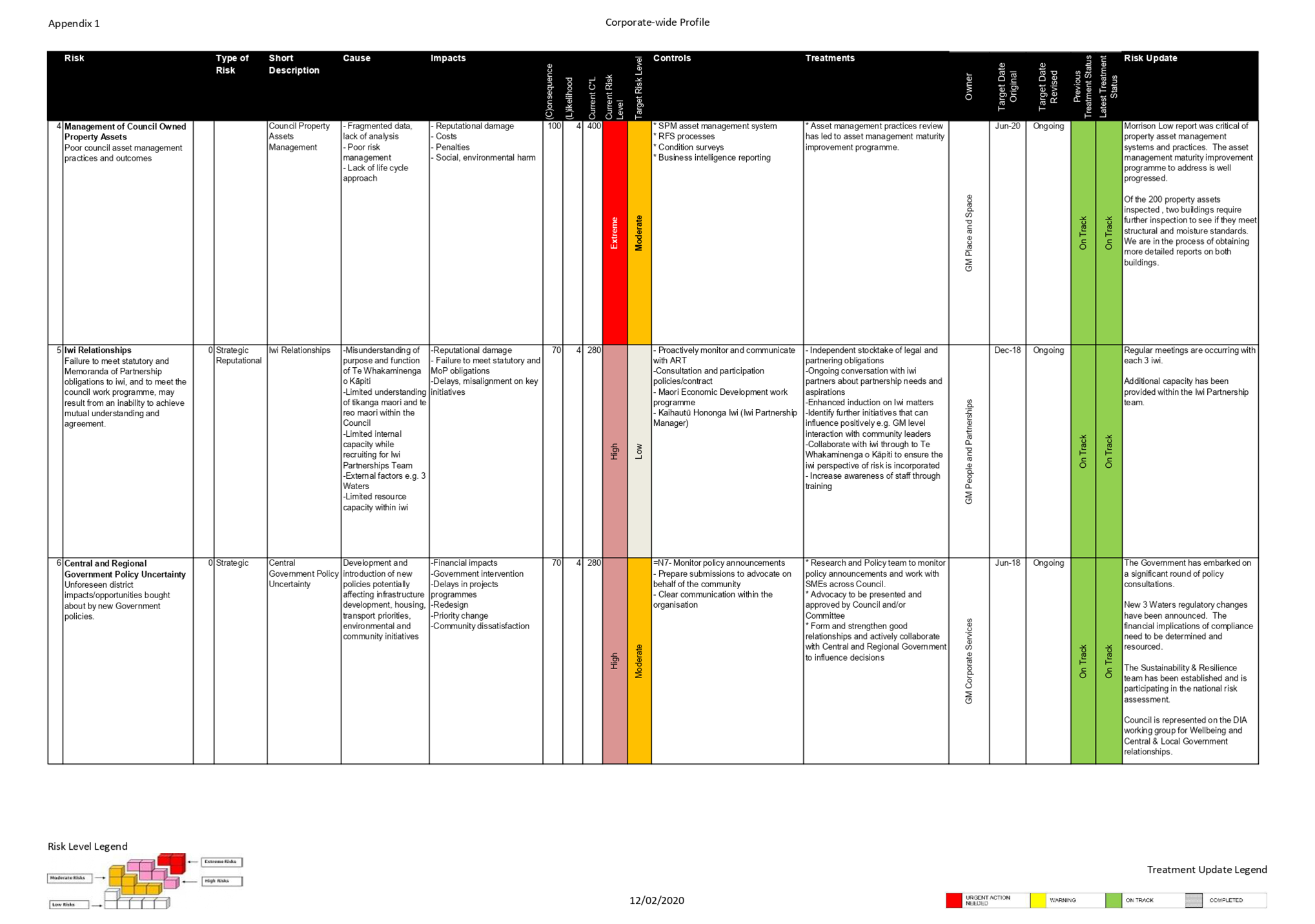

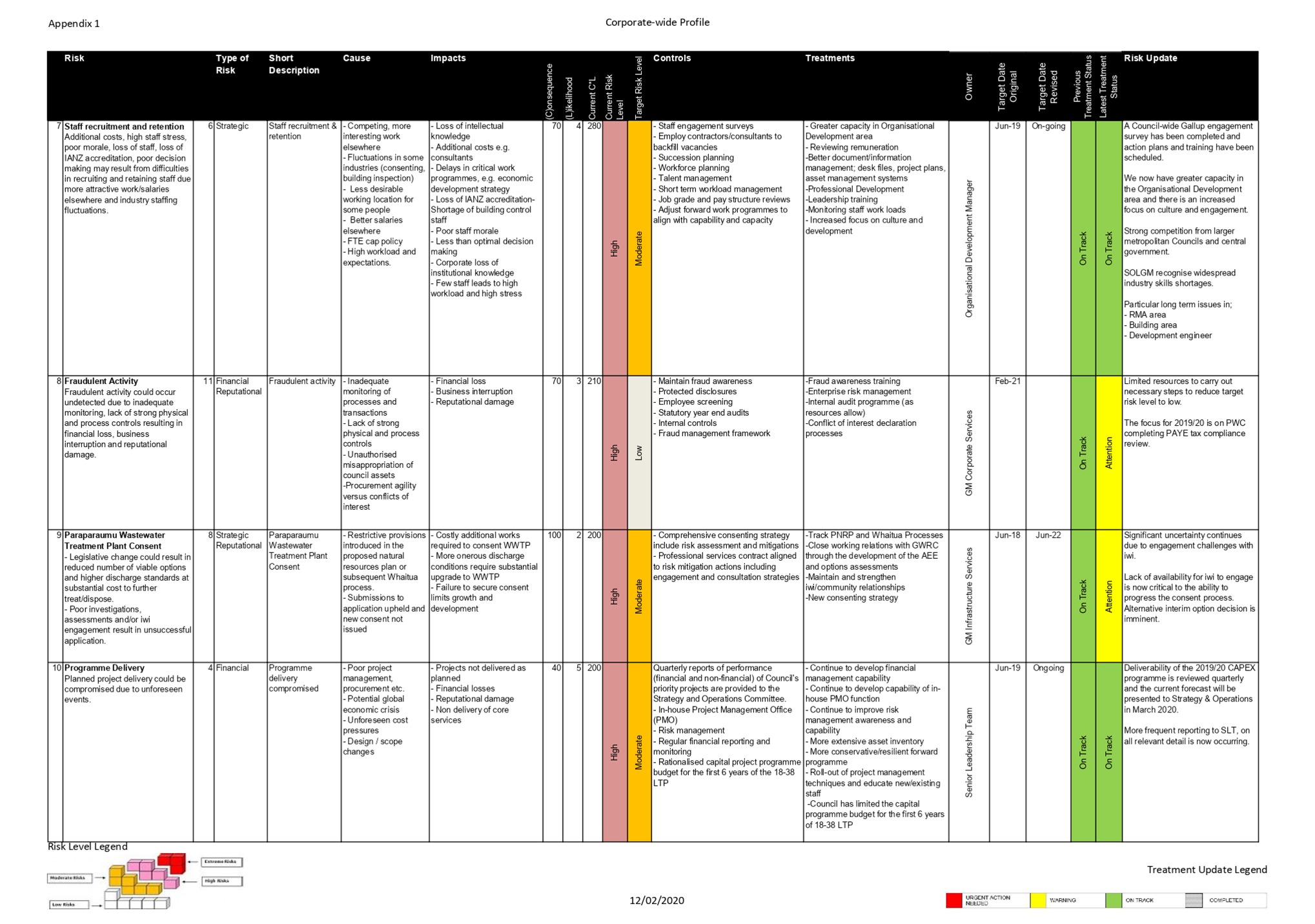

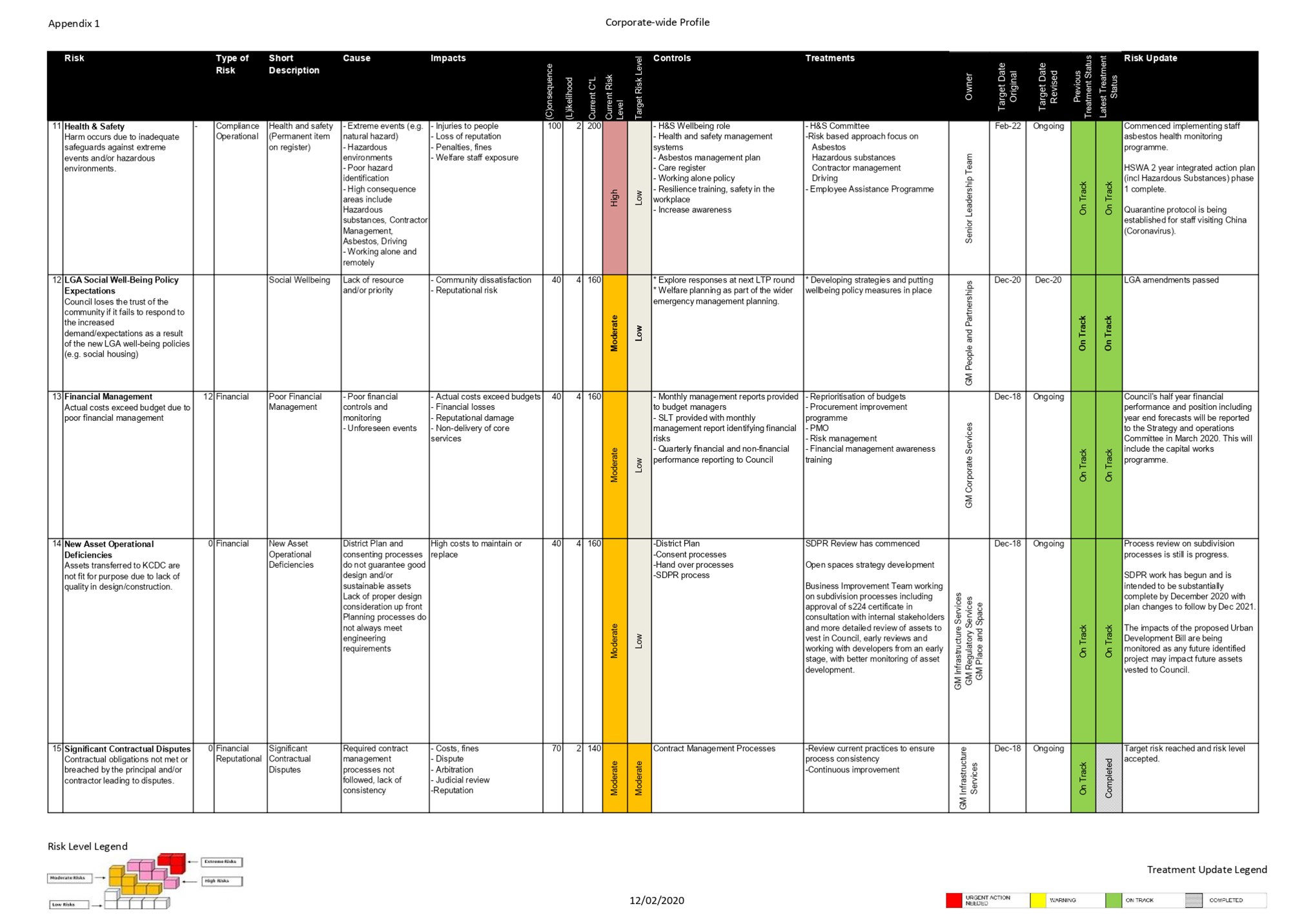

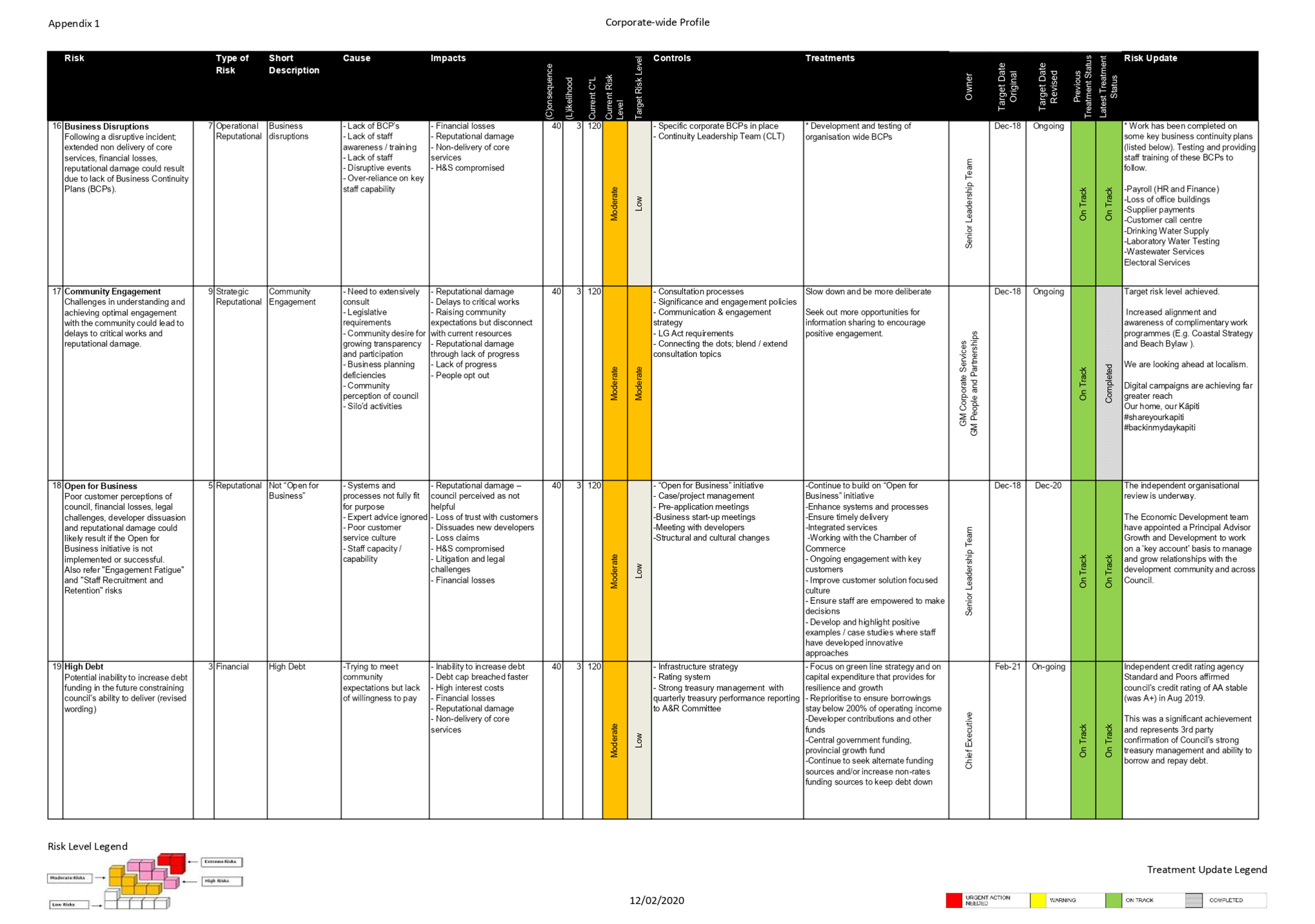

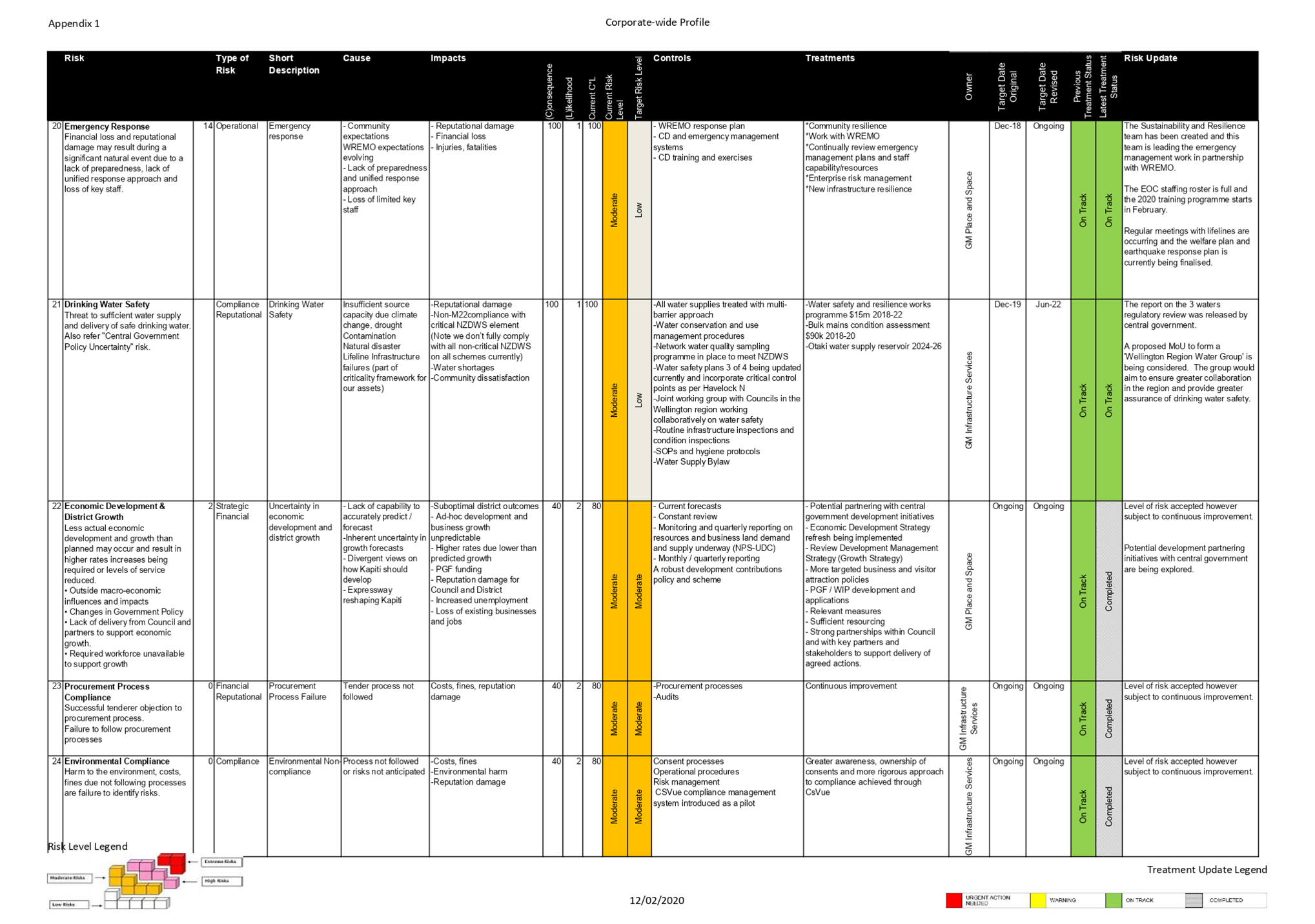

Corporate Risk Profile

– Status Update

8 As

part of Enterprise Risk Management (ERM) a risk profile, comprising a risk

register and risk treatment plan, was established. This is subject to

approximately quarterly updates by management and is then reported to the

Subcommittee. The focus is on identifying, managing and communicating the very

highest strategic and operational risks that the Council faces.

9 Engagement

on the risk profile now routinely includes conversation with activity managers

as well as Group Managers. The overall risk management culture and

practice is improving and risk conversations are widening.

10 We

are currently considering implementation of a new risk management software tool

to enable wider and efficient awareness and management of all organisational