|

|

|

AGENDA

Audit and Risk Sub-committee Meeting

|

|

I hereby give notice that a Meeting of the Audit and Risk Subcommittee will be held on:

|

|

Date:

|

Thursday, 13 August 2020

|

|

Time:

|

9.30am

|

|

Location:

|

Council Chamber

Ground Floor, 175 Rimu Road

Paraparaumu

|

|

Mark de Haast

Group Manager Corporate

Services

|

|

Audit and

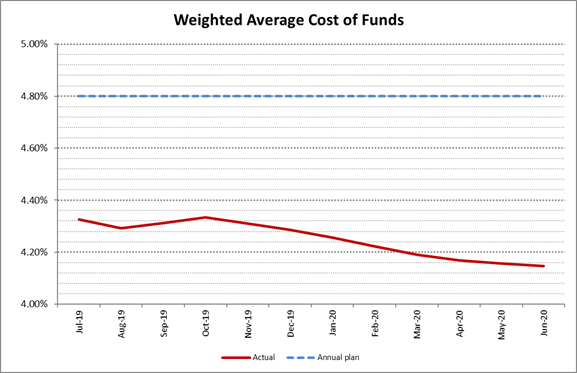

Risk Sub-committee Meeting Agenda

|

13 August 2020

|

Kapiti Coast District Council

Notice

is hereby given that a meeting of the Audit and Risk Subcommittee will

be held in the Council Chamber,

Ground Floor, 175 Rimu Road, Paraparaumu, on Thursday 13 August 2020, 9.30am.

Audit and Risk Subcommittee

Members

|

Mr Bryan

Jackson

|

Independent Chair

|

|

Mayor K Gurunathan

|

Member

|

|

Cr Angela Buswell

|

Deputy

|

|

Deputy Mayor Janet Holborow

|

Member

|

|

Cr Gwynn Compton

|

Member

|

|

Mr Gary Simpson

|

Independent

|

2 Council

Blessing

“As we deliberate on the

issues before us, we trust that we will reflect positively on the

communities we serve. Let us all seek to be effective and just, so that with

courage, vision and energy, we provide positive leadership in a spirit of

harmony and compassion.”

I a mātou e whiriwhiri ana

i ngā take kei mua i ō mātou aroaro, e pono ana mātou ka

kaha tonu ki te whakapau mahara huapai mō ngā hapori e mahi nei

mātou. Me kaha hoki mātou katoa kia whaihua, kia tōtika

tā mātou mahi, ā, mā te māia, te tiro whakamua me te

hihiri ka taea te arahi i roto i te kotahitanga me te aroha.

3 Apologies

4 Declarations

of Interest Relating to Items on the Agenda

Notification from Elected

Members of:

4.1 – any interests that

may create a conflict with their role as an elected member relating to the

items of business for this meeting, and

4.2 – any interests in

items in which they have a direct or indirect pecuniary interest as provided

for in the Local Authorities (Members’ Interests) Act 1968

5 Public

Speaking Time for Items Relating to the Agenda

6 Members’

Business

(a)

Public Speaking Time Responses

(b)

Leave of Absence

(c)

Matters of an Urgent Nature (advice to be provided to the Chair prior to

the commencement of the meeting)

7 Updates

Nil

8 Reports

8.1 Health

and Safety Quarterly Reports: 1 January 2020 - 30 March 2020; and 1 April 2020

- 30 June 2020

Author: Dianne

Andrew, Organisational Development Manager

Authoriser: Wayne

Maxwell, Chief Executive

Purpose of Report

1 This

report presents Health and Safety reports for the periods 1 January 2020

– 31 March 2020 and 1 April 2020 – 30 June 2020.

Delegation

2 The

Audit and Risk Sub Committee has delegated authority to consider this report

under the following delegation in the Governance Structure, Section C.1:

· Ensuring

that the Council has in place a current and comprehensive risk management

framework and making recommendations to the Council on risk mitigation;

· Assisting

elected members in the discharge of their responsibilities by ensuring

compliance procedures are in place for all statutory requirements relating to

their role;

· Governance

role in regards to the Health and Safety Leadership Charter and Health and Safety

Plan.

Background

3 The

quarterly Health & Safety Performance Report is intended to provide the

Council with insight into initiatives and activities, and their progress, as

part of our organisations commitment to providing a safe and healthy place to

work. The contents and any subsequent discussions arising from this report can

support Council officers to meet their due diligence obligations under the

Health & Safety at Work Act (HSWA) 2015.

4 Between

July and September 2017 the Simpson Grierson Health and Safety team were

engaged to review how the Council was progressing with changes and planned

initiatives following the introduction of the Health and Safety at Work Act

(HSWA) 2015. The findings were presented back to the Audit and Risk Committee

in November 2017. This review identified areas for improvement, in particular

where we can improve some current processes to further strengthen our ability

to more effectively monitor and verify.

5 A

draft Health and Safety Plan 2018 – 2020 was provided to the Committee at

the meeting 13 September 2018 and has since been adopted by the Senior

Leadership Team.

6 Progress

on the 2018 – 2020 Health and Safety Plan has been incorporated into

quarterly reports going forward.

7 Two

reports are presented at this time due to the business interruptions as a

result of the Covid19 pandemic impact on ‘business as usual’.

Issues and Options

Issues

8 Progress

on the Health and Safety 2018-2020 Plan initiatives is progressing however the

alert level 4 and alert level 3 restrictions severely disrupted planned health

and safety related initiatives and training. Several time lines may be extended

and this will be updated through the reporting cycle.

Considerations

Policy

considerations

9 There

are no Policy considerations.

Legal considerations

10 There

are no legal considerations.

Financial

considerations

11 Budget

has been provided for implementation of the action plan initiatives as part of

the 2018-38 Long Term Plan.

Tāngata

whenua considerations

12 There

are no Tāngata whenua considerations.

Significance and Engagement

Significance

policy

13 This

report does not trigger the Council’s Significance and Engagement Policy.

Publicity

14 There

are no publicity considerations.

|

Recommendations

15 That

the Audit and Risk Sub Committee notes the two Health and Safety Quarterly

Reports for the periods: 1 January 2020 – 31 March 2020; and 1 April

2020 – 30 July 2020 attached as Appendix One and Appendix Two to this

Report.

|

Appendices

1. Appendix

One - H&S Quarterly Report Jan-March 2020 ⇩

2. Appendix

Two - H&S Quarterly Report April-June 2020 ⇩

|

Audit

and Risk Sub-committee Meeting Agenda

|

13 August 2020

|

|

Audit and Risk Sub-committee Meeting Agenda

|

13 August 2020

|

8.2 Update

on key 2018-19 Audit Findings

Author: Anelise

Horn, Manager Financial Accounting

Authoriser: Mark

de Haast, Group Manager Corporate Services

Purpose of Report

1 This

report provides the Audit and Risk Subcommittee with a progress update regards

Ernst & Young’s Report on Control Findings for the year ended

30 June 2019.

Delegation

2 The

Audit and Risk Subcommittee has delegated authority to consider this report

under the following delegation in the Governance Structure, Section C.1.

· Reviewing

and maintaining the internal control framework.

Obtaining from external auditors any

information relevant to the Council’s financial statements and assessing

whether appropriate action has been taken by management in response to the

above.Background

3 In

accordance with New Zealand Auditing Standards, Ernst & Young (Audit)

performed a review of the design and operating effectiveness of the

Council’s significant financial reporting processes as part of their

audit for the year ended 30 June 2019.

4 Control

risk matters and/or issues are classified as high, moderate or low. Control

risk definitions are as follows:

· High

Risk – matters and/or issues are considered to be fundamental to the

mitigation of material risk, maintenance of internal control or good corporate

governance. Action should be taken either immediately or within three months.

· Moderate Risk –

matters and/or issues are considered to be of major importance to maintenance

of internal control, good corporate governance or best practice for processes.

Action should normally be taken within six months.

· Low Risk – A weakness which does

not seriously detract from the internal control framework. If required, action

should be taken within 6 -12 months.

5 Audit

identified eight control risk issues for the year ended 30 June 2019, ranging

from low to moderate risk rankings. The table at the end of the report, details

the year to date progress against these control findings.

6 Unfortunately,

some of the planned work programmes to fully address Audit’s 2018/19

control findings have been delayed due to the Covid-19 restrictions.

7 As

part of their audit for the year ended 30 June 2020, Audit will consider this

progress update and in doing so, Audit will assess whether any existing control

findings can be formally closed-out.

Considerations

Policy

considerations

8 There

are no policy implications arising from this report.

Legal

considerations

9 There

are no legal considerations arising from this report.

Financial

considerations

10 Financial

issues have been covered as part of this report.

Tāngata

whenua considerations

11 There

are no direct tāngata whenua considerations arising from this report.

Significance and Engagement

Significance

policy

12 This

matter has a low level of significance under the Council’s Significance

and Engagement Policy.

Publicity

13 There

are no publicity considerations.

|

Recommendations

14 That

the Audit and Risk Subcommittee notes the progress update in regards to Ernst

& Young’s Report on Control findings for the year ended 30 June

2019 and that Ernst & Young will re-assess these as part of their audit

for the year ended 30 June 2020.

|

Appendices

Nil

Summary

of Control Findings for the year ended 30 June 2019

|

1.

Service requests - Accuracy of response and resolution times (Moderate)

|

|

Target date for completion and current status

|

31/03/2020

Complete

|

|

Ernst & Young Audit Observation

|

In completing our testing

of performance reporting information we identified multiple instances where

the response and resolution times used as a basis for calculating measures

were inconsistent with the times indicated on job sheets that were completed

for those jobs by the staff attending to the request.

One

particular issue we observed that occurred for multiple items tested was

requests being marked as responded to or resolved too early. This was

observed for both water supply and waste water when measuring response or

resolution times to urgent and non-urgent requests. This is primarily the

result of the first action logged in response to the request being treated as

either KCDC having responded to, or resolved, the matter when in actual fact

the action was a step towards either responding to, or resolving, the matter.

Since a number of performance measures

require reporting of response or resolution times discrepancies in the time

recorded will lead to incorrect outcomes being reported. Whilst this has

implications for Council’s non-financial performance reporting it also

impacts management’s ability to understand the team’s

responsiveness to ratepayer requests and any resourcing or process issues

that may need to be remedied to allow timely responses to requests.

|

|

EY Audit Recommendation

|

Requests logged in Council’s system

should be reviewed on a periodic basis to ensure the time to respond to, or

resolve, matters is being accurately reflected in the system.

|

|

Action Plan

|

We

agree with the observation. The MagiQ system allows multiple actions to be

recorded against a service request. In some cases, the final response

time is recorded on the second or later action. Our analysis found

that, although the correct response time is being entered in the system, the

automatic reports used to calculate the response time measures only capture

the time that the first action is completed. This has meant that in

cases when the final response time is not when the first action is completed,

the calculations of median response time are being made incorrectly.

The

issues have been documented and several solution options will be investigated

further:

· Re-design the service request system and

data capture process, to allow for reports to accurately calculate the

correct median response time. This is the most robust and long-term

solution, but would be the most complex to implement.

· Adopt a workaround whereby staff ensure

that only the first action can be used for the resolving action, allowing

existing reports to calculate the median response time accurately.

· Continue the current practice of cleaning

the report data manually to ensure that the measure is reported accurately,

but undertake this on a more regular basis throughout the year as recommended

above. This is a short-term solution that does not fix the root cause

of the problem. However, in advance of a more sustainable solution

being implemented, a review and cleaning of the first two months of data for

FY19/20 is already underway.

Responsibility:

Manager Corporate Planning and

Reporting and Chief Information Officer

|

|

Progress Update

|

In March 2020, we activated new fields on the Service

Request form to capture service

restored date and time which the Operations team are now using. The

median response time reports have been rewritten so they now calculate the

resolution KPI measures using the time elapsed from the date and time of

receipt to the date and time of service restored. This avoids the

previous risk of errors when calculating the resolution time by excluding the

action completed times from any calculation. The new field is included

on hard copy SR forms and in the MagiQ system. We have retrospectively

completed this field for SRs from July 2019 to March 2020 to ensure the data

is consistent for the full 2019/20 year.

The new report also excludes the following

requests:

· private site requests (coded as ‘Not

Council issue’).

· requests where no fault was found (coded

as ‘Not Council issue’).

· requests generated by staff (coded as internal

requests) per control finding 3 below.

|

|

2. Service requests - Monitoring of roading requests for service

(Moderate)

|

|

Target date for completion and current status

|

31/03/2020

Proposed solution in operation, testing in

progress.

|

|

Ernst & Young Audit

Observation

|

For the

access and transport measure relating to the Council’s response time to

requests for service for roads and footpaths, Council were unable to

accurately determine if requests for service had been responded to within the

target timeframes. The information for this measure is sourced from two

separate systems, MagiQ which holds the details of requests, and RAMM, which

holds the details of work and actions undertaken. The primary issue is that

there is insufficient clarity of how some requests in MagiQ can be linked to

actions taken recorded in RAMM.

Because requests for service in MagiQ are

unable to be fully mapped to work undertaken and recorded in RAMM, Council is

unable to report an outturn for the year against this target. The issue also

limits Council’s ability to measure responsiveness from the perspective

of managing operations and considering performance on a regular basis and how

resource should be allocated.

|

|

EY Audit Recommendation

|

We recommend that work is

completed to improve the interfacing or flow of data between these two

systems. Alternatively work completed could be recorded in MagiQ against each

of the relevant requests for service.

|

|

Action Plan

|

Investigative

work will be needed to determine the best way forward to accurately measure

response time to service requests for road and footpath work. The ideal would

be an automated flow of data between MagiQ and RAMM where the interface is

seamless and error-free. However, if that proves unattainable we will

have to look at establishing systems to achieve manual updates of service

request response time information from RAMM to MagiQ at the same time that

completion times are entered into MagiQ from RAMM. This may require

additional consistency checks between the two databases to ensure that

request types and priority assignments are the same in the two systems so

that response time targets are equivalent. At first glance this appears to be

a substantial piece of work and will probably exceed the recommended

six-month timeframe.

Responsibility:

Chief Information Officer and

Manager Corporate Planning and Reporting

|

|

Progress Update

|

Council’s road maintenance

contractor Higgins has identified a solution to automate service requests

data from Council’s MagiQ system into RAMM to ensure the data is

consistent across both systems. Currently this is a one-way data transfer,

and solutions to enable two-way data transfer are being investigated.

A new process whereby Higgins update MagiQ

directly using their remote access has been documented and is now in place.

Test Reports need to be run to check whether there is a need for any

improvements in data quality.

|

|

Audit

and Risk Sub-committee Meeting Agenda

|

13 August 2020

|

|

3. Service requests – Duplicate

requests for services (Low)

|

|

Target date for completion and current status

|

30/06/2020

Complete

|

|

Ernst & Young Audit

Observation

|

When

reviewing requests for service data for the water supply and wastewater

management activities we identified duplicate requests for service for the

same matter. In some instances, requests for service were closed with zero

response times if they were confirmed as duplicates. This has an impact on

median response times through reducing this measure incorrectly.

We also noted instances

where Council initiated requests for service for planned work and these were

included in the calculation of median response times. The request for service

based metrics are primarily intended to measure response times to ratepayer requests

as opposed to Council’s internal work program.

Duplicate

requests included in the system impact the reported results especially in

instances where duplicates have a response time set to zero and have been

included in the calculation of the median.

The inclusion of requests

for service from Council employees means the measures become less focused on

Council’s responsiveness to ratepayer requests.

|

|

EY Audit Recommendation

|

We recommend implementing

controls that prevent duplicate requests for service being recorded in the

system. Alternatively, a periodic review of requests within the system could

be undertaken to identify and remove duplicate requests. The same review

could ensure Council generated requests are clearly labelled as such and

excluded from the calculation of the measure.

|

|

Action Plan

|

We agree

with the observation.

Several

solution options will be investigated further in conjunction with the

response in 2.1.1:

1. Re-design

the service request system and data capture process, to ensure that duplicate

requests, internal requests, planned work, and other non-applicable requests

can be excluded from the calculation of the performance measure.

2. Continue

the current practice of cleaning the report data manually to ensure that the

measures are reported accurately, but undertake this on a more regular basis

throughout the year as recommended above.

As noted in

2.1.1, we have already begun a review and cleaning of the report data for

FY19/20. As well as correcting the response times, this task also

includes removing duplicates and non-applicable service requests from the

calculated median response times.

Responsibility:

Manager Corporate Planning and

Reporting, and Chief Information Officer

|

|

Progress Update

|

The process for managing duplicate

requests within MagiQ was updated in March 2020. Staff are now using

the system’s ability to add multiple callers to one request (rather

than raising multiple requests for the same issue). Process

documentation for dealing with multiple callers & duplicate requests has

also been developed.

A report to identify all duplicate

requests (more than one request for a single issue) is now being circulated

to the business activity areas at month end for review, so that these can be

rectified prior to month-end reporting. Records that are duplicated in

error are being deleted from the system to ensure accuracy of the median

response time determinations. A few key staff have been selected

to be given access to do this. This work is ongoing, however, all

duplicates for 2019/20 service requests have been removed.

Requests that are raised internally (between

departments) are flagged as INTERNAL within the system and the DIA report has

been amended to exclude these.

|

|

4.

Service requests – Manual reorganisation of requests for services (Low)

|

|

Target date for completion and current status

|

30/06/2020

Solution development in progress but delayed due to

COVID-19. Expect new process to be in place from August 2020.

|

|

Ernst & Young Audit

Observation

|

To

calculate outcomes for some measures, data was extracted from the system and

put through a further manual process to determine the category of the

request. This involved adjusting the category of the request per the system

and then calculating the measure to be reported based on the excel

spreadsheet with updated categorisations.

We

identified instances where information extracted from the system was

subjected to further manual categorisation and was incorrectly categorised,

affecting the reported results. For example, requests for service that did

not relate to the particular activity or urgency categorisation were included

in calculating the outcome for that measure.

We also identified

instances where subsequent to information being extracted from the system,

changes were made to the information in the system and the associated

spreadsheet wasn’t updated to reflect these changes. Because the

measures are calculated based on the data in the spreadsheet this results in

information relevant to the request for service being excluded.

Incorrect categorisation

of data could lead to measures being incorrectly calculated.

|

|

EY Audit Recommendation

|

We recommend that

processes be updated to allow for correct classification of requests for

service at the point the requests are received. If this is impractical we

would suggest that requests for service be reviewed on a periodic basis and

reclassified within the system when a reclassification is required.

|

|

Action Plan

|

The points

above appear to refer to the current system for assessing and reporting on

Stormwater and Coastal service requests.

We agree

that this system should be amenable to significant improvement.

However, following our own analysis we have further characterised the issue:

Firstly,

our understanding is that ‘instances where information extracted

from the system subjected to further manual categorisation was incorrectly

categorised affecting the reported results’ relates to two separate

matters;

i) Where instances of service requests

related to stormwater outlets were included in calculations of the Coastal

measure for ‘Urgent requests to repair sea walls or rock

revetments’ when they should only be accounted for in the Coastal

measure for ‘Stormwater beach outlets are kept clear’. This has

been fixed in the current reporting and is a straightforward fix even in the

existing ‘manual’ spreadsheet method of reporting on Coastal KPI

measures.

ii) There were three instances of stormwater

service requests (out of 89) which were classified as urgent in error. This

error rate is unlikely to be improved by adopting the suggestion that ‘processes

be updated to allow for correct classification of request for service at the

point requests are received’. Requests are received at the

call centre for the most part and staff often either a) do not have

sufficient or accurate enough information from the caller to correctly

classify the request, or b) do not have the experience to be able to do so.

This is why we rely on a subsequent, secondary, classification process by our

stormwater team, who occasionally make errors.

Secondly,

it was identified that ‘instances where subsequent to information

being extracted from the system changes were made to the information in the

system and the associated spreadsheet wasn’t updated to reflect these

change’. It isn’t clear how many instances of this were

found but to our knowledge there weren’t many and we expect they would

be largely immaterial to the measures being reported on or the response time

calculations. Many of the changes made to request types subsequent to data

being extracted from the system do not have any material bearing on the

secondary categorisation made by the stormwater team and to revisit MagiQ on

a regular basis to update these would be both time-consuming and probably not

very productive.

A full

improvement solution to MagiQ to enable it to generate more stream-lined and

efficient Coastal and Stormwater service request reporting will take

significant investigation and discussion with both MagiQ, regarding the system’s

capabilities, and the Coastal and Stormwater team, regarding their

requirements. We envisage the following:

i) introducing a pro-forma report that

doesn’t require manual set-up each week and only needs date ranges

entered to provide the appropriately filtered list of service requests each

week.

ii) ideally, we would then like to see

enhancements to the system so that there are a range of drop-down or

pick-list categories that the Coastal and Stormwater team can use for

providing secondary and tertiary categorisations to each service request (so

that this is done in MagiQ rather than on a separate spreadsheet). This

categorisation process would include categorisations as to which service

requests are Coastal or Stormwater requests, and further to that, which are

urgent/non-urgent, council/private issues, affect buildings/or don’t

etc.

iii) if such improvements are feasible then

when that secondary categorisation process is complete each week, a report

should be able to be generated from MagiQ which generates the equivalent of

the current Stormwater and Coastal service request spreadsheets.

This

approach would significantly improve the efficiency of the current process

and improve the audit trail. It would not remove the human judgement

factor behind the categorisation process as that is how the categorisations

are currently made in MagiQ in any case. We would need to investigate whether

there is an efficient process for checking whether subsequent changes to

categorisations of service requests not initially identified as relevant for

Coastal or Stormwater reporting purposes have, as a result of a

re-categorisation in MagiQ, become relevant for those purposes.

This will

be a significant piece of work and will need to be undertaken in concert with

the planned upgrade to MagiQ and other proposed improvements recommended to

improve reporting of actual resolution times and avoidance of counting

duplicate service requests in those calculations.

Responsibility:

Manager

Corporate Planning and Reporting, and Chief Information Officer

|

|

Progress Update

|

The management of Coastal & Stormwater

service requests and manual data manipulation was reviewed as part of a

previous KPI project. The BI team and Coastal & Stormwater team

reviewed the proposed changes from that project and agreed the following:

• amend

SR request “types” to align with KPI reporting requirements

• update

Kbase instructions for Customer Engagement staff

• create

new reports in MagiQ to align with KPI reporting requirements

Due to key resources being allocated to the EOC to

assist with Covid-19 response, this work has been delayed. For the

2019/20 audit the current manual categorisation and quality checking will

remain. The above changes are planned to be implemented in August 2020.

|

|

5.

Corporate policies due for review (Low)

|

|

Target date for completion and current status

|

30/12/2020

On-track but progress delayed by COVID-19

|

|

Ernst & Young Audit

Observation

|

We

observed various employee manuals and policy documents were last updated over

3 years ago. Specifically, we noted the below policies are currently overdue

for review and update:

a. Receipt

of gifts and hospitality

b. Rewards

and recognition policy

c. Mitigation

of fraud

d. Employee

code of conduct

e. Elected

member code of conduct

Policies and other guidance documents should be

updated on a regular basis to ensure any changes in circumstances that

require additional guidance are incorporated on a timely basis.

|

|

EY Audit Recommendation

|

We recommend that

corporate policies be monitored and updated on a regular basis.

|

|

Action Plan

|

We accept

the findings and recommendation from audit. The register of corporate

policies, including review dates, will be updated and monitored by Corporate

Services going forward as part of the wider policy programme.

Responsibility:

Manager

Research and Policy, Corporate Services

|

|

Progress Update

|

The Research and Policy team are currently developing

a programme of work to review, update and maintain all corporate policies.

This includes prioritising the review of the policies identified above. This

programme has been delayed by COVID-19 restrictions, however, work has now

resumed on this programme.

|

|

6.

Timeliness of purchase order initiation (Low)

|

|

Target date for completion and current status

|

30 September 2020

Delayed but on-track

|

|

Ernst & Young Audit

Observation

|

During our testing of the expenditure and payments

process we observed that some purchase orders were generated subsequent to

the receipt of invoices.

Without adequate controls for processing and

reconciling purchase orders, invoices and the receipt of goods and services,

there is an increased risk that inappropriate or erroneous expenditure is

incurred or reported. A

purchase order system works most effectively when purchase orders are

approved prior to goods or services being purchased. After the transaction

has occurred there may be less opportunity to change the agreement that has

been entered into.

|

|

EY Audit Recommendation

|

We recommend purchase

orders are raised and appropriately approved prior to placing orders with

suppliers.

|

|

Action Plan

|

Management

accepts the recommendation and is currently working on a programme for

induction and increased training for staff to ensure there is a consistent

high standard of compliance with the Procurement Policy across all areas of

the Council. The Finance team worked with the suppliers during the

2018/19 year to highlight the importance of requesting an EPO number from

Council before beginning any work.

Responsibility:

Chief Financial

Officer/ Manager, Financial Accounting

|

|

Progress Update

|

Finance is implementing an Accounts Payable

Automation function across the Council and engaged CSG technologies Limited

in February 2020 to implement a Scanning and Optic character recognition

(SOCR) solution to streamline our supplier payment process. Council is

currently testing the solution functionality and its integration with our

current Financial Management Information System (MagiQ).

The delivery of the project was delayed by the

COVID-19 restrictions and full implementation has been delayed to the end of

August 2020. As part of this project, EPO training will be rolled out to all

EPO users within Council.

Automation will strengthen the discipline of

initiating an EPO when the goods or services are ordered as the EPO number

will be a key field on the supplier invoice required by the payment solution.

Council suppliers will be informed, before the “go-live” date, of

the changes to our systems and the importance of the EPO reference on their

invoices to ensure prompt payment.

Council-wide procurement training continues.

|

|

7.

Approval of expenditure (Low)

|

|

Target date for completion and current status

|

30/06/2020

On-going

|

|

Ernst & Young Audit

Observation

|

KCDC’s

General Expenses policy states “one-up” authorisation must be

given to the person who will benefit or might be perceived to benefit from

the expenditure.”

We noted two instances where an expense

claim was either authorised by a person who was not one up from the

individual that incurred the cost or was not one up from the most senior

individual that benefited or might be perceived to have benefited from the

expenditure. In both instances we are satisfied that the expenditure was

appropriate but have recommendations regarding the execution of the relevant

controls.

This may increase the risk

that inappropriate expenditure goes undetected.

This policy also serves to safeguard

staff in that in instances where they may have been perceived to have benefited

from Council expenditure an independent member of staff has concurred with

their judgement that the costs are appropriate.

|

|

EY Audit Recommendation

|

We recommend that

expenses incurred are approved in a manner that is in line with KCDC’s

policies

|

|

Action Plan

|

Management

accepts the findings and recommendation from Audit. Corporate Services will

seek to increase Council-wide access to and awareness of all corporate

policies

Responsibility:

Chief Financial

Officer / Manager, Financial Accounting

|

|

Progress Update

|

The Accounts Payable team are manually reviewing

each expense claim submitted for payment to ensure that it has been approved

in accordance with the General Expenses policy. If not, the claim is returned

to the relevant staff members to be corrected.

The General Expense policy is included in the

programme of work being developed by the Research and Policy team to review,

update and maintain Corporate Policies, as noted in control finding No. 5

above.

|

|

8.

Review of useful life of landfill asset (Low)

|

|

Target date for completion and current status

|

30/06/2020

Completed

|

|

Ernst & Young Audit

Observation

|

The useful life of the Otaihanga landfill

asset has not been thoroughly re-assessed recently. The asset is nearing the

end of its capacity and is only able to accept clean-fill going

forwards. There is currently an asset recorded on balance sheet for the

Otaihanga landfill that has a residual useful life spanning a number of

years. If the landfill is near to the end of its useful life and the asset

has limited remaining value the residual useful life used for accounting

purposes may need to be reduced or the value attributed to the asset may need

to be decreased.

|

|

EY Audit Recommendation

|

The

current useful life of the landfill suggests that benefit will continue to be

derived from the landfill over a number of years going forward. We recommend

that Council consider the nature and timing of the expected benefits from the

landfill and use this as context for evaluating if the current useful life is

still appropriate and if Council is likely to receive future benefit from the

landfill that broadly equates to the current carrying value of the landfill

asset.

|

|

Action Plan

|

Management

accepts the findings and will assess the economic life of the asset during

the 2019/20 year.

Responsibility:

Chief Financial

Officer /Manager, Financial Accounting

|

|

Progress Update

|

Council

reviewed the current useful life and future benefit/service potential of the

Otaihanga landfill asset during June 2020.

The

capping of the landfill has progressed faster than initially anticipated.

Therefore, the final closure date of the landfill has been brought forward

from the resource consent closure date of June 2026 to June 2022.

While the

landfill will be in-use for another 2 years, it has been determined that the

future income generated from accepting clean-fill is negligible.

In accordance

with IPSAS (International Public Sector Accounting Standards) an asset should

be held at its recoverable service amount. As negligible service value

will be delivered by the asset, the full value of this asset at year-end

($2,998,259) has been impaired to the statement of comprehensive revenue and

expense.

|

8.3 Quarterly

Treasury Compliance Report

Author: Anelise

Horn, Manager Financial Accounting

Authoriser: Mark

de Haast, Group Manager Corporate Services

Purpose of Report

1 This

report provides confirmation to the Audit and Risk Subcommittee of the

Council’s compliance with its Treasury Management Policy (Policy) for the

six months ended 30 June 2020.

Delegation

2 The

Audit and Risk Subcommittee has delegated authority to consider this report

under the following delegation in the Governance Structure, Section C.1.

Ensuring that

the Council has in place a current and comprehensive risk management framework

and making recommendations to the Council on risk mitigation.

Background

3 The

Policy sets out a framework for the Council to manage its borrowing and

investment activities in accordance with the Council’s objectives and

incorporates legislative requirements.

4 The

Policy mandates regular treasury reporting to management and the Strategy and

Operations Committee, as well as quarterly compliance reporting to the Audit

and Risk Subcommittee.

5 In

order to assess the effectiveness of the Council’s treasury management

activities and compliance to the Policy, certain performance measures and

parameters have been prescribed. These are:

· cash/debt

position;

· liquidity/funding

control limits;

· interest

rate risk control limits;

· counterparty

credit risk;

· specific

borrowing limits; and

· risk

management performance.

6 Due

to the cancellation of the Audit and Risk Subcommittee meeting on 24 May 2020

due to COVID-19, this report covers the compliance reporting for both the third

quarter (January to March) and the fourth quarter (April to June) of the

2019/2020 financial year.

discussion

Cash/Debt Position

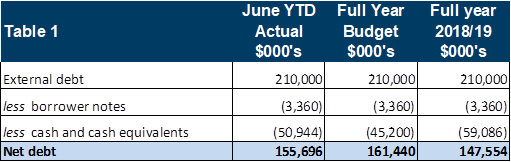

7 Table

1 below shows the Council’s net debt position as at 30 June 2020 against

the 2019/20 full year budget and the prior year closing balance.

8 During

the past six months, the Council has issued $20 million of new debt.

9 $15

million was issued to pre-fund the May 2021 and October 2021 debt

maturities. As part of the Council’s prefunding programme, all

prefunding is placed on term deposit, at the most favourable market rates

available at that time.

10 $5

million was issued to part fund the 2019/20 planned capex work programme.

11 During

the same period, $25 million of long term debt matured during April 2020. This

was fully funded through the Council’s prefunding programme and was

repaid from term deposits maturing on the day.

12 The

table below shows (a) the movement in the Council’s external debt balance

and (b) the movement in the Council’s pre-funding programme by debt

maturity, for the year ended 30 June 2020.

13 As

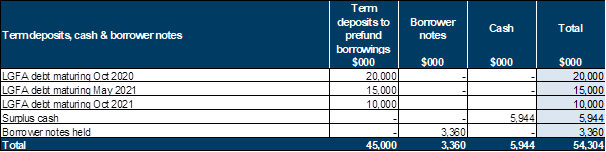

at 30 June 2020, the Council had $54.3 million of cash, borrower notes and term

deposits on hand, relating mainly to the Council’s debt pre-funding

programme. This is broken down as follows:

14 For

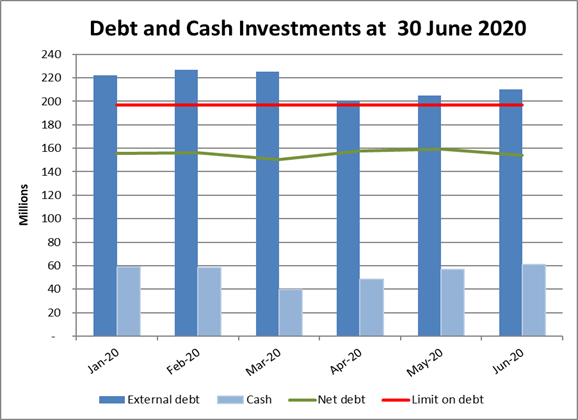

the six months ended 30 June 2020, the Council has not breached its net debt

upper limit, as shown in the chart below:

15 The

Council is however targeting ,through its financial strategy, to keep net

borrowings below 200% of total operating income. At 30 June 2020, the

Council’s net borrowings are 184.8% of total operating income.

Liquidity/Funding control limits

16 Liquidity

and funding management focuses on reducing the concentration of risk at any

point so that the overall borrowings cost is not increased unnecessarily and/or

the desired maturity profile is not compromised due to market conditions. This

risk is managed by spreading and smoothing debt maturities and establishing

maturity compliance buckets.

17 Since

October 2015 the Council’s treasury strategy has included a debt

pre-funding programme. The Policy allows pre-funding of the Council debt

maturities up to 18 months in advance, including re-financing. Market

conditions have been favourable for this approach, where the Council draws down

debt early and is able to invest the funds on term deposit for a positive net

return.

18 The

strength of the Council’s debt pre-funding programme was again

highlighted by the Council’s independent Credit Rating Agency, Standard

& Poor’s (S&P), during their July 2020 review. This has resulted

in the Council’s credit rating remaining at AA with a stable outlook for

the following year. S&P noted that the Council’s liquidity coverage

remains exceptional.

19 The

following chart presents the Council’s debt maturity dates in relation to

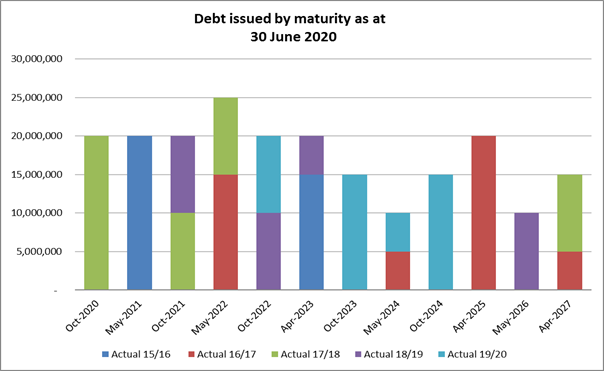

the financial year in which the debt was issued. This demonstrates that since

2016/17, the Council has actively reduced risk concentration by spreading debt

maturity dates and debt maturity values.

20 Debt

maturities must fall within maturity compliance buckets. These maturity buckets

are as follows:

|

Maturity Period

|

Minimum

|

Maximum

|

|

0 to 3 years

|

10%

|

70%

|

|

3 to 5 years

|

10%

|

60%

|

|

5 to 10 years

|

10%

|

50%

|

|

10 years plus

|

0%

|

20%

|

21

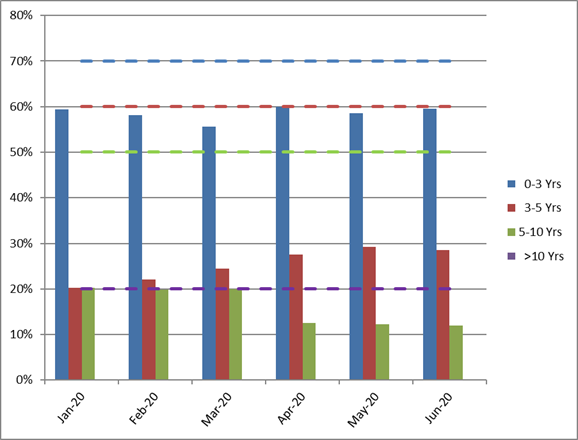

For the six months ended 30 June 2020, the Council has been fully compliant

with its debt maturity limits, as shown by the chart below. The upper limits,

as shown by dashed lines, relate to the bars of the same colour. For example,

the 0 to 3 year upper limit of 70% is in blue. Actual maturities in the 03 year

bucket are represented by the blue bars. The Council has no long term debt

maturing in ten years’ time or beyond.

Interest rate risk control limits

22 The

Council issues all debt on a floating rate basis, as lower interest rates are

realised this way, and uses fixed interest rate swaps (hedges) to minimise

exposure at any one time to interest rate fluctuations. This ensures more

certainty of interest rate costs when setting our Annual Plan and Long Term

Plan budgets.

23 Without

such hedging, the Council would have difficulty absorbing adverse interest rate

movements. A 1% increase in interest rates on $210 million of external debt

would equate to additional interest expense of $2.1 million per annum.

Conversely, fixing interest rates does however reduce the Council’s

ability to benefit from falling and/or more favourable interest rate movements.

24 The

objectives of any treasury strategy are therefore to smooth out the effects of

interest rate movements, while being aware of the direction of the market, and

to be able to respond accordingly.

25 The

Policy sets out the following interest rate limits:

Major control limit where

the total notional amount of all interest rate risk management instruments

(i.e. interest rate swaps) must not exceed the Council’s total actual

debt, and;

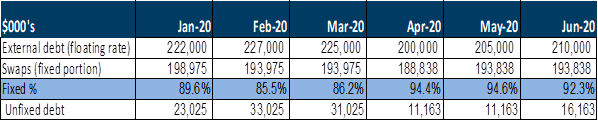

Fixed/Floating Risk Control

limit, that specifies that at least 55% of the Council’s borrowings

must be fixed, up to a maximum of 100%.

26 The

Council has been fully compliant for the six months ended 30 June 2020, as

shown by the table below.

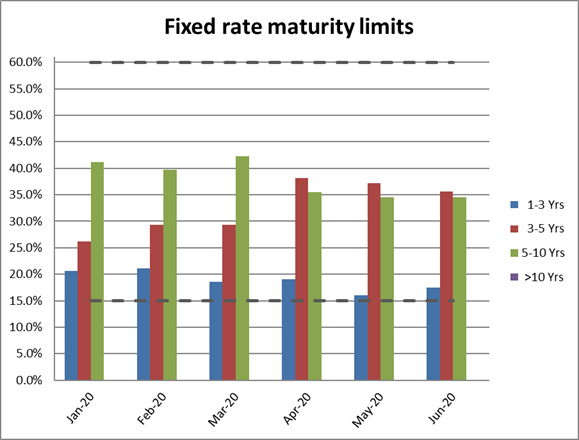

27 Similar to debt maturities, hedging

instrument maturities must also fall within maturity compliance buckets.

These maturity compliance buckets are as follows:

|

Period

|

Minimum

|

Maximum

|

|

1 to 3 years

|

15%

|

60%

|

|

3 to 5 years

|

15%

|

60%

|

|

5 to 10 years

|

15%

|

60%

|

|

10 years plus

|

0%

|

20%

|

28 The

Council has been fully compliant for the six months ended 30 June 2020, as

shown by the following chart. Note that maturities falling within 1 year are

not included.

Counterparty Credit Risk

29 The

policy sets maximum limits on transactions with counterparties. The purpose of

this is to ensure the Council does not concentrate its investments or risk

management instruments with a single party.

30 The

policy sets the gross counterparty limits as follows:

|

Counterparty/Issuer

|

Minimum Standard and

Poor’s long term

|

Investments maximum per

counterparty

|

Risk management

instruments maximum per counterparty

|

Borrowing maximum per

counterparty

|

|

NZ Government

|

N/A

|

Unlimited

|

None

|

Unlimited

|

|

LGFA

|

AA-/A-1

|

$20m

|

None

|

Unlimited

|

|

NZ Registered Bank

|

A+/A-1

|

60% of total investments or

$25m; whichever is greater

|

50% of total instruments or

$80m; whichever is greater

|

$50m

|

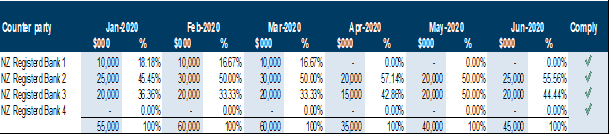

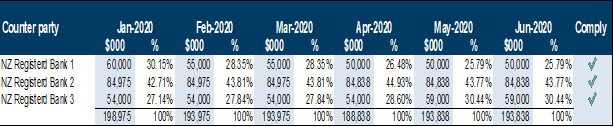

31 The

Council was in full compliance with all counterparty credit limits for the six

months ended 30 June 2020. The tables below show the Council’s

investments and risk management instruments holdings per counterparty for this

period.

Term deposits

*Policy Limit: 60% of total investments or $25 million;

whichever is greater

Interest rate

swaps

*Policy

Limit: 50% of total instruments or $80 million; whichever is greater

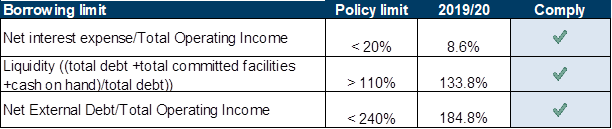

Specific Borrowing Limits

32 In

managing debt, the Council is required to adhere to the limits below. The

Council fully complied with these limits for the 6 months ended 30 June 2020

(or a period as otherwise specified) and the results are shown below:

Risk Management Performance

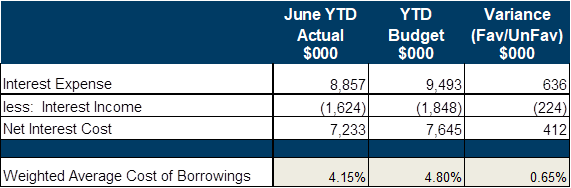

33 The

following table shows the Council’s interest income and expense for the

year ended 30 June 2020, together with the weighted average cost of

borrowing (WACB)

34 The

Council’s net interest cost for the year is $412,000 favourable to

budget. This is mainly due to less external borrowings at the start of the

2019/20 financial year than planned and delays to the Council’s capital

works programme due to Covid-19 restrictions.

35 The

Council has been effective in its treasury management with its weighted average

cost of funds being 0.65% lower than planned as at the 30 June 2020.

36 The

following graph shows the cost of borrowing each month.

Considerations

Policy considerations

37 There

are no policy considerations in addition to those already noted in this

report.

Legal

considerations

38 There

are no legal considerations arising from this report.

Financial

considerations

39 There

are no financial considerations in addition to those already noted in this

report.

Tāngata

whenua considerations

40 There

are no tāngata whenua considerations arising directly from this

report.

Significance and Engagement

Significance

policy

41 This

matter has a low level of significance under the Council’s Significance

and Engagement Policy.

Publicity

42 There

are no publicity considerations arising from this report.

|

Recommendations

43 That

the Audit and Risk Subcommittee notes the Council’s full compliance

with its Treasury Management Policy for the six months ended 30 June 2020.

|

Appendices

Nil

8.4 Risk

Management - Business Assurance Update

Author: Sharon

Foss, Business Improvement Manager

Authoriser: Mark

de Haast, Group Manager Corporate Services

Purpose of Report

1 This

report primarily updates the Audit and Risk Subcommittee on the on-going

implementation of the Enterprise Risk Management (ERM) framework.

Delegation

2 The

Audit and Risk Subcommittee has delegated authority to consider this report

under the following delegation in the Governance Structure, Section C.1.

Ensuring that Council has in

place a current and comprehensive risk management framework and making

recommendations to the Council on risk mitigation.

Background

3 The

key elements of the Enterprise Risk Management Framework include:

· Risk

Management;

· Business

Continuity Management;

· Business

Assurance; and

· Procurement

Improvement Programme.

4 The

key work streams within this area are:

· Regularly

discuss risks with the Council’s business groups and Senior Leadership

Team and embed the day-to-day management of risks in the more routine activities;

· develop

a risk communication/reporting process at, and between, the following levels:

− Council/Committees;

− Senior

Leadership Team (SLT);

− Business

Units/Groups; and

− Projects,

Asset Management.

· develop

a Business Continuity Management System for effective response to a range of

potential business disruptions;

· provide

fraud awareness training;

· provide

business assurance oversight and complete business assurance work; and

· improve

the understanding and tools to support good procurement practices.

5 As

previously reported, the intended outcomes from performing this programme well

will include:

· stakeholders,

external auditors, Council and management achieve high levels of assurance that

the real risks are being identified and managed effectively;

· better

decision making throughout the business through greater awareness of the real

risks (threats and opportunities); and

· clarification

and socialisation of the Council’s risk appetite and tolerance.

Enterprise Risk Management Progress Update

6 Guidance

for the risk management, procurement and assurance work has been established

through a collaborative process with Council staff.

7 The

work has focussed primarily on tangible outputs, as discussed separately below.

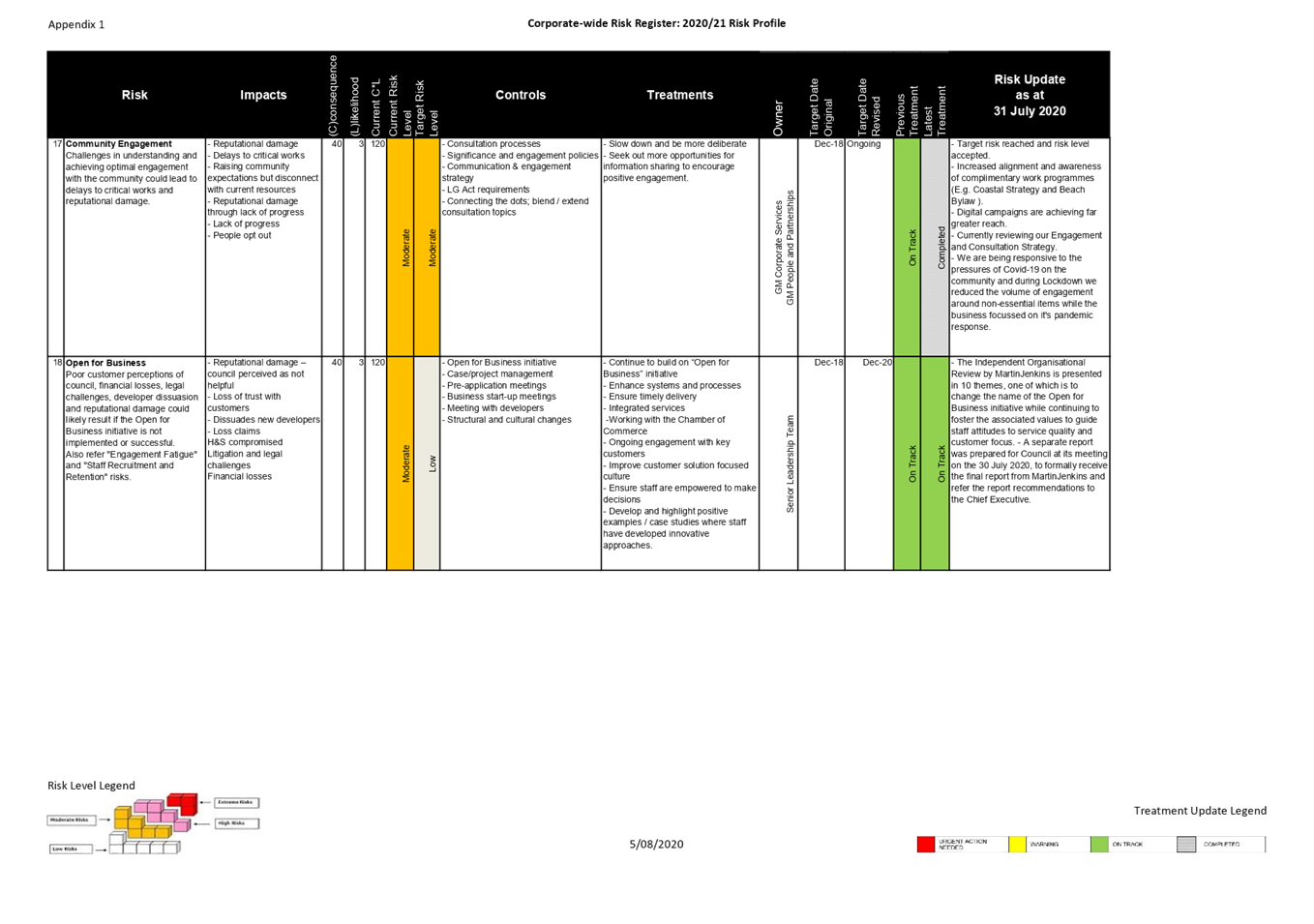

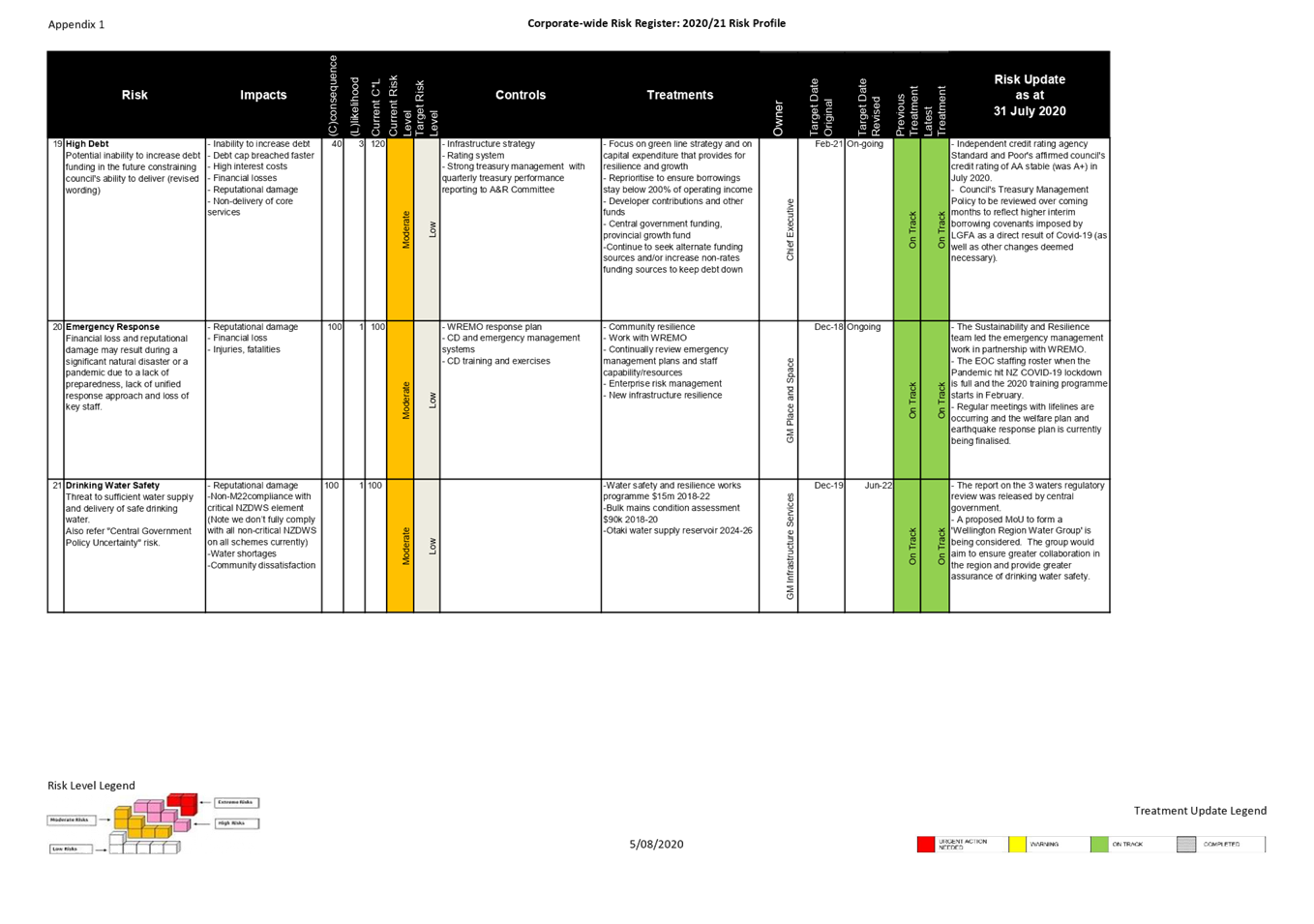

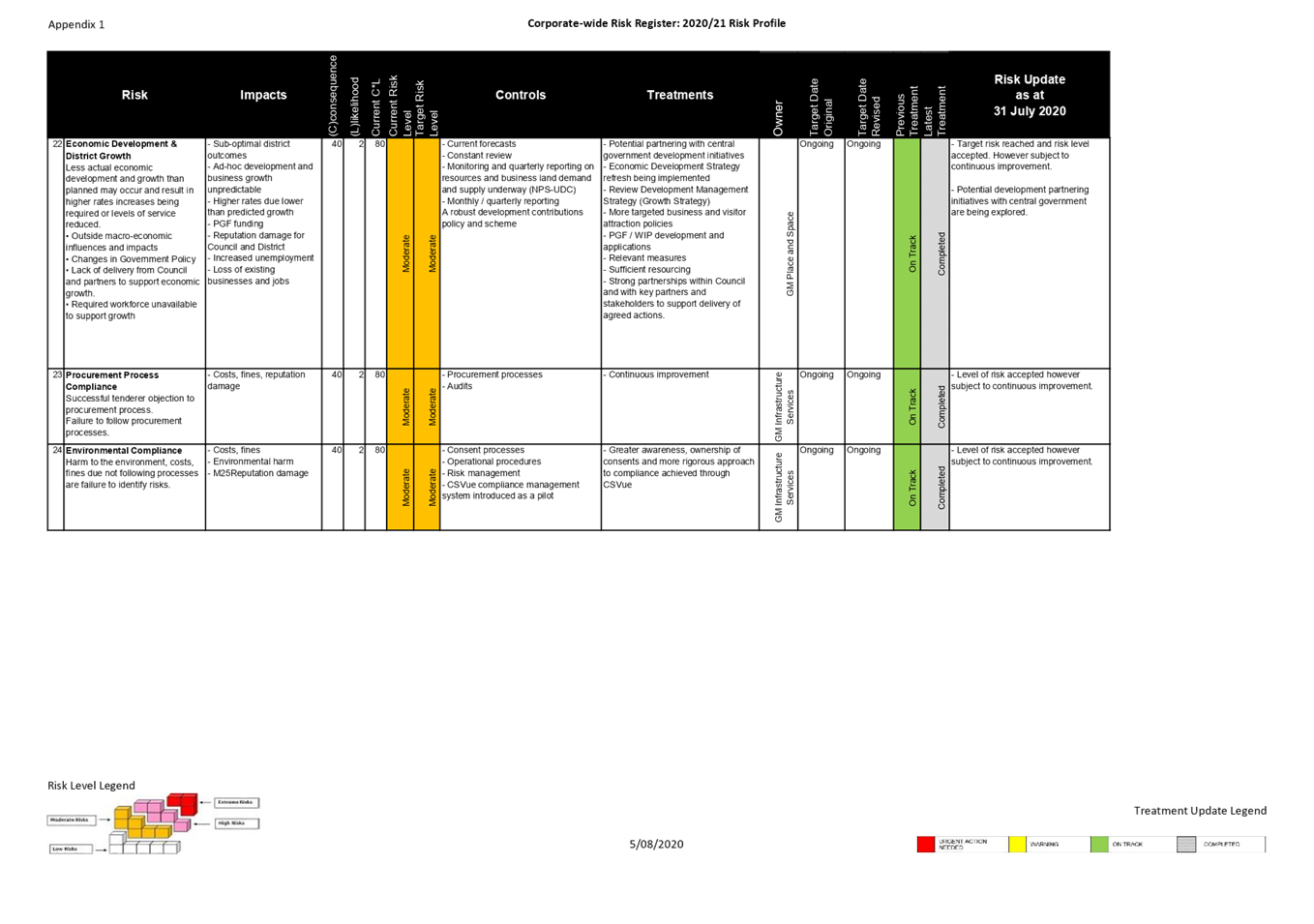

Corporate Risk Profile

– Status Update

8 As

part of Enterprise Risk Management (ERM) a risk profile, comprising a risk

register and risk treatment plan, was established. This is subject to

approximately quarterly updates by management and is then reported to the

Subcommittee. The focus is on identifying, managing and communicating the very

highest strategic and operational risks that the Council faces.

9 Engagement

on the risk profile now routinely includes conversation with activity managers

as well as Group Managers. The overall risk management culture and practice is

improving and risk conversations are widening.

10 The

concept of risk acceptance is being further embedded across the organisation,

i.e. certain moderate level risks may be overtly tolerated by the business in

the context of the costs or impracticalities to further mitigate the risk.

11 The

risk profile has been reviewed and updated by the Group Managers and the

relevant Activity Managers. The Corporate Risk Register is attached as Appendix

1 to this report.

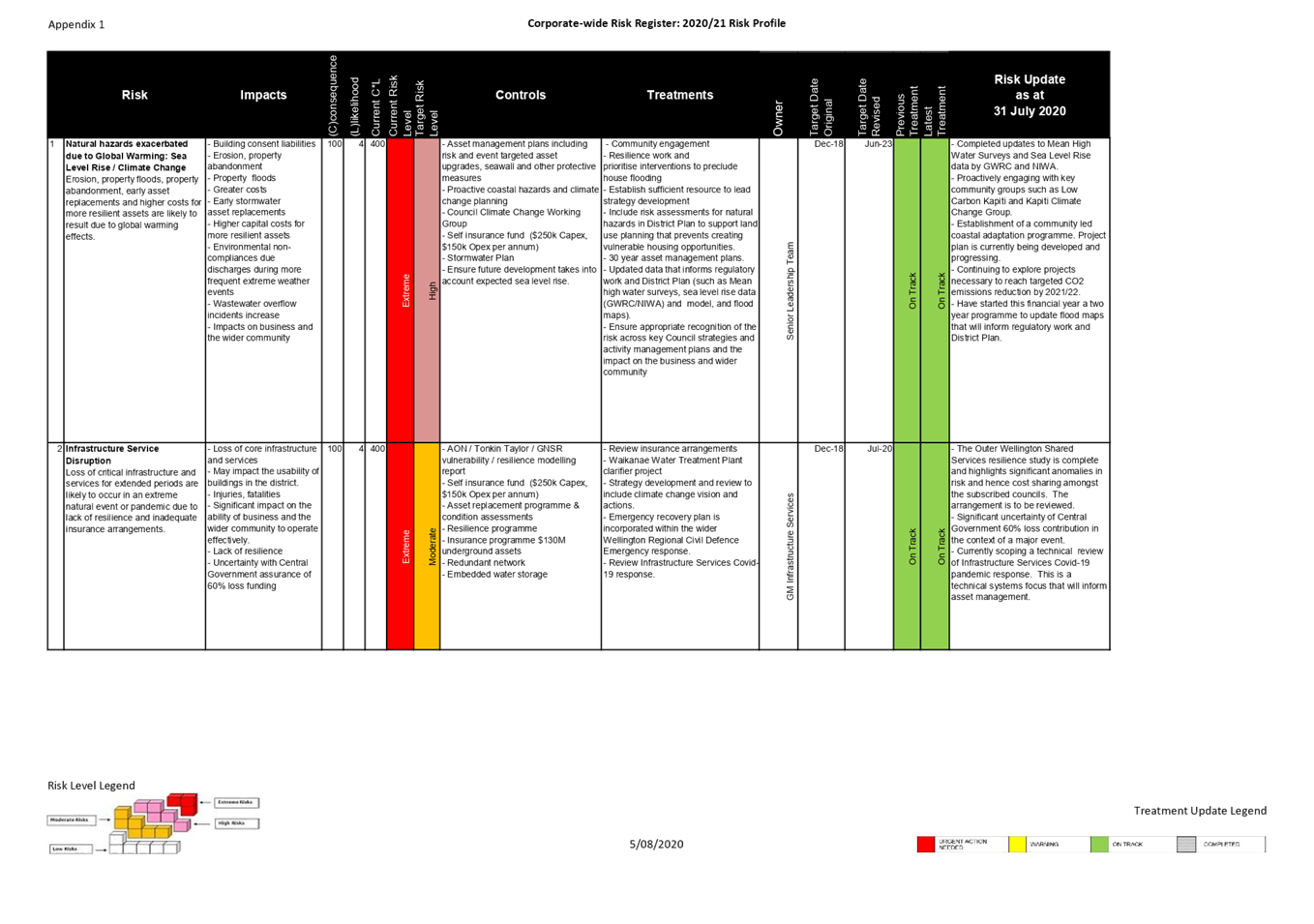

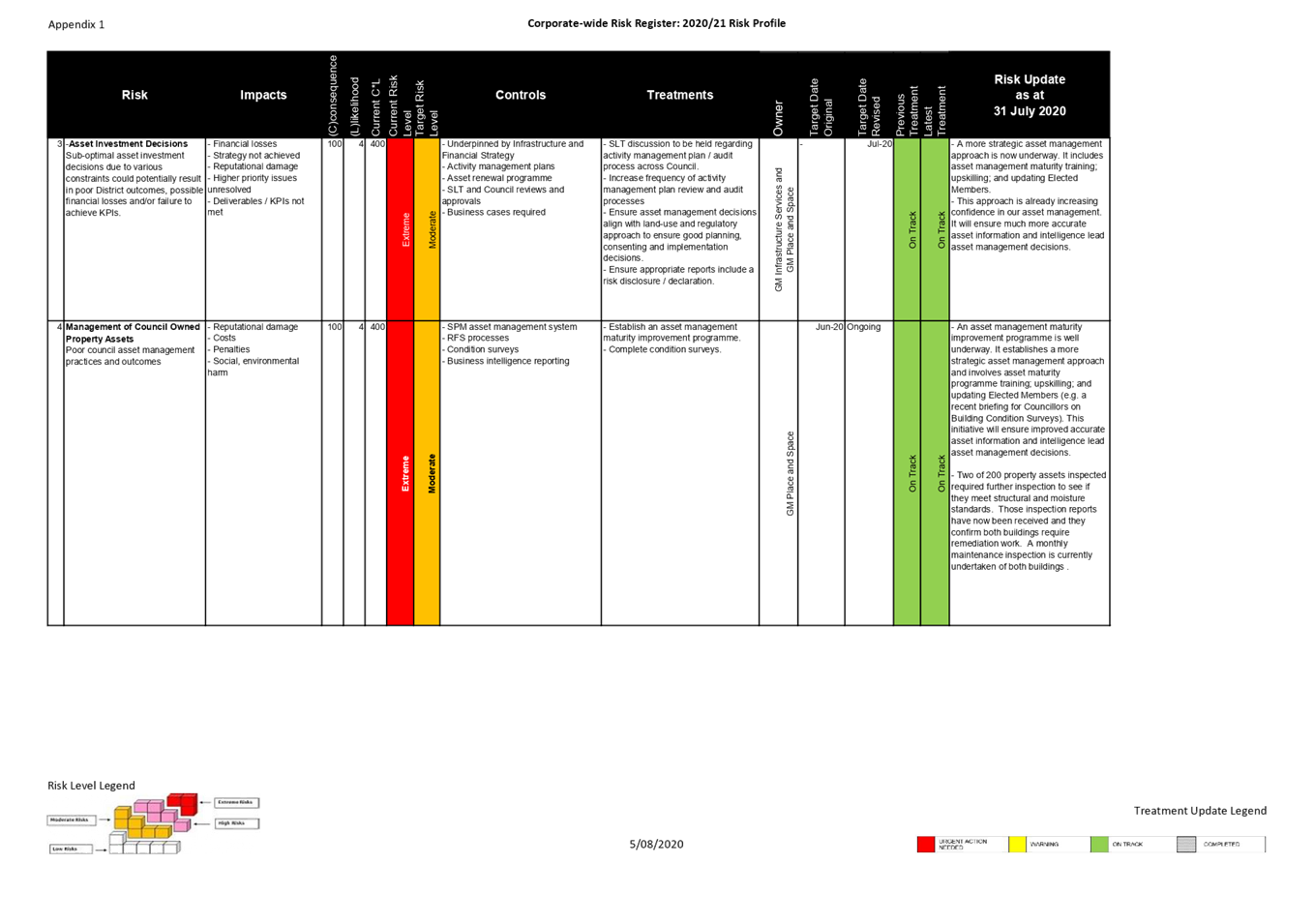

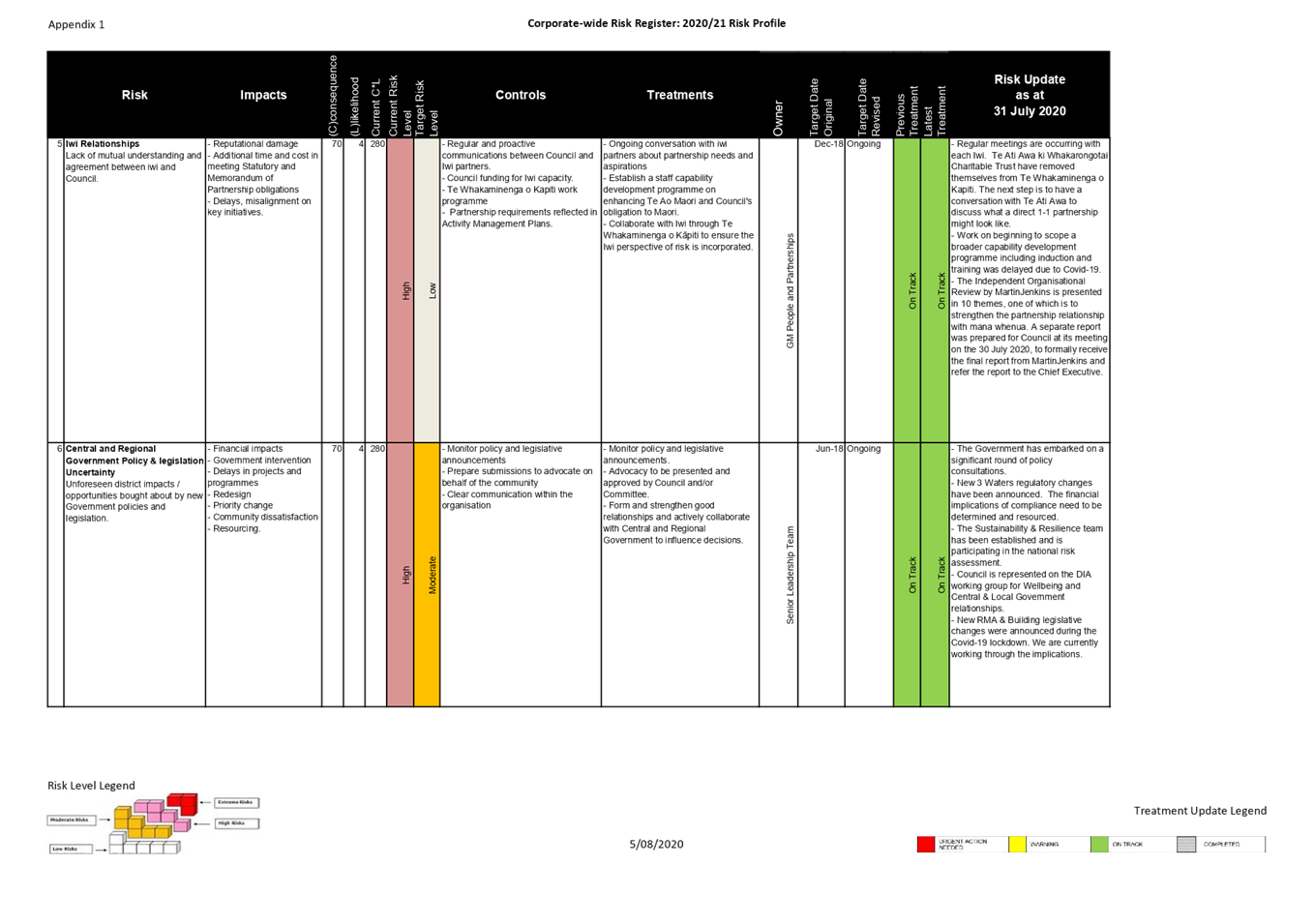

12 The

intention is for the Subcommittee to first familiarise themselves with the

Corporate Risk Register and thereafter, to nominate any risk/s for “deep

dive” discussions at future Subcommittee meetings. Risk “deep

dives” provide an opportunity for Subcommittee members to engage and gain

a deeper insight on a specific risk/s.

13 Whilst

there is no specific “deep dive” included in this report, it is

appropriate to provide the Subcommittee with an overview of the Council’s

response to date to the challenges brought about by Covid-19.

14 On

11 March 2020, the World Health Organization declared the outbreak of a

coronavirus (Covid-19) pandemic and two weeks later, the New Zealand Government

declared a State of National Emergency. From this, the country went into Alert

Level 4 lockdown. As a result, the Council implemented its pandemic plan

and responded in line with government Alert Level guidelines.

15 The

Council moved quickly to open the Emergency Operations Centre and comply with

the Health Order. Services deemed essential continued and non-essential

services ceased and/or were delivered in accordance with the Health Order and

the appropriate Alert Level. Examples of some key changes to service

delivery made at Alert Levels 4 and 3 are shown in the table below:

|

Example

of changes made to Service Levels

|

Alert Level 4 - 25 March 2020

|

Alert Level 3 - 27 April 2020

|

|

Council

Offices

|

Closed.

Staff working remotely

|

Closed.

Staff working remotely

|

|

Transfer /

recycling stations and kerbside recycling

|

Closed. No

kerbside collection.

|

Open for

rubbish drop off only.

Kerbside

recycling collection resumed.

|

|

Sewer/water/stormwater

maintenance

|

Emergency

repairs and maintenance as required.

|

Emergency

repairs and maintenance as required.

|

|

Reserves,

playgrounds and sportsgrounds

|

Closed. No

mowing or planned maintenance undertaken.

|

Closed.

High priority mowing and maintenance undertaken.

|

|

Roads and

coastal infrastructure

|

Emergency repairs and maintenance

as required.

|

Emergency repairs and maintenance as required. Planning and higher

priority work undertaken.

|

|

Resource

and building consents

|

Processing

continued but no building inspections undertaken.

|

Processing continued. Building and subdivision site inspections

undertaken. Virtual hearings for resource consents.

|

|

Noise

control

|

Very limited

service.

|

Excessive noise complaints investigated.

|

|

Libraries

|

Closed.

Virtual services available.

|

Closed. Virtual services available.

|

|

Pools,

Halls, Public Toilets

|

Closed.

|

Closed.

|

16 A

considerable amount of effort went into establishing working from home

arrangements for staff where possible. This included using technology for

remote communication and meetings. Covid-19 necessitated $115,000 of critical

IT expenditure planned for 2020/21 to be brought forward to March 2020 in order

to fully support staff during the lockdown. Travel was reduced to an absolute

minimum.

17 Services

for ratepayers and businesses were provided remotely, therefore the impact on

customers was largely limited to changing meetings from in-person to virtual

meetings, and from walk-ins to phone calls or emails. A point to note is that

our customers were also subject to lockdown rules.

18 The

Council offices and facilities including service centres, libraries, aquatic

facilities, community centre, halls and venues started reopening at Alert Level

2 on 13 May 2020 with contact tracing and appropriate Covid-19 safety measures

in place. Up to 50% of our office-based staff continued to work remotely

from home to enable us to maintain physical distancing requirements.

19 For

Alert Level 1, staff began the transition back into the office from 9 June

2020.

Corporate Business Continuity Management System (BCMS) – Status

Update

20 Business

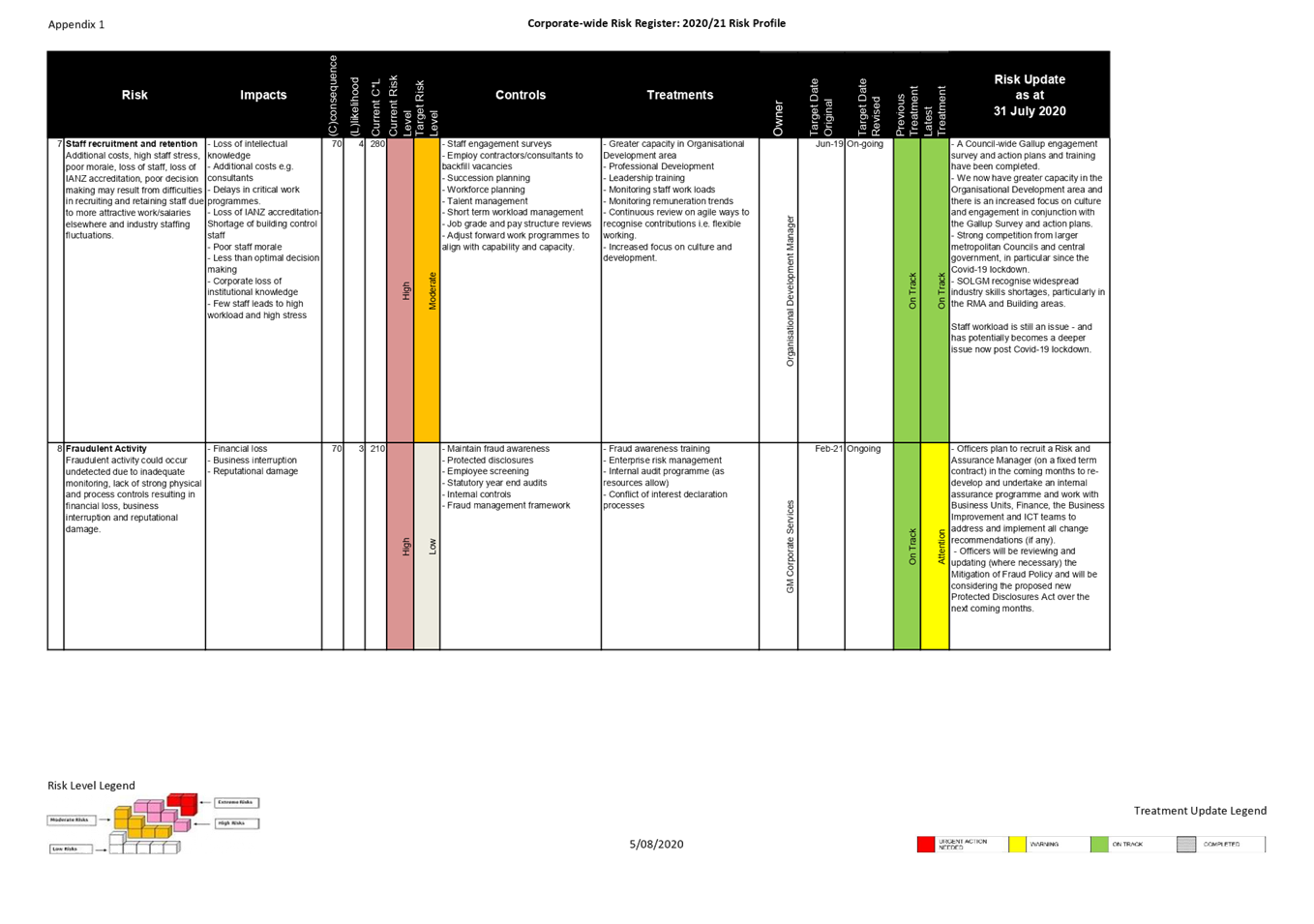

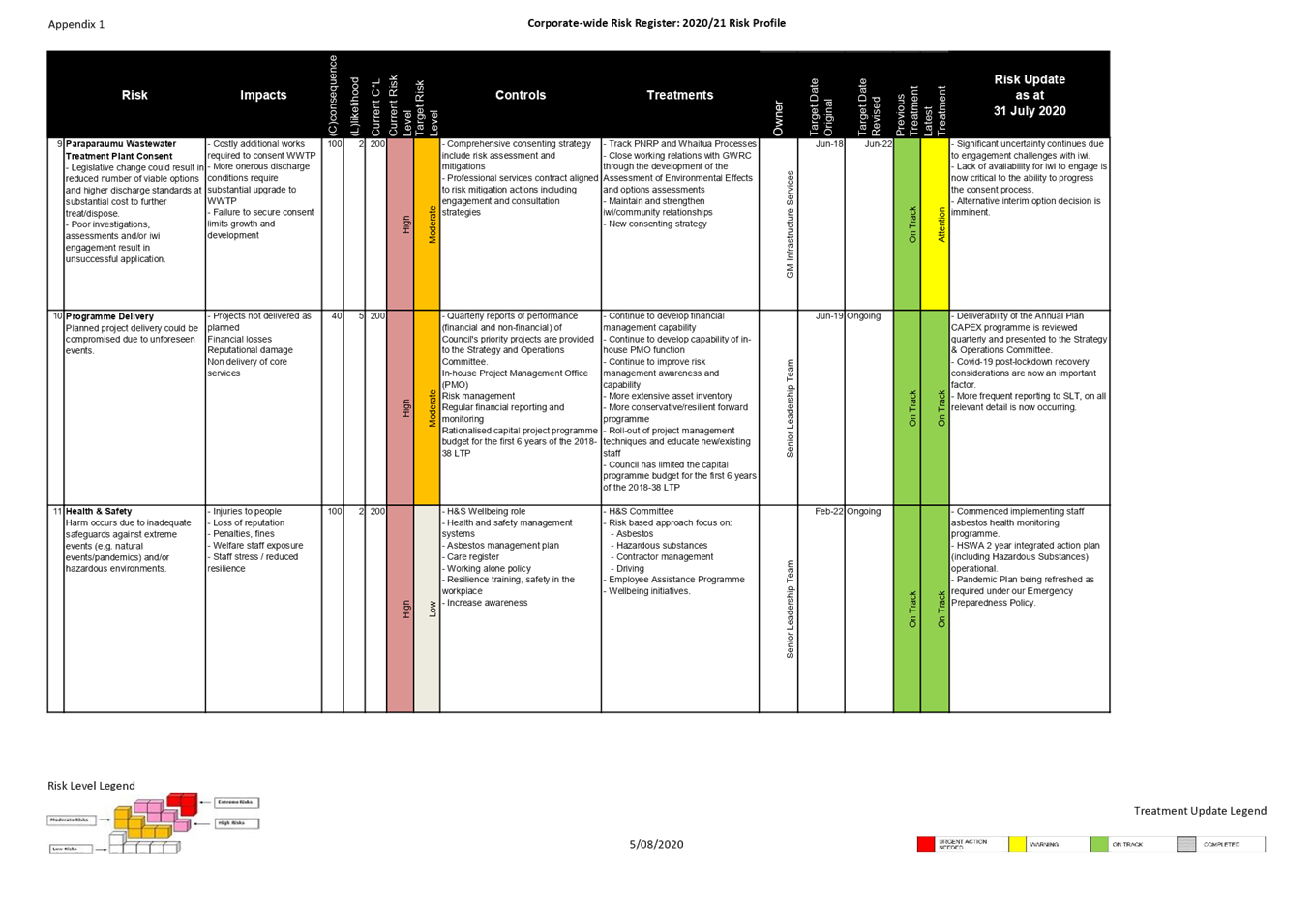

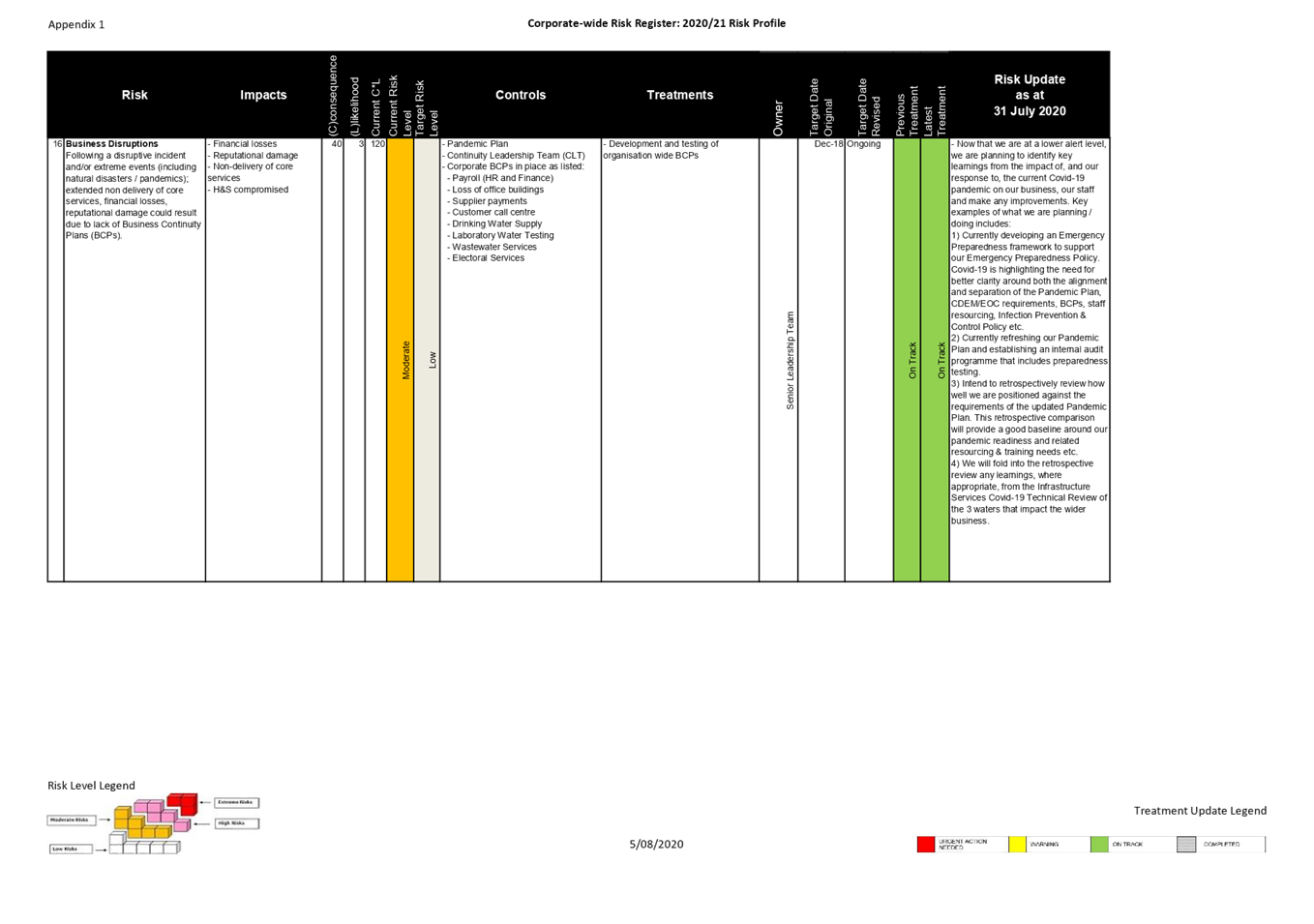

Disruptions are currently assessed as a “moderate” level risk (with

a target risk level of “Low”), on the Corporate Risk Register,

attached as Appendix 1 to this report.

21 To

address this risk, the Council is actively progressing its BCMS development

programme. The objective of the programme is to ensure that following a disruptive

incident, the Council has the systems and capability to continue the delivery

of its critical activities and services within acceptable, predefined levels

and timeframes.

22 We

intend to review all aspects of the Council’s Covid-19 lockdown experience.

The aim is to identify the key learnings from the impacts of, and the

Council’s response to the Covid-19 pandemic on our business, our staff

and our customers and stakeholders and make all necessary improvements where

needed. Some examples of what we are already planning / doing are listed below:

i. We

are currently developing an Emergency Preparedness framework to support our

Emergency Preparedness Policy. Covid-19 is highlighting the need for better

clarity around both the alignment and separation of the Pandemic Plan, CDEM/EOC

requirements, BCPs, staff resourcing, Infection Prevention and Control Policy

etc.

ii. We

are currently refreshing our Pandemic Plan and we will retrospectively review

how well we are positioned against the requirements of the updated Pandemic

Plan. This retrospective comparison will provide a good baseline around our

pandemic readiness and related resourcing and training needs etc.

iii. An

independent technical review of Infrastructure Service’s preparedness,

readiness and security of supply of essential infrastructure services, (water,

wastewater and stormwater), following localised natural disasters and pandemic

events, is currently underway to identify any service delivery risks that need

to be further mitigated.

Procurement Improvement

Programme – Status Update

23 A

procurement improvement programme commenced in 2017. Significant improvements

have been made to date. The Council established its own procurement framework

in 2018, modelled on the latest public sector procurement materials, customised

for the local government environment. This framework comprises a procurement

policy containing key principles and rules, a procurement manual setting out

procurement procedures, along with a set of templates, forms and guides to

support good procurement practice.

24 However,

further progress on the framework has been constrained by limited staff

capacity and resources and variable quality of data and information. As

previously reported to the Council, progress on the framework was particularly

delayed when the Procurement Specialist was reassigned in the previous

triennium to advise and lead the procurement process required by the

Independent Organisational Review.

25 However,

progress toward better procurement maturity has recommenced now and further

work is planned to meet the improvement targets, addressing the barriers to

progress, and adjusting the sequencing of work.

Business Assurance – Status Update

26 The

Council has contracted PricewaterhouseCoopers (PwC) to complete a PAYE tax

compliance review. Originally this was planned in March 2020 but has been

delayed due to Covid-19 restrictions. Officers are working with PwC to finalise

a new review date and a report back will be provided to the Subcommittee once

the review has been completed.

27 In

addition, Officers are planning to recruit a dedicated Risk and Assurance

Manager on a two year fixed term contract to develop and implement a risk

assurance and monitoring programme. This position will work with the Business Units,

as well as Finance, Legal, Business Improvement and IT, to identify any

internal control risks and implement all steps necessary to satisfactorily

mitigate those risks. Report backs will be provided to the Subcommittee when

internal assurance reviews have been completed.

Considerations

Policy

considerations

28 There

are no further policy implications arising from this report.

Legal

considerations

29 There

are no further legal considerations arising from this report.

Financial

considerations

30 The

work described above is planned to be funded from the 2020/21 Annual Plan

budget by way of prioritised spending.

Tāngata

whenua considerations

31 There

has been no direct engagement with tāngata whenua regarding this report.

Strategic

considerations

32 This

enterprise risk management framework contributes to ensuring that the Council

is continuing to improve its financial position against financial constraints.

Significance and Engagement

33 This

matter has a low level of significance under the Council Policy.

|

Recommendations

34 That

the Audit and Risk Subcommittee receives and notes this report, including

Appendix 1 to this report.

|

Appendices

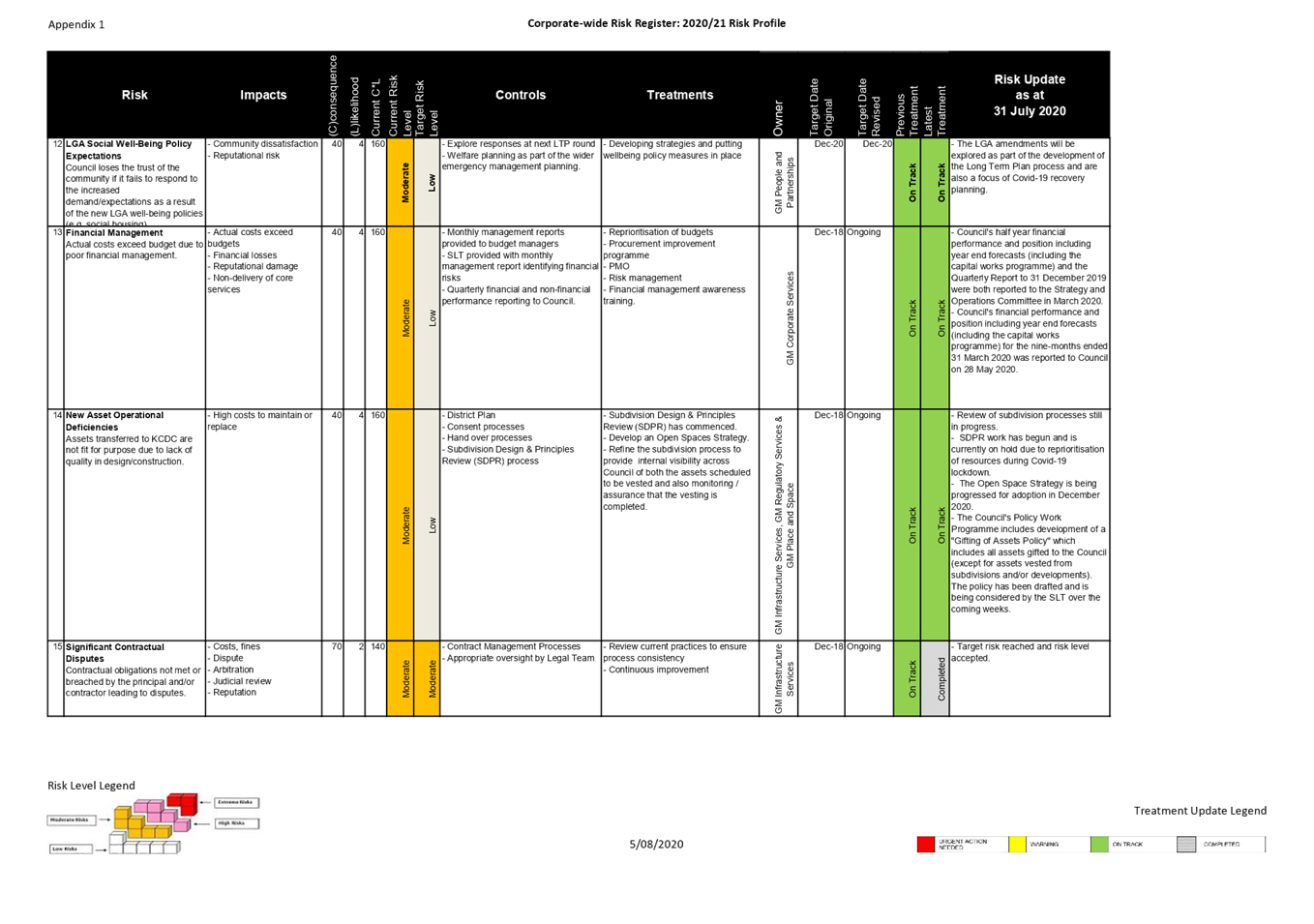

1. Corporate-wide

Risk Register 2020/21 ⇩

|

Audit

and Risk Sub-committee Meeting Agenda

|

13 August 2020

|

8.5 Waka

Kotahi NZ Transport Agency Procedural Investment Audit Report

Author: Glen

O'Connor, Access and Transport Manager

Authoriser: Sean

Mallon, Group Manager Infrastructure Services

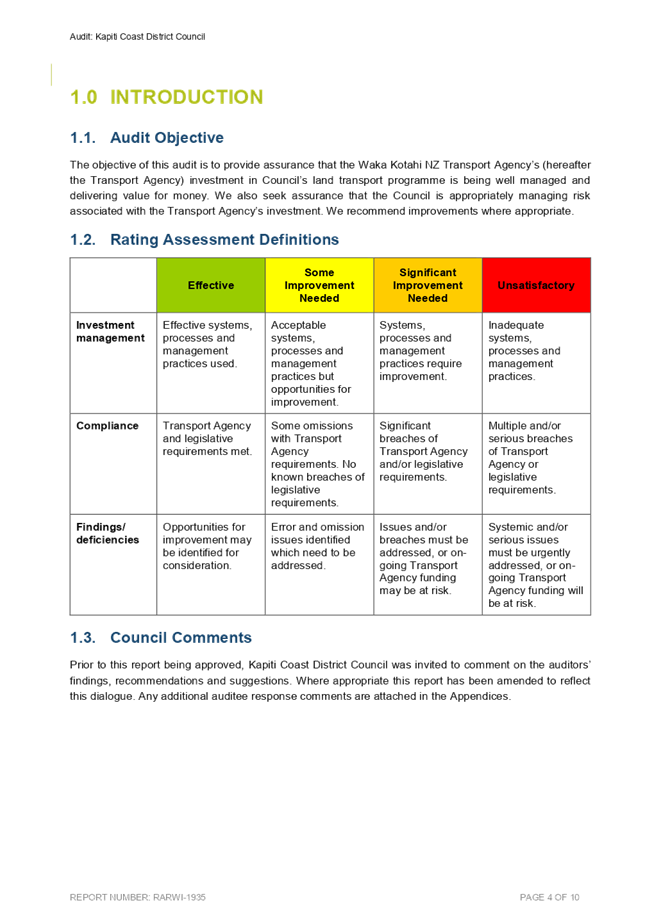

PURPOSE OF REPORT

1. To

present the findings of the Waka Kotahi NZ Transport Agency (Waka Kotahi)

Procedural Investment Audit undertaken in February 2020.

DELEGATION

2. Section

C.1 of the Governance Structure and Delegations 2019-22 Triennium provides that

the Audit and Risk Committee will monitor Council’s financial management

and report mechanisms and framework and review the audit and risk function,

ensuring the existence of sound internal systems.

BACKGROUND

3. Waka

Kotahi undertake investment audits every three to six years on Local

Authorities. The audits provide assurance that Waka Kotahi’s investment

in land transport programmes (roading) is being well managed and is delivering

value for money. Further, Waka Kotahi seek assurance that Council are

appropriately managing risk associated with the Transport Agency’s investment.

4. Waka

Kotahi carry out two types of audit for Local Authorities which are:

a. Investment audits; and

b. investment procedural audits.

5. The

investment audit monitors investment performance and is technical in

nature focusing on physical works such as road resealing, network condition and

minor works programmes. Council was audited in 2019 and was rated as

effective, which is the highest rating. This was reported to the Operations

and Finance Committee on 15 August 2019.

6. The

investment procedural audit examines the financial administration and

processes associated with the funding claimed from Waka Kotahi The audit

focuses on reviewing documents/ledgers, ledger transactions, procedures for

claiming Waka Kotahi funds and the procurement and management of roading

related works and services contracts. Waka Kotahi previously carried out a

procedural audit in 2017.

7. The

items covered in the February 2020 Investment Procedural Audit included:

· Previous

Audit Issues – review of recommendations from the previous procedural

audit.

· Financial

Processes – review of financial management/controls and alignment of

funds claimed with the Transport Agency’s activity classes.

· Procurement

Procedures – examination of procured services/physical works and compliance

with Council and Waka Kotahi procurement procedures and requirements.

· Contract

Management – review of contracts with regard to contract administration,

management and control procedures and processes.

· Professional

Services – review of council’s approach to providing and funding

professional services in accordance with Waka Kotahi requirements.

8. Waka

Kotahi’s investment into our district is typically 51% of our

approximately $6-8m per year (depending on the amount of works undertaken) land

transport programme.

9. The

investment procedural audit was undertaken at Council offices over four days

and involved Waka Kotahi ‘s auditors and Councils roading and finance

staff.

ISSUES AND OPTIONS

Issues

10. The

key findings of the audit are as follows:

· Previous

Audit Issues

There were no issues outstanding

from the previous audit.

|

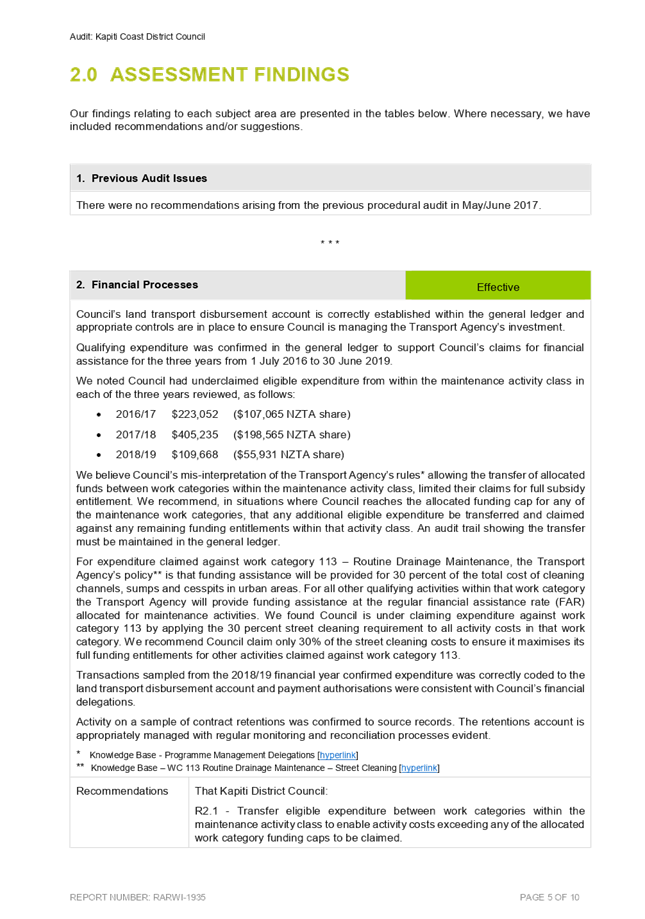

· Financial

Processes

Council’s

land transport disbursement account is correctly established within the

general ledger and appropriate controls are in place to ensure Council is

managing the Transport Agency’s investment. Qualifying

expenditure was confirmed in the general ledger to support Council’s

claims for financial assistance for the three years from 1 July 2016 to 30

June 2019.

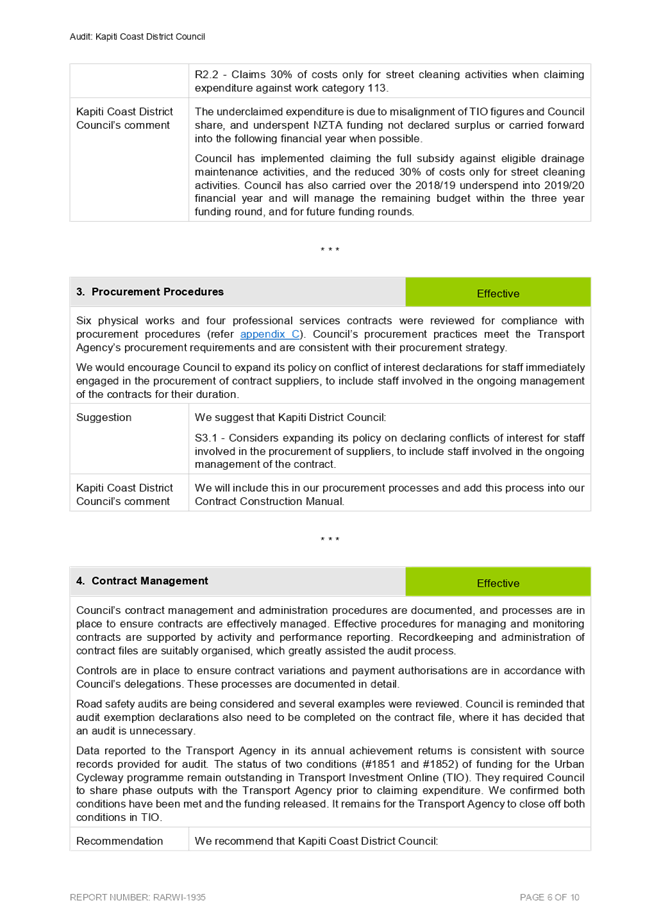

· Procurement

Procedures

Six physical

works and four professional services contracts were reviewed for compliance

with procurement procedures. Council’s procurement practices meet the

Transport Agency’s procurement requirements and are consistent with

their procurement strategy.

· Contract

Management

Council’s

contract management and administration procedures are documented, and

processes are in place to ensure contracts are effectively managed. Effective

procedures for managing and monitoring contracts are supported by activity

and performance reporting. Recordkeeping and administration of contract files

are suitably organised, which greatly assisted the audit process. Controls

are in place to ensure contract variations and payment authorisations are in

accordance with Council’s delegations. These processes are documented

in detail.

· Professional

Services

Council has

documented the management structure for its in-house operations and the

methodology covering how costs for in-house services, including associated

overheads and administration, are determined in accordance with Transport

Agency requirements. Budgeted expenditure for the business unit for the

current financial year (2019/20) appear reasonable. Council’s costs for

the previous three years are consistently mid-range when compared with

Council’s urban peer group.

|

11. The

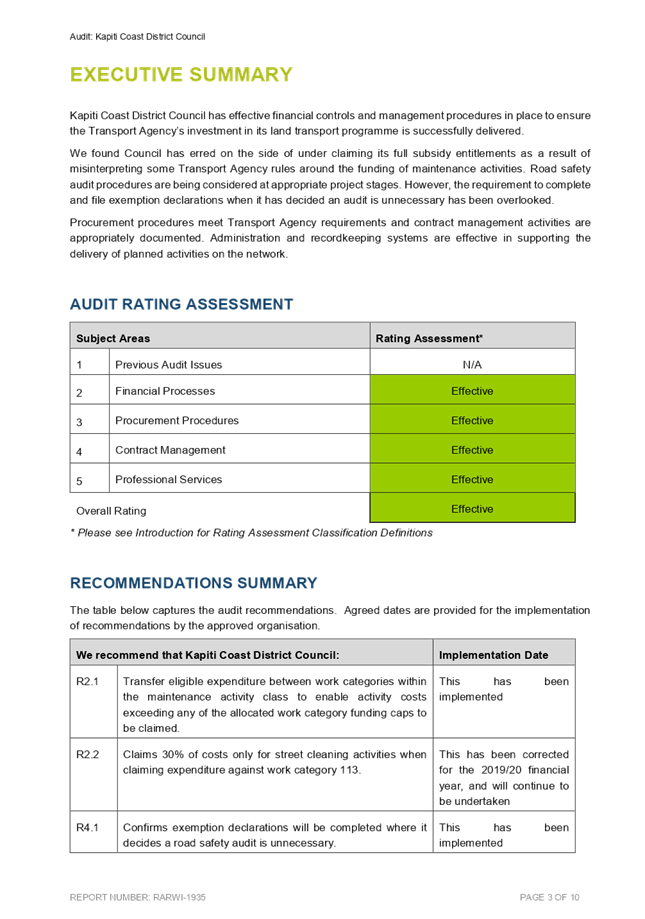

overall audit rating for our Council was effective, which is the highest

obtainable rating. All subject areas assessed were also rated as effective.

12. The

audit identified minor issues for Council to address, and these were identified

as recommendations or suggestions in the audit and are listed as follows:

· Financial

Processes

Recommendation

1 - Transfer eligible expenditure between work categories within the

maintenance activity class to enable activity costs exceeding any of the

allocated work category funding caps to be claimed.

Recommendation

2 - Claim 30% of costs only for street cleaning activities when claiming

expenditure against work category 113.

These

recommendations were made so to ensure that Council claimed the allowable

funding entitlements. Following this recommendation Council has implemented

changes to allow the full subsidy to be claimed.

· Procurement

Procedures

Suggestion -

Consider expanding the policy on declaring conflicts of interest for staff

involved in the procurement of suppliers, to include staff involved in the

ongoing management of the contract.

This suggestion will be considered by

Council.

· Contract

Management

Recommendation - Confirm exemption

declarations will be completed where it decides a road safety audit is

unnecessary.

This recommendation will be

implemented by Council.

13. The

executive summary of the audit report reads:

Kapiti Coast District Council has

effective financial controls and management procedures in place to ensure the

Transport Agency’s investment in its land transport programme is

successfully delivered.

We found Council has erred on the

side of under claiming its full subsidy entitlements as a result of

misinterpreting some Transport Agency rules around the funding of maintenance

activities. Road safety audit procedures are being considered at appropriate

project stages. However, the requirement to complete and file exemption

declarations when it has decided an audit is unnecessary has been overlooked.

Procurement procedures meet

Transport Agency requirements and contract management activities are

appropriately documented. Administration and recordkeeping systems are effective

in supporting the delivery of planned activities on the network.

CONSIDERATIONS

Policy considerations

14. There

are no policy considerations from this report.

Legal considerations

15. There

are no legal considerations from this report.

Financial considerations

16. Any

financial considerations are accommodated under current budgets.

Tāngata whenua considerations

17. There

are no Iwi considerations from this report.

Strategic considerations

18. This

audit relates to infrastructure investment that supports resilience and agreed

growth projections, and improved accessibility of Council services.

SIGNIFICANCE AND ENGAGEMENT

Significance policy

19. This

matter has a low level of significance under Council’s Significance and

Engagement Policy.

Consultation already undertaken

20. Consultation

was not required for this report.

Engagement planning

21. Engagement

was not required for this report.

Publicity

22. A

media release will be developed around the findings of this audit.

.

|

Recommendations

That the Operations and Finance Committee notes the

findings from the February 2020 Waka Kotahi Procedural Investment Audit

Report.

|

Appendices

1. Kapiti

Coast 2020 Audit ⇩

|

Audit

and Risk Sub-committee Meeting Agenda

|

13 August 2020

|

9 Confirmation

of Minutes

9.1 Confirmation

of minutes

Author: Tanicka

Mason, Democracy Services Advisor

Authoriser: Leyanne

Belcher, Democracy Services Manager

|

Recommendations

That the minutes of the Audit

& Risk Subcommittee meeting on 20 February 2020 be accepted as a true and

accurate record of the meeting.

|

Appendices

1. Minutes

20 February 2020 ⇩

|

Audit

and Risk Sub-committee Meeting Agenda

|

13 August 2020

|

MINUTES OF Kapiti Coast District Council

Audit and Risk

Sub-committee Meeting

HELD AT THE Council

Chamber, Ground Floor, 175 Rimu Road, Paraparaumu

ON Thursday, 20

February 2020 AT 9.30am

PRESENT: Cr

Angela Buswell, Deputy Mayor Janet Holborow, Cr Gwynn Compton, Mr Gary Simpson,

Mr Bryan Jackson

IN

ATTENDANCE: Wayne Maxwell (Mr), Mark de Haast (Mr), Natasha Tod (Ms), Glen

O’Connor (Mr), Janice McDougall (Mrs), Tim Power (Mr), Jacinta Straker

(Ms), Anelise Horn (Ms),Tanicka Mason (Mrs), David Borrie (Mr), Grayson Rowse

(Mr), Dan O’Connel (Mr), Jill Griggs (Mrs).

APOLOGIES: Mayor

K Gurunathan

LEAVE OF Nil

ABSENCE:

1 Welcome

2 Council

Blessing

The Chair welcomed everyone to the meeting and read the

Council blessing.

3 Apologies

|

Committee Resolution 2020/1

Moved: Cr

Gwynn Compton

Seconder: Mr Gary Simpson

That the apology received from Mayor K Gurunathan be

accepted.

Carried

|

4 Declarations

of Interest Relating to Items on the Agenda

Nil

5 Public

Speaking Time for Items Relating to the Agenda

Nil

6 Members’

Business

(a) Public

Speaking Time Responses

Nil

(b) Leave

of Absence

Nil

(c) Matters

of an Urgent Nature (advise to be provided to the Chair prior to the

commencement of the meeting)

Nil

7 Updates

Nil

8 Reports

|

8.1 Proposal